A credit score reflects a person’s creditworthiness based on their credit history, while a credit limit is the maximum amount of credit a lender extends to an individual. While a high credit score indicates reliability, a higher credit limit offers greater borrowing capacity, both influencing one’s financial opportunities and responsibilities.

Key Takeaways

- A credit score is a numerical representation of a person’s creditworthiness based on credit history and financial behavior; a credit limit is the maximum amount a person can borrow from a lender or spend using a credit card.

- Lenders use credit scores to determine creditworthiness and interest rates; credit limits are set by lenders based on factors such as income, credit history, and credit score.

- A higher credit score can lead to better credit terms and higher credit limits, while a lower score may result in less favorable terms and lower credit limits.

Credit Score vs Credit Limit

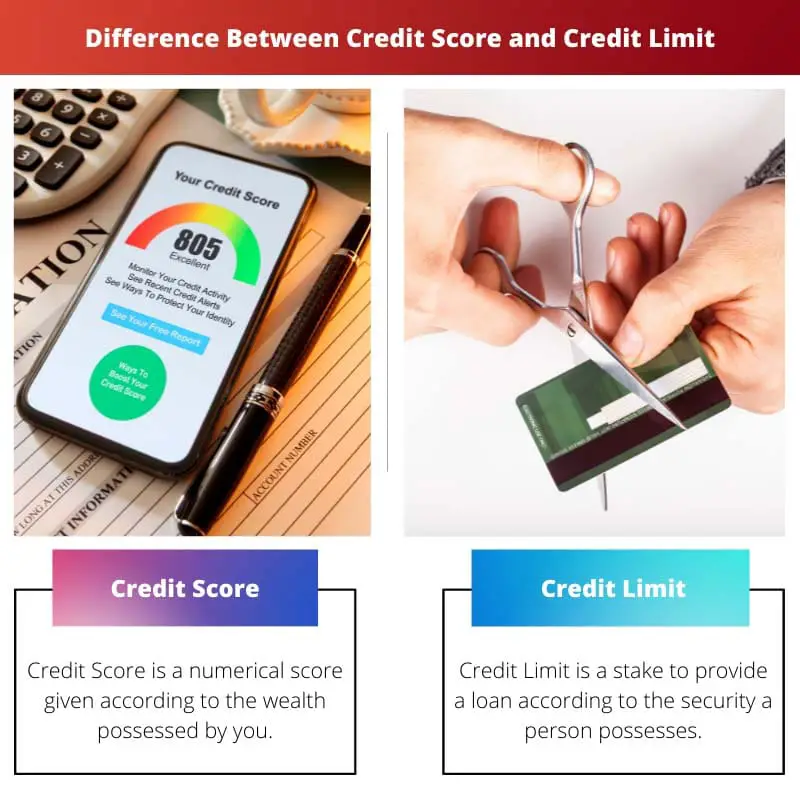

A credit score is a numerical representation of a person’s creditworthiness, based on their credit history and current credit status. A credit limit is the maximum amount of credit that a financial institution or other lender will extend to a debtor for a particular line of credit.

Credit Score is a parameter to understand the creditworthiness of a customer. This score gives the lenders/credit card companies an idea of the secureness they can have if they lend the customer cash.

Different credit score levels are maintained to qualify for other loan claims.

A credit limit is a parameter to understand the capability of a credit receiver. If a certain amount is lent to a customer, the resources available to him are checked beforehand so that the lender will not have to face a loss in the future.

A line of credit is maintained; if crossed, no more credits can be given to the debtor.

Comparison Table

| Feature | Credit Score | Credit Limit |

|---|---|---|

| Definition | A numerical representation of your creditworthiness, ranging from 300 to 850. | The maximum amount of credit a lender extends to you on a credit card or line of credit. |

| Purpose | Used by lenders to assess the risk of lending you money and determine the interest rate you will be charged. | Sets a spending limit on your credit card or line of credit. |

| Calculation | Calculated by credit bureaus using a complex formula that considers factors like payment history, credit utilization, credit history length, and credit mix. | Determined by lenders based on your creditworthiness, income, and employment history. |

| Impact on your finances | Higher scores lead to lower interest rates on loans and better credit card terms. | Lower credit utilization (using less of your credit limit) can positively impact your credit score. |

| Management | You can improve your score by making timely payments, keeping credit utilization low, and maintaining a healthy credit mix. | You can manage your spending by staying within your credit limit and avoiding exceeding it. |

| Direct control | You have limited direct control over your credit score as it is based on past financial behavior. | You have complete control over your credit limit and can request adjustments from your lender. |

What is Credit Score?

Factors Affecting Credit Score:

- Payment History: The most significant factor influencing a credit score is the borrower’s payment history. This includes whether they have made timely payments on credit accounts, loans, and other financial obligations. Missed or late payments can significantly lower a credit score.

- Credit Utilization Ratio: This ratio represents the amount of credit being used compared to the total credit available. Keeping credit card balances low relative to the credit limit can positively impact the credit score, as high credit utilization suggests financial strain.

- Length of Credit History: The length of time an individual has been using credit accounts also affects their credit score. A longer credit history demonstrates stability and responsible credit management, potentially boosting the credit score.

- Types of Credit in Use: Lenders prefer to see a mix of different types of credit accounts, such as credit cards, installment loans, and mortgages. A diverse credit portfolio can positively influence the credit score, indicating responsible financial management.

- New Credit Applications: Applying for multiple new credit accounts within a short period can negatively impact the credit score. Each application generates a hard inquiry on the credit report, signaling potential financial strain or a higher risk of default.

Importance of Credit Score:

- Loan Approval: A good credit score significantly increases the likelihood of loan approval for mortgages, auto loans, personal loans, and credit cards. Lenders use credit scores to evaluate the risk of default, with higher scores qualifying for better loan terms and lower interest rates.

- Interest Rates: Borrowers with higher credit scores receive lower interest rates on loans and credit cards. A good credit score can save individuals thousands of dollars in interest payments over the life of a loan.

- Financial Opportunities: Beyond borrowing, a good credit score can open doors to other financial opportunities, such as renting an apartment, securing insurance coverage, or even obtaining favorable terms on utility services.

What is Credit Limit?

Determining Factors of Credit Limit:

- Creditworthiness: Lenders assess the creditworthiness of a borrower based on factors such as credit history, income, debt-to-income ratio, and payment history. Borrowers with higher credit scores and more stable financial profiles are offered higher credit limits.

- Income and Financial Stability: Lenders also consider the borrower’s income and overall financial stability when determining the credit limit. A higher income and lower debt burden may result in a higher credit limit, as it suggests the borrower has the means to repay borrowed funds.

- Existing Credit Relationships: For existing customers, lenders may consider the borrower’s history with the institution when determining credit limits. Positive repayment history and a longstanding relationship may lead to higher credit limits being offered.

- Credit Card Type: Different types of credit cards may come with varying credit limits. Premium or high-end credit cards offer higher credit limits compared to standard or secured credit cards. The credit limit may also vary based on the card’s rewards program and benefits.

Importance of Credit Limit:

- Purchasing Power: The credit limit dictates how much a cardholder can spend using their credit card or access through a line of credit. A higher credit limit provides greater purchasing power and flexibility for making large purchases or managing unexpected expenses.

- Emergency Fund: A credit card with a sufficient credit limit can serve as an emergency fund, allowing cardholders to cover unexpected expenses or financial emergencies when cash flow is tight.

- Credit Utilization Ratio: The credit limit plays a crucial role in calculating the credit utilization ratio, which is the amount of credit being used compared to the total credit available. Maintaining a low credit utilization ratio, below 30%, can positively impact credit scores and demonstrate responsible credit management.

- Building Credit History: Responsible use of credit, including staying within the credit limit and making timely payments, can help individuals build a positive credit history over time. This, in turn, can lead to higher credit limits and better loan terms in the future.

Main Differences Between Credit Scores and Credit Limit

- Nature:

- Credit score is a numerical representation of an individual’s creditworthiness based on their credit history and financial behavior.

- Credit limit is the maximum amount of credit extended to an individual by a lender or financial institution.

- Calculation:

- Credit score is calculated based on various factors such as payment history, credit utilization ratio, length of credit history, types of credit accounts, and new credit applications.

- Credit limit is determined by the lender or credit card issuer based on factors like creditworthiness, income, existing credit relationships, and the type of credit card.

- Impact:

- Credit score influences the likelihood of loan approval, interest rates offered, and various financial opportunities.

- Credit limit determines the amount of credit available to the borrower, affecting purchasing power, credit utilization ratio, and emergency fund accessibility.

I was expecting a more in-depth discussion on the factors that influence credit scores and limits, but the article still presents a good introduction to the topic.

True, more details on influencing factors would have made it even more insightful.

I agree, but it’s a great starting point for anyone wanting to understand credit scores and limits.

While the article discusses an important topic, I felt that it could have delved deeper into the intricacies of credit scores and limits.

I understand your perspective, but it’s still a pretty comprehensive overview.

I found this article very informative and helpful. It explains the complex topic of credit score and credit limit in a very easy to understand manner. Great work!

It’s great to see such precise and comprehensive information on these topics. Kudos to the writer!

I agree! It really gave me a clear understanding of these financial terms.

The article provides a thorough and detailed explanation of credit scores and credit limits, ensuring that even a novice can comprehend these financial terms.

I couldn’t agree more. The article truly simplifies the complexities of credit scores and limits.

An excellent overview for anyone looking to understand these important financial concepts.

The article succinctly explains the significance and function of credit score and credit limit, making it a valuable read for anyone wanting to understand these financial aspects.

The article effectively distinguishes between credit score and credit limit, providing insights that are both informative and enlightening.

I agree, the informative nature of the content was quite impressive.

The usage of easy-to-understand language made the article even more engaging and helpful.

I already knew about credit scores and limits, but this article presents some additional aspects that I hadn’t considered before. Good read!

Absolutely, the article provided a fresh perspective on something I thought I knew everything about.

Yes, the comparisons and key takeaways really added value to my knowledge.

The straightforward comparison table and detailed explanations helped me understand the differences between credit score and credit limit better.

I appreciate the use of real-world examples in the explanation of credit score and credit limit, making it easier to relate to the concepts.

Agreed. The relatable examples enhanced the practical understanding of these terms.

This article successfully provides a clear and comprehensive explanation of credit score and credit limit. Very well-written!

I couldn’t agree more. The details provided are quite illuminating.