Common men invest their savings in multiple ways – investing in the stock market, mutual funds, issuing policies, fixed deposits, etc., to secure their future. These investments have always been a source of benefit at the worst phase of their lives.

But all of these investments must be made with proper documentation legally and an understanding of the full and final conditions of the same.

Key Takeaways

- Annuitants receive periodic payments from annuities, whereas beneficiaries inherit assets or receive benefits upon the policyholder’s death.

- Annuitants’ payments rely on the annuity’s performance, while beneficiaries’ payouts depend on the specific terms of an insurance policy or will.

- Annuitants can designate themselves or another person, but beneficiaries must be a separate individual or entity from the policyholder.

Annuitant vs Beneficiary

The difference between Annuitant and a Beneficiary is that Annuitant makes an investment in something like – bonds, policies, funds, etc. After some time, they use to receive it back every month. In contrast, comparatively, on the other side, a beneficiary doesn’t do any such commitments but only gets the profit in all cases.

Annuitant makes a certain investment in which, in the starting, they had to invest a huge lump of money, and then after a certain period, they receive it back on a monthly basis. This can be somehow taken as the retirement fund.

The money is given to the same person who made the annuity, but sometimes, in certain cases like the death of the Annuitant, the beneficiary or nominee gets it. The beneficiary is said to be a person who only gets the profit.

The person doesn’t have to make any investment or had to deposit any money but can get one. They are nominated by the person who had issued or opened any certain policy, deposits, or funds.

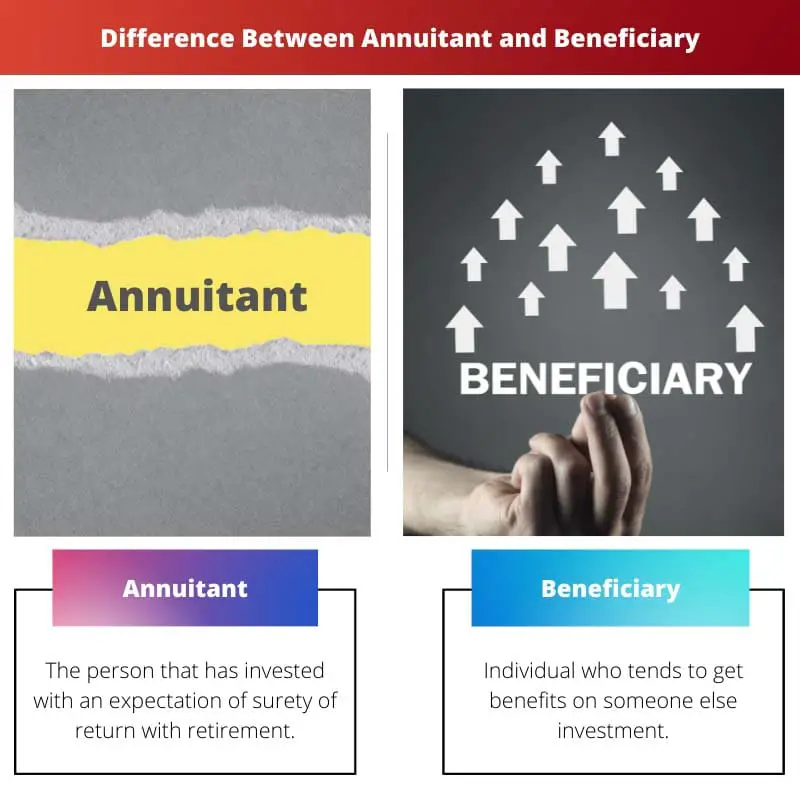

Comparison Table

| Parameters of Comparison | Annuitant | Beneficiary |

|---|---|---|

| Definition | The person that has invested with an expectation of surety of return with retirement | Individual who tends to get benefits on someone else investment |

| Tax Payment | Liable | Non-liable |

| Decision Making | They have complete rights to do so | They don’t have any right to make a decision |

| Types | Fixed and Variable | No such things |

| Profit Received | By themselves but in some cases like after death beneficiary gets it | In some cases |

What is Annuitant?

An annuitant is said to have made an investment in some annuity, and the return on investment is expected to be sure along with the retirement. In other words, it may sometimes refer to as a retirement fund for some people.

An annuity is opened by a huge lump of money, and the money deposits are made in the starting itself, and after that, the withdrawal can be made periodically. The person who has bought the annuity is said to be liable for paying taxes to the government for a certain time.

Plus, sometimes it also helps in saving the tax, but a condition for tax payment is that if the individual gets the payment before 59.5 of age themselves, they are said to be liable for paying a penalty of 10%. The Annuitant is liable to make any important decision regarding the annuity.

Even if the Annuitant has to add any beneficiary or nominee in it, they have to fully mention their respective full name with the percentage they are allotting them. And the most common annuity is known as fixed and variable annuities.

What is Beneficiary?

The beneficiary is used for the individual or the particular group that will be getting any advantage or profit from certain investments. These individuals don’t have to make any money deposits or have to spend a penny to get these returns from an annuity or bond, insurance, etc.

Even though, unlike the Annuitant, they aren’t liable for any tax on the money they receive. In some cases, like life insurance or making any annuity, it is necessary to make a beneficiary or nominee for future reference.

When an annuity is taken, the buyer is the first beneficiary in the case, but sometimes to avoid any inconvenience, the buyer if he/she dies, then the rest of the payment will stop, but if any other beneficiary is added, then the payment is taken by them. In a similar case of life insurance, the buyer has to mention the nominee or the beneficiary even if they are their respective children receiving it proportionately or disproportionately, it must be mentioned.

The individual is also not said to decide on insurance, bonds, funds, etc. But they only have to count the profit received in these cases.

Main Differences Between Annuitant and Beneficiary

- The word Annuitant is used for the individual who buys an annuity and gets an assured return along with retirement, whereas comparatively, on the other side, the word beneficiary is used for the individual or group of individuals that gets a benefit from the annuity.

- The Annuitant is said to be liable for paying tax on the money they receive from the annuity, whereas comparatively, on the other hand, the beneficiary is said to be not liable in any case to pay any tax payment or penalty on the receiving money.

- The Annuitant has the authority to make certain decisions regarding their annuity, whereas comparatively, on the other hand, the beneficiary does not have any such kind of authority to take any decision.

- An annuity can be classified into two main groups, the fixed annuity or the variable annuity, whereas comparatively, on the other hand, there are no such types in the beneficiary.

- The profit received by annuitants is when they are also mentioned as the first beneficiary in their annuity, whereas comparatively, on the other side, the profit received by a beneficiary is directly only in some cases.

- https://heinonline.org/HOL/LandingPage?handle=hein.journals/ssbul40&div=87&id=&page=

- https://heinonline.org/HOL/LandingPage?handle=hein.journals/taxlr9&div=28&id=&page=

- https://heinonline.org/HOL/LandingPage?handle=hein.journals/ssbul44&div=48&id=&page=

- https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1475-5890.2001.tb00042.x

Last Updated : 13 July, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The main differences between annuitant and beneficiary are articulated in a clear and concise manner, making it an excellent source of information for those wanting to understand the nuances of these financial roles.

The detailed comparison between annuitant and beneficiary serves as an excellent resource for anyone seeking to grasp the fundamental differences between these two concepts.

I completely agree with your assessment. The comparison table and detailed explanations are incredibly informative.

The article offers an in-depth look at annuitants and beneficiaries, providing valuable insights for individuals looking to understand these financial roles in more detail.

The distinction between annuitant and beneficiary is well-explained, outlining the specific rights and responsibilities of each role.

This is a comprehensive and detailed explanation of the differences between the annuitant and the beneficiary. It provides clear information to understand the topic better.

The comparison table is particularly useful to highlight the key differences between annuitant and beneficiary. It serves as a quick reference for understanding their distinctions.

I completely agree. The side-by-side comparison makes it easier to grasp the nuances between the two roles.

The detailed explanation about the tax implications for annuitants and beneficiaries provides a valuable insight into the financial considerations associated with these roles.

The section ‘What is Annuitant?’ provides a clear understanding of the investment process and the tax responsibilities. It’s elucidated concisely and comprehensively.

The article effectively establishes the essential aspects of annuitant and beneficiary. It’s an insightful read for anyone seeking to understand these concepts more deeply.