Debt represents borrowed funds that need to be repaid with interest, offering a fixed obligation but risking financial strain. Equity signifies ownership in a company, involving no fixed repayment but diluting ownership as more shares are issued, sharing profits and control with shareholders.

Key Takeaways

- Debt refers to borrowed funds that must be repaid with interest, whereas equity represents ownership in a company or asset, in the form of shares.

- Debt financing involves borrowing and repaying the money over time, while equity financing involves raising capital by selling ownership stakes in a company.

- Debt holders have priority over equity holders in the event of liquidation or bankruptcy, and interest payments on debt are tax-deductible, while dividends paid to equity holders are not.

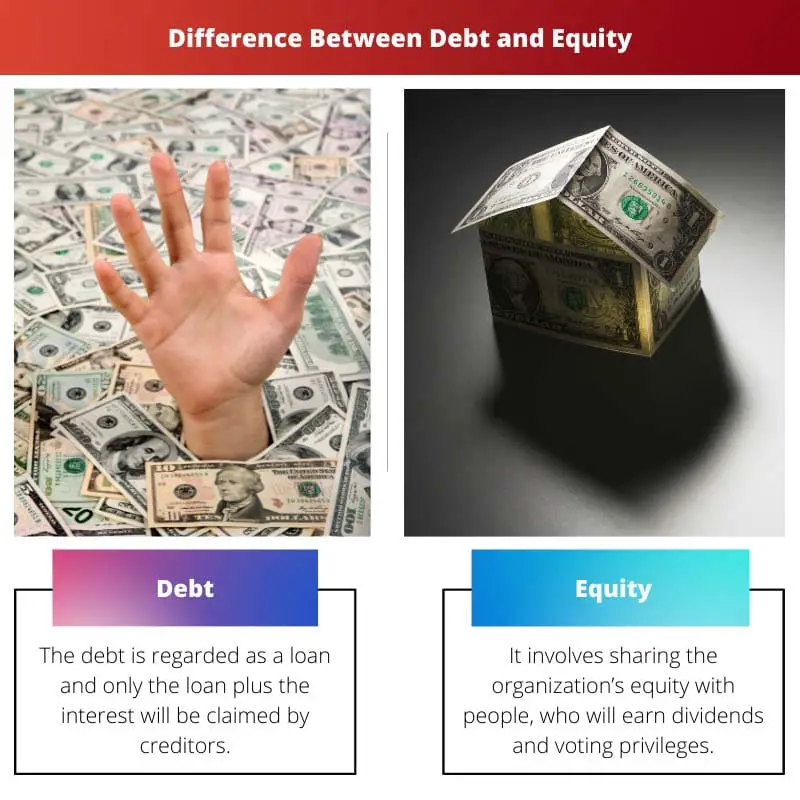

Debt vs Equity

The difference between debt and equity is that equity is valuable for those who go public and transfer the organization’s shares to others. The debt, however, is the amount of money lent by the creditor or third sources to the company and will be repaid, together with interest, over the years.

For an IPO to be conducted, an organization must incur various expenses. The situation is very different in the case of debt.

For two primary factors, businesses opt for debt. First, the firm will take some of the debt and build leverage if it goes through the equity path.

Secondly, companies do not wish to endure the difficult IPO phase and instead want a means of taking debts from banks or financial institutions. This write-up will discuss the difference between the two terms.

Comparison Table

| Feature | Debt | Equity |

|---|---|---|

| Source of Funds | Borrowing money from creditors (banks, investors) | Selling ownership stake in the company (shares) |

| Repayment Obligation | Principal amount + interest must be repaid at a predetermined time | No guaranteed repayment; shareholders only receive profits if declared as dividends |

| Cost of Capital | Generally lower than equity due to tax deductibility of interest payments | Generally higher than debt due to potential for higher returns |

| Ownership Rights | Debt holders have no ownership rights in the company | Equity shareholders have ownership rights and voting rights |

| Profit Sharing | Debt holders receive fixed interest payments regardless of company profits | Equity shareholders receive dividends only if the company generates profits and the board decides to distribute them |

| Control | Debt holders do not have voting rights and cannot influence company decisions | Equity shareholders have voting rights and can influence company decisions through voting |

| Risk | Lower risk for debt holders as they have a contractual claim on the company’s assets in case of bankruptcy. | Higher risk for equity shareholders as they are last in line to receive payment in case of bankruptcy. |

| Impact on Financial Ratios | Increases debt-to-equity ratio, which can affect creditworthiness | May not directly impact financial ratios, but can influence profitability and growth metrics |

| Suitability | Suitable for established companies with a good track record and stable cash flow | Suitable for startups and companies with high growth potential |

What is Debt?

Debt is a financial instrument that involves borrowing funds with the promise of repayment, with interest, over a specified period. It is a crucial component of a company’s capital structure and can take various forms, including loans, bonds, and other debt securities.

Characteristics of Debt:

- Fixed Obligation: Debt comes with a predetermined repayment schedule, specifying the principal and interest payments over the loan or bond’s tenure. This fixed obligation provides clarity to both the borrower and lender.

- Interest Payments: Borrowers are required to pay interest on the borrowed amount, which represents the cost of utilizing the funds. The interest rate can be fixed or variable, depending on the terms of the debt agreement.

- Creditor Claims: In the event of liquidation, creditors holding debt have priority over equity holders in claiming assets. This priority is established through legal agreements and is a key factor in assessing risk and return associated with debt.

- Leverage: Debt allows companies to leverage their capital, amplifying returns on equity. However, excessive leverage also increases financial risk, as interest payments become a fixed cost, irrespective of the company’s performance.

- Diverse Forms: Debt instruments can take various forms, such as bank loans, corporate bonds, convertible bonds, and other debt securities. Each form has distinct terms, conditions, and implications for the borrower and lender.

Pros and Cons of Debt:

Pros:

- Tax Deductibility: Interest payments on debt are tax-deductible, providing a potential tax advantage for businesses.

- Financial Leverage: Debt enables companies to amplify returns on equity, potentially leading to higher profitability.

Cons:

- Financial Risk: Excessive debt increases financial risk, especially if the company struggles to meet its debt obligations during economic downturns.

- Fixed Payments: The fixed nature of debt payments can strain cash flow, particularly if the business faces unexpected challenges.

What is Equity?

Equity represents ownership in a company and reflects the residual interest in the assets after deducting liabilities. It is a critical component of a company’s capital structure and provides shareholders with certain rights and claims on the company’s earnings and assets.

Characteristics of Equity

- Ownership Stake: Equity holders, or shareholders, are owners of the company. They have a claim on the company’s assets and earnings proportionate to their ownership stake, represented by the number of shares they hold.

- No Fixed Repayment: Unlike debt, equity does not involve a fixed obligation for repayment. Equity investors participate in the company’s success through capital appreciation and dividends but bear the risk of fluctuations in the value of their investment.

- Residual Claim: In the event of liquidation, equity holders have a residual claim on the company’s assets after all debts and obligations have been settled. This residual claim reflects the ownership’s risk and potential reward.

- Voting Rights: Common shareholders have the right to vote on key company decisions, such as the election of the board of directors and major corporate actions. The voting power is proportional to the number of shares held.

- Dividends: Companies may distribute a portion of their profits to shareholders in the form of dividends. While not guaranteed, dividends provide a direct financial benefit to equity holders and are a key factor for income-oriented investors.

Types of Equity

- Common Stock: Represents basic ownership in a company, providing voting rights and potential dividends. Common shareholders have the highest risk and reward potential.

- Preferred Stock: Grants priority in receiving dividends and liquidation proceeds over common shareholders. However, preferred shareholders do not have voting rights.

Pros and Cons of Equity

Pros:

- No Fixed Repayment: Equity does not involve fixed repayment obligations, reducing financial strain during challenging periods.

- Permanent Capital: Equity represents permanent capital, providing stability to the company’s capital structure.

Cons:

- Dilution: Issuing additional equity can dilute existing shareholders’ ownership and potentially impact control and earnings per share.

Main Differences Between Debt and Equity

- Obligation and Repayment:

- Debt: Involves a fixed obligation for repayment, including principal and interest, over a specified period.

- Equity: Does not entail a fixed repayment obligation; instead, equity investors share in the company’s success without a predetermined repayment schedule.

- Ownership and Control:

- Debt: Does not confer ownership; creditors have a legal claim to repayment but do not participate in company ownership or decision-making.

- Equity: Represents ownership in the company, entitling shareholders to voting rights and a share of profits. However, excessive equity issuance can dilute existing shareholders’ ownership.

- Risk and Returns:

- Debt: Involves fixed interest payments, providing clarity but increasing financial risk. Creditors have priority claims in case of liquidation.

- Equity: Bears the risk of fluctuating share values but offers the potential for higher returns through capital appreciation and dividends. Equity holders have a residual claim on assets after debts are settled.

- Tax Treatment:

- Debt: Interest payments on debt are tax-deductible, providing a potential tax advantage for businesses.

- Equity: Dividends are not tax-deductible, and there are no tax advantages associated with equity financing.

- Flexibility and Leverage:

- Debt: Allows companies to leverage their capital, potentially amplifying returns on equity. However, excessive leverage increases financial risk.

- Equity: Provides financial flexibility as there are no fixed repayment obligations. However, it may dilute ownership and control if additional equity is issued.

- Claim on Profits:

- Debt: Creditors receive fixed interest payments, irrespective of the company’s profitability. They do not share in the company’s success beyond the agreed-upon interest.

- Equity: Shareholders participate in the company’s profitability through dividends and capital appreciation. Their returns are linked to the company’s performance.

- Duration of Obligation:

- Debt: Has a finite duration, with a specified repayment period for the principal and interest.

- Equity: Represents a more permanent form of capital with no fixed maturity date.

- https://academic.oup.com/qje/article-abstract/109/4/1027/1866393

- https://www.nber.org/chapters/c4790.pdf

Last Updated : 26 February, 2024

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The article enriches readers with comprehensive knowledge about finance, which is essential in today’s financial landscape.

It’s a valuable source of information for both professionals and learners in the finance industry.

The author’s straightforward approach to explaining complex financial terms makes this article an excellent resource for anyone seeking knowledge in this field.

I find this article very helpful in understanding financial decisions and their consequences.

The article uses examples effectively to illustrate key concepts, which makes it easier to comprehend.

Yes, the practical examples help in understanding the real-life applications of these financial systems.

This article provides a clear and concise explanation of the differences between debt and equity financing. It is well-written and informative.

I couldn’t agree more. The article breaks down complex financial concepts into easy-to-understand terms.

The article’s objective comparison of debt and equity financing provides valuable insights for individuals and businesses looking to make informed financial choices.

This article is a must-read for those interested in finance and investments.

Absolutely, understanding these concepts is crucial for sound financial planning.

The article is an intelligent and thorough explanation of debt and equity financing, providing readers with valuable insights.

The author’s expertise in finance shines through in this article.

I agree, it’s a comprehensive guide to understanding the complexities of financial systems.

The author’s meticulous comparison between debt and equity financing provides a thorough understanding of both concepts.

Absolutely, the level of detail in the article is commendable.

The information presented here is crucial for those looking to understand the implications of debt and equity financing on their companies or investments.

Absolutely, it’s knowledge that every business owner and investor should have.

It’s an essential guide for making informed financial decisions.

The comparison table is incredibly helpful in understanding the key differences between debt and equity financing.

I found the table to be a great visual aid, summarizing the information effectively.

This article effectively demystifies complex financial terms, providing clarity to those seeking knowledge in finance.

Indeed, the clarity in explanations is one of the strengths of this article.