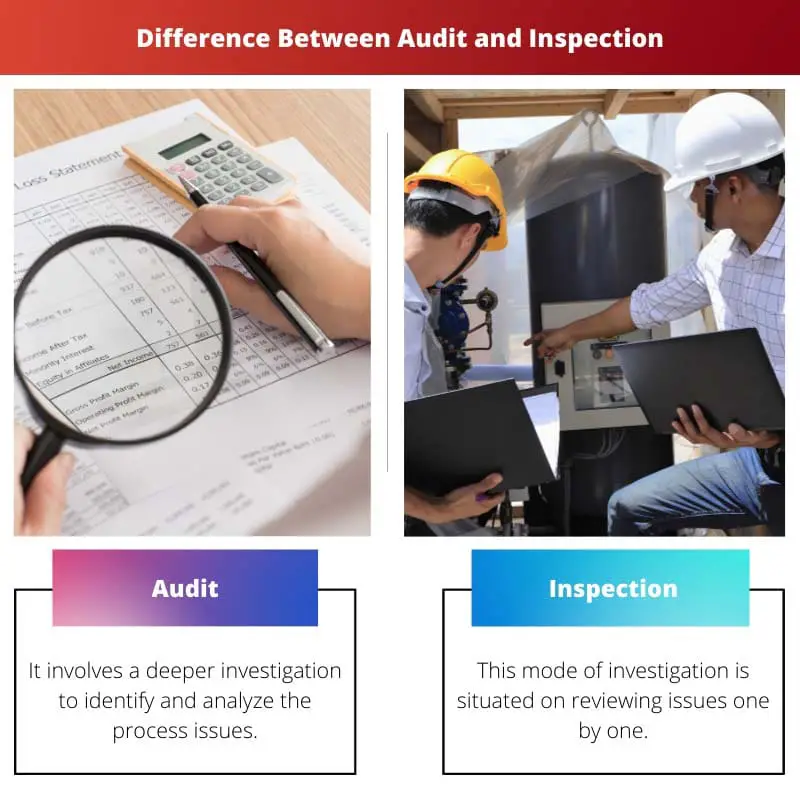

An audit is a systematic review and evaluation of processes, procedures, or systems to ensure compliance with standards or regulations, conducted by an independent party. On the other hand, an inspection is a more focused examination aimed at identifying specific issues, defects, or deviations from standards, conducted by internal or external inspectors.

Key Takeaways

- An audit is a formal examination of financial accounts to verify their accuracy and compliance with regulations.

- Inspection is visually examining a product or facility to ensure it meets the specified requirements.

- An audit is focused on financial accounts, while an inspection is focused on the product or facility.

Audit vs Inspection

Audit is a systematic and independent examination of an organization’s financial activities to ensure compliance with established policies and procedures. Inspection is a physical examination of an organization’s premises, equipment, and processes to ensure they meet safety and quality standards.

An audit is a tedious task encompassing planning, performing, and reporting to get a detailed vision of the ongoing investigation. Adding on, the Audit facilitates proper in-depth examination of goods and services.

Inspection is a relatively simple one-step process where the superiors examine the basic requirements of the workforce and the workplace. Still, an Audit is a complex process incorporating various steps to get the full details of that product or service.

For example: during an Inspection, the person in charge will only note the number of missing pieces of equipment, whereas, during an Audit, the person in charge will try to find out the reasons for the lost equipment through well-informed data and documentation.

This example depicts that Inspection majorly works on quantitative principles to provide a snapshot of the operative functions in an organization. In contrast, an Audit is more concerned about an organisation’s overall and detailed functioning.

Comparison Table

| Feature | Audit | Inspection |

|---|---|---|

| Purpose | To evaluate the effectiveness of a system, process, or control and identify opportunities for improvement | To verify compliance with specific rules, regulations, or standards |

| Scope | Broader, encompassing entire systems, departments, or organizations | Narrower, focusing on specific areas, tasks, or items |

| Depth | More in-depth, involving detailed analysis of documents, interviews, and observations | Less in-depth, involving visual observation and verification of checklists |

| Formalty | More formal, following a documented process and resulting in a comprehensive report | Less formal, conducted quickly and resulting in a simpler report or checklist |

| Frequency | Less frequent, conducted periodically (e.g., annually) | More frequent, sometimes conducted regularly or even continuously |

| Conducted by | Internal auditors (employed by the organization) or external auditors (independent) | Internal inspectors (employed by the organization) or external inspectors (from a regulatory body) |

| Outcome | Focuses on identifying weaknesses, recommending improvements, and ensuring long-term effectiveness | Focuses on identifying non-compliance, taking corrective actions, and ensuring adherence to regulations |

What is Audit?

Key Objectives of an Audit:

- Verification of Financial Information: Auditors assess the accuracy and completeness of financial statements, ensuring that they fairly represent the organization’s financial position, performance, and cash flows.

- Compliance Assurance: Audits verify whether the organization complies with applicable laws, regulations, and internal policies, reducing the risk of legal penalties, regulatory sanctions, or reputational damage.

- Evaluation of Internal Controls: Auditors examine the adequacy and effectiveness of internal control systems to mitigate risks, safeguard assets, and ensure the reliability of financial reporting.

- Identification of Operational Improvements: Through observations and recommendations, audits help identify opportunities for operational enhancements, cost savings, and process efficiencies.

Types of Audits:

- Financial Audit: This type of audit focuses on reviewing financial statements and records to ensure accuracy, completeness, and compliance with accounting standards and regulatory requirements.

- Operational Audit: Operational audits assess the efficiency and effectiveness of internal processes, procedures, and systems, aiming to enhance organizational performance and achieve strategic objectives.

- Compliance Audit: Compliance audits evaluate adherence to laws, regulations, contractual agreements, and internal policies to mitigate legal and regulatory risks and ensure ethical conduct.

- Information Systems Audit: Information systems audits examine the security, integrity, and reliability of IT infrastructure, data management practices, and cybersecurity measures to protect against cyber threats and data breaches.

Audit Process:

- Planning and Preparation: Auditors define objectives, scope, and methodologies, gather relevant information, and develop an audit plan tailored to the organization’s needs and risks.

- Fieldwork and Evidence Collection: Auditors conduct on-site visits, interviews, and examinations of documents, transactions, and records to gather evidence supporting their findings and conclusions.

- Analysis and Reporting: Auditors analyze the collected evidence, assess findings against audit criteria, and document observations, recommendations, and conclusions in an audit report presented to management and stakeholders.

- Follow-up and Monitoring: Auditors may follow up on audit recommendations to track implementation progress, address any outstanding issues, and ensure continuous improvement in organizational practices and performance.

What is Inspection?

Key Objectives of Inspection:

- Quality Assurance: Inspections verify the quality and conformity of products, materials, or services to specified standards, ensuring consistency, reliability, and customer satisfaction.

- Safety Compliance: Inspections assess adherence to safety regulations, guidelines, and industry standards to prevent accidents, injuries, or hazards in workplaces, facilities, or public spaces.

- Regulatory Compliance: Inspections ensure compliance with legal requirements, regulations, codes, and standards established by regulatory authorities or industry bodies to avoid penalties, fines, or legal liabilities.

- Process Improvement: Through the identification of deficiencies and opportunities for enhancement, inspections contribute to process optimization, efficiency gains, and cost reduction initiatives.

Types of Inspections:

- Product Inspection: Product inspections involve examining finished goods, components, or materials to verify quality, specifications, functionality, and compliance with standards before distribution or use.

- Process Inspection: Process inspections evaluate manufacturing processes, procedures, or operations to identify inefficiencies, deviations, or non-conformities and implement corrective measures for improved performance and quality.

- Facility Inspection: Facility inspections assess the condition, safety, and compliance of buildings, infrastructure, equipment, and environmental controls to ensure a safe and conducive working environment.

- Regulatory Inspection: Regulatory inspections are conducted by government agencies, regulatory bodies, or authorized auditors to enforce compliance with laws, regulations, and standards governing specific industries or activities.

Inspection Process:

- Preparation and Planning: Inspectors define objectives, criteria, and scope, develop inspection checklists, and schedule activities to ensure a systematic and thorough examination of the subject matter.

- On-site Inspection: Inspectors conduct visual inspections, measurements, tests, or interviews, comparing observed conditions or practices against established criteria, standards, or regulations.

- Documentation and Reporting: Inspectors record findings, observations, and deviations, document evidence through photographs, samples, or reports, and communicate results to relevant stakeholders, highlighting areas for improvement or corrective action.

- Follow-up and Verification: Inspectors may follow up to ensure corrective actions are implemented, verify compliance with recommendations, and monitor ongoing adherence to standards or regulations through periodic inspections and audits.

Main Differences Between Audit and Inspection

- Purpose:

- Audit:

- Verify accuracy of financial information.

- Evaluate compliance with regulations and internal controls.

- Inspection:

- Ensure compliance with standards, specifications, or requirements.

- Identify defects, deviations, or non-conformities.

- Audit:

- Scope:

- Audit:

- Comprehensive review of processes, procedures, or systems.

- Focus on financial records, operations, and internal controls.

- Inspection:

- Specific examination of products, processes, or premises.

- Assess quality, safety, and regulatory compliance.

- Audit:

- Outcome:

- Audit:

- Provides assurance on financial accuracy and compliance.

- Offers recommendations for process improvement.

- Inspection:

- Identifies defects or non-conformities requiring corrective action.

- Ensures adherence to quality, safety, and regulatory standards.

- Audit: