Education is much-needed wisdom for anyone. All need proper education to make this world a better place to live in.

Education comes with a cost, and the cost, at times, is enormous. Subduing talents for no money is close to the destruction of the world.

Federally guaranteed loans are available for students to ensure they graduate with flying colours. The support which the money offers for education as loans is categorized into subsidized and unsubsidized loans.

Key Takeaways

- Subsidized loans are need-based loans offered to eligible students, where the government pays the interest on the loan while the student is in school, during the grace period and deferment.

- Unsubsidized loans are not need-based and are available to eligible students regardless of financial need. Still, the borrower is responsible for paying the interest during all periods, including during school and deferment.

- The primary difference between subsidized and unsubsidized loans is the interest payment responsibility. The government covers the interest for subsidized loans during specific periods, while the borrower is responsible for all interest on unsubsidized loans.

Subsidized vs Unsubsidized Loans

Only undergraduate students with financial need are eligible for subsidized loans. When the borrower is enrolled in school at least part-time, no interest is charged. While both graduate and undergraduate students are eligible for unsubsidized loans. They are not determined by financial necessity.

It is well understood from the financial norms to complete an unsubsidized loan first before repaying the subsidized loan. Nevertheless, norms are set for students to acquire knowledge to put into worthwhile actions.

Comparison Table

| Parameter of Comparison | Subsidized Loans | Unsubsidized Loans |

|---|---|---|

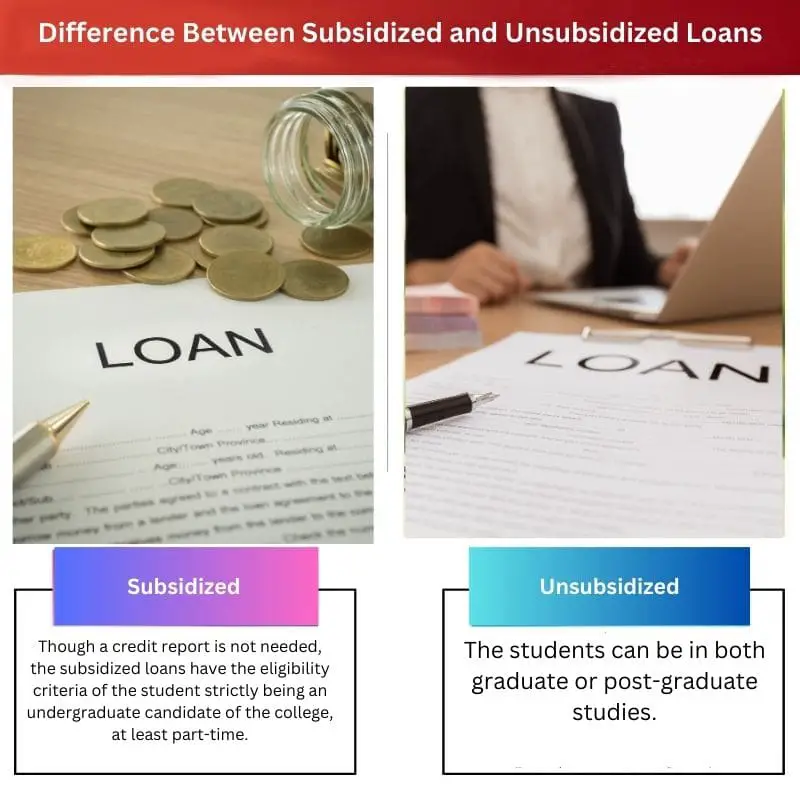

| Availability Criteria | Though a credit report is not needed, the subsidized loans have the eligibility criteria of the student strictly being an undergraduate candidate of the college, at least part-time. | The students can be in both graduate or post-graduate studies. |

| How is the amount determined | The amount is determined based on financial need. It does not exceed the same too. The school determines the amount of money be availed as a loan. | This loan also is determined by the school after considering the cost of attendance. They also consider if there is any other financial help received earlier. |

| Repayment Procedure | The interest does not add to the principal amount until the studies are completed. Further, a grace period of 6 months is applied immediately after graduation for the repayment to begin. | The interest starts adding to the principal amount from the beginning, and the borrower repays it once the term of studies is completed. |

| Loan Limits | Subsidized loans are always lower in limits as it is based on the exact financial need for the education to be completed. | Students can avail of higher loan amounts when compared to subsidized loans. |

| Eligibility Criteria | Financial needs must be submitted to be eligible for the loan | There is no need to submit any financial need for this loan |

What are Subsidized Loans?

Subsidized loans are federal loans offered to a student to complete his/her graduation. The loans are of low interest and are available only for students in undergraduate programs.

Subsidized loans are not only low-interest loans but also have an advantage to the student of not making the repayment during his study period. Moreover, a grace period of 6 months is offered for non-payment to support the student in finding a job.

It is also good to be understood that the interest does not add up to the principal amount during the study period as well as the grace period. If the loan payment is postponed as deferment, even then, the interest is not added to the principal.

If an amount of $10000 is availed as a subsidized loan, it remains the same when the repayment period starts. More importantly, when the repayment is made, the amount gets directly deducted from the principal amount.

Subsidized loans are designed for lower-income parents who want their wards to study. The school decides the loan amount, and the amount is always limited.

Subsidized loans can be availed only by submitting the financial need as an eligibility criterion. The best part is this loan will never get bigger over time.

What are Unsubsidized Loans?

Unsubsidized loans are offered to students who want to complete his/her education. It is offered to both graduates as well as postgraduate students at a lower interest rate.

Unsubsidized loans will require the students to pay back after graduation. No grace period offers to exist for unsubsidized loans, as the interest keeps adding even during the grace period.

The interest starts adding to the principal amount from the time the loan is taken. It is expected of the student to pay back the interest as well as the principal within the stipulated time without any deferment or non-payment.

The non-payment of unsubsidized loan interest on time will also add up to the interest as a penalty. Interest in interests shall also add up if any payment is missed.

No financial need is to be submitted to avail of this loan. Unsubsidized loans are easy to avail of, and not much documentation is needed too.

Any, even wealthy parents, can take this loan. Here again, the school decides the loan amount but can have higher limits on loans.

Main Differences Between Subsidized and Unsubsidized Loans

- Although the loan terms and interest rates are more or less similar for both loans, the main difference between Subsidized and Unsubsidized loans is the interest accruing factor. In subsidized loans, the interest does not accrue until the education is completed, whereas unsubsidized loans attract interest from when it is borrowed.

- The amount that can be borrowed is lower in the case of Subsidized loans when compared to their opposite counterpart.

- Subsidized loans are applicable only for undergraduate students, whereas unsubsidized loans are offered for both graduates as well as postgraduate students. Mainly, a graduate cannot avail of a subsidized loan.

- Income-based repayment options work wonders with subsidized loans as the interest would not have grown higher while completing the graduation. In contrast, income-based repayment can be supportive of unsubsidized loan repayment but not practical as the interest would have added to the principal for all the time payment was not made.

- Subsidized loans are strictly given to students who have exceptional financial need statements. Unsubsidized loans do not need any financial need as a requirement.

The article effectively presents the finer details of student loans, ensuring that students and families are well-informed about subsidized and unsubsidized loan options. It’s essential to have a comprehensive understanding of these financial considerations when navigating higher education.

Indeed, understanding the differences between subsidized and unsubsidized loans equips students with the knowledge to make informed financial decisions about their education and loan options.

Absolutely, this article is a valuable resource for students seeking to comprehend the financial impact of subsidized and unsubsidized loans. It’s crucial for students to make informed choices about financing their education.

The comparison table provided in the article offers a comprehensive breakdown of the differences between subsidized and unsubsidized loans. This detailed analysis is incredibly valuable for students navigating the complexities of student loans.

This article provides students with an essential guide to understanding the eligibility criteria and repayment procedures of subsidized and unsubsidized loans, ensuring that they are well-equipped to make informed financial decisions for their education.

I completely agree, the detailed comparison table serves as a helpful resource for students seeking to understand the financial nuances of subsidized and unsubsidized loans.

The breakdown of subsidized and unsubsidized loans is valuable for prospective students and their families. Understanding the eligibility criteria and repayment procedures can help students make well-informed decisions about financing their education.

I agree, the article carefully delves into the nuances of subsidized and unsubsidized loans, offering clarity on the financial obligations associated with each type of loan.

Absolutely, this article provides a comprehensive overview of student loans, which is particularly important for families navigating the complexities of financing higher education.

The cost of education and student loans can be staggering. It’s disheartening to think of the financial burden placed on students, but this article sheds light on the options available to ease that burden.

The article does a great job of outlining the various facets of student loans, which is crucial for anyone navigating higher education. It’s important to be aware of every option available to mitigate the financial strain of education.

Indeed, the financial impact of pursuing education can be daunting, but knowing the difference between subsidized and unsubsidized loans can empower students to make more informed choices about their loans.

The detailed insights into subsidized and unsubsidized loans help students grasp the financial responsibility associated with their educational funding. It’s important for students to have a clear understanding of the terms and obligations of their loans.

Absolutely, understanding the finer details of student loans is imperative for students as they embark on their educational journey. This article provides a comprehensive overview of the financial considerations associated with subsidized and unsubsidized loans.

The detailed breakdown of subsidized and unsubsidized loans in the article offers valuable insights for students to understand the financial responsibilities associated with their education. It’s essential for students to have a comprehensive understanding of the implications of their student loans.

Absolutely, the article provides students with valuable knowledge about the financial nuances of subsidized and unsubsidized loans, ensuring that they can make well-informed decisions about their educational financing.

The article effectively highlights the important differences between subsidized and unsubsidized loans, providing insightful information for students and parents. It’s crucial for everyone to understand the financial implications of their education.

Absolutely, education should be accessible to all, and understanding the financial aspects of student loans is essential for making informed decisions about higher education.

The norms and procedures outlined in the article are crucial for students to understand the financial implications of their educational choices. It’s essential to have a clear understanding of the differences between subsidized and unsubsidized loans before making borrowing decisions.

Absolutely, a well-informed approach to student loans ensures that students are equipped to manage the financial commitments associated with higher education effectively.

The article carefully delineates the financial implications of student loans, providing a comprehensive guide for students to navigate the complexities of subsidized and unsubsidized loans. It’s a valuable resource for those embarking on higher education.

I completely agree, the article serves as an essential guide for students and parents to gain clarity on the complexities of student loans, ensuring that they can approach higher education with informed decisions about financial obligations.

Absolutely, the insights presented in the article offer a thorough understanding of the financial considerations associated with subsidized and unsubsidized loans, providing students with the knowledge to make informed financial decisions about their education.

The clarity provided by the article on the differences between subsidized and unsubsidized loans is invaluable for students navigating the complexities of student loan options. It ensures that students make informed decisions about their financial commitments.

Absolutely, understanding the implications of subsidized and unsubsidized loans allows students to approach their education with a well-considered financial strategy, enabling them to make informed decisions about their student loans.