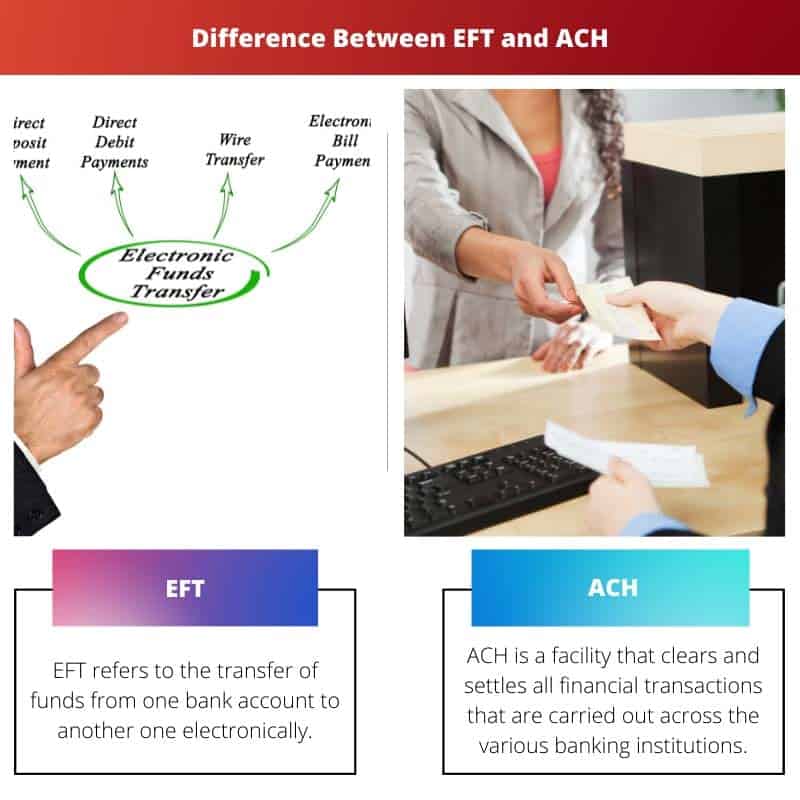

EFT (Electronic Funds Transfer) is a broader term that encompasses various electronic methods of transferring funds, while ACH (Automated Clearing House) is a specific type of EFT system commonly used for processing electronic payments and direct deposits in the United States.

Key Takeaways

- Electronic Funds Transfer (EFT) is a general term for electronic transactions between bank accounts. At the same time, Automated Clearing House (ACH) is a specific network for processing bulk electronic transactions in the United States.

- EFT covers a wide range of electronic payment methods, including wire transfers, credit cards, and ACH transactions, whereas ACH is a specific system for processing batch transactions.

- ACH transactions are lower-cost and slower than other EFT methods like wire transfers but are well-suited for high-volume, low-value transactions.

EFT vs ACH

EFT (Electronic Fund Transfer) refers to money transactions between bank accounts. EFT allows instantaneous fund transfers. ACH (Automated Clearing House) refers to money being transferred to different accounts collectively like paying salaries. It can take a few days to complete the transaction.

EFT is faster in comparison with ACH. While on the other hand, ACH has to connect to different banks that take time.

Comparison Table

| Aspect | Electronic Funds Transfer (EFT) | Automated Clearing House (ACH) |

|---|---|---|

| Purpose | General term for electronically transferring funds from one account to another. EFT can encompass various methods, including ACH. | A specific network and system for batch processing electronic payments, including direct deposits, bill payments, and other transactions. |

| Transfer Speed | Can vary depending on the method used (e.g., wire transfer, online banking, card transactions). Transactions can be processed in real-time or with a slight delay. | Typically processed in batches with specific processing windows, leading to a delay of at least one business day. |

| Transaction Types | Encompasses a wide range of electronic transactions, including wire transfers, online banking transfers, debit/credit card transactions, and more. | Primarily used for specific types of transactions, including direct deposits, payroll payments, vendor payments, tax refunds, and consumer bill payments. |

| Cost | Costs can vary widely depending on the specific EFT method used. Wire transfers, for example, may incur higher fees, while online banking transfers are free. | ACH transactions are less expensive than other EFT methods. Fees may apply for some ACH transactions, but they are lower. |

| Regulatory Oversight | Subject to regulatory oversight, but the level of regulation can vary depending on the specific EFT method and jurisdiction. | Highly regulated by the National Automated Clearing House Association (NACHA) in the United States. ACH transactions must comply with specific rules and guidelines. |

| Typical Use Cases | Used for various purposes, including retail transactions, person-to-person payments, online shopping, and more. | Commonly used for payroll processing, direct deposit of salaries, recurring bill payments (e.g., utilities, mortgages), vendor payments, and government disbursements. |

| Payment Network | Not tied to a specific payment network; various EFT methods may use different networks or channels. | Operates on a specific payment network, such as the ACH Network in the United States. Transactions are processed through this network. |

| Settlement Process | Settlement can occur in real-time or with a slight delay, depending on the specific EFT method. | ACH transactions are settled in batches with specific processing windows, leading to a delay in funds transfer. |

| International Use | Can be used for both domestic and international transactions, depending on the method and financial institutions involved. | Primarily used for domestic transactions within the country or region where the ACH network is established. International ACH transactions (IAT) are possible but less common. |

| Accessibility | Available through various channels, including banks, financial institutions, online banking platforms, payment processors, and more. | Accessible through banks, financial institutions, and organizations that are participants in the ACH network. |

What is Electronic Funds Transfer (EFT)?

Electronic Funds Transfer (EFT) is a secure and efficient digital method of transferring money between accounts, eliminating the need for physical currency or paper checks. This electronic process facilitates financial transactions, providing a swift and convenient means of exchanging funds.

Mechanism

- Initiation: EFT begins with the initiation of a transaction by the payer through electronic means, such as online banking, mobile apps, or automated systems.

- Authorization: The payer authorizes the transfer by providing necessary details like account numbers, amount, and recipient information. This step ensures the legitimacy and security of the transaction.

- Transmission: The payment details are securely transmitted through established electronic networks, such as the Automated Clearing House (ACH) system or wire transfers, enabling the seamless transfer of funds.

- Processing: Financial institutions process the transaction based on the provided information, verifying the availability of funds and ensuring compliance with security protocols.

- Completion: Once the processing is complete, the recipient’s account is credited, and the payer’s account is debited, finalizing the electronic funds transfer.

Benefits

- Speed and Efficiency: EFT enables swift and real-time transactions, reducing the time associated with traditional paper-based methods.

- Security: With encryption and authentication measures in place, EFT ensures secure financial transactions, minimizing the risk of fraud.

- Cost-Effective: EFT eliminates the need for physical handling of checks or cash, resulting in cost savings for both individuals and businesses.

- Accessibility: EFT can be initiated from anywhere with an internet connection, providing convenience and accessibility for users.

What is Automated Clearing House (ACH)?

Automated Clearing House (ACH) is an electronic funds transfer system that facilitates the seamless and secure transfer of funds between financial institutions within a country. It operates as a batch processing system, allowing businesses, individuals, and financial institutions to electronically initiate and receive payments.

Functionality

- Payment Processing: ACH serves as a centralized platform for processing various types of financial transactions, including direct deposits, bill payments, and business-to-business payments. This streamlines the transfer of funds, reducing the need for paper checks and manual processes.

- Batch Processing: ACH transactions are grouped into batches and processed in predefined intervals, on a daily basis. This efficiency makes it suitable for recurring payments, such as payroll deposits and utility bill payments.

- Direct Deposits and Withdrawals: ACH enables direct deposits, allowing employers to transfer salaries directly to employees’ bank accounts. It also facilitates automatic withdrawals for recurring payments, like mortgage installments and subscription fees.

- Cost-Effective and Timely: ACH transactions are cost-effective compared to traditional payment methods, such as wire transfers or paper checks. The system promotes timely fund transfers, enhancing financial efficiency for both businesses and individuals.

Security and Regulation

- Encryption and Authentication: ACH transactions prioritize security through encryption and authentication protocols, ensuring the confidentiality and integrity of sensitive financial information.

- Regulatory Oversight: ACH operations are subject to regulatory oversight to safeguard the interests of consumers and financial institutions. Compliance with established rules and regulations helps maintain the integrity of the electronic funds transfer system.

- NACHA Rules: The National Automated Clearing House Association (NACHA) establishes and enforces rules governing ACH transactions in the United States, ensuring standardized practices and promoting a secure and reliable electronic payments system.

Main Differences between Electronic Funds Transfer (EFT) and Automated Clearing House (ACH)

- Scope and Term:

- EFT: EFT is a broad term encompassing various electronic transfer methods between accounts. It is a general concept that includes various electronic financial transactions.

- ACH: ACH refers specifically to the Automated Clearing House network and system used for batch processing electronic payments, including direct deposits, bill payments, and other transactions. It is a specific network and term.

- Types of Transactions:

- EFT: EFT covers many electronic transactions, including wire transfers, online banking transfers, debit/credit card transactions, automated bill payments, and more. It can include retail, consumer, and business transactions.

- ACH: ACH primarily focuses on specific types of transactions, such as direct deposits (e.g., payroll and government benefits), direct debits (e.g., recurring bill payments), and business-to-business payments. It is used for scheduled and recurring transactions.

- Processing Speed:

- EFT: The speed of EFT transactions can vary widely depending on the specific method used. Some EFT transactions, such as wire transfers, can be processed in real-time, while others may take a short time or several business days.

- ACH: ACH transactions are processed in batches with specific processing windows, leading to a delay of at least one business day. They are not real-time transactions.

- Regulatory Oversight:

- EFT: EFT is subject to regulatory oversight, but the level of regulation can vary depending on the specific EFT method and the jurisdiction in which it is conducted.

- ACH: ACH transactions are highly regulated by the National Automated Clearing House Association (NACHA) in the United States. ACH transactions must comply with specific rules and guidelines established by NACHA.

- Costs and Fees:

- EFT: The costs associated with EFT transactions depend on the method used and the financial institutions involved. Some EFT methods may incur fees, while others, like online banking transfers within the same bank, are free or have minimal charges.

- ACH: ACH transactions are less expensive than other EFT methods. Fees may apply for some ACH transactions, but they are lower.

- Accessibility:

- EFT: EFT is available through various channels, including banks, financial institutions, online banking platforms, payment processors, and mobile banking apps. It offers convenience and flexibility for conducting financial transactions.

- ACH: ACH services are accessible through banks, financial institutions, and organizations participating in the ACH network. It is primarily used for specific types of transactions within the United States.

The post elucidates the complexities of EFT and ACH in a highly informative manner, facilitating a comprehensive understanding of these electronic transaction systems. The breakdown of transaction types, speed, costs, and accessibility of EFT is noteworthy.

I share your sentiments, Joel Scott. The detailed breakdown of key characteristics and features of EFT enhances readers’ knowledge of the various transaction types, speed, costs, and accessibility involved in electronic funds transfer.

The post offers a detailed comparison between EFT and ACH, providing readers with a comprehensive overview of the differences between these two electronic funds transfer methods. The inclusion of key characteristics and features of EFT enhances the post’s informational value.

I concur, Tanya Kelly. The delineation of key characteristics and features of EFT contributes significantly to the post’s informational depth, allowing readers to gain insights into the specifics of electronic funds transfer.

The breakdown of EFT and ACH into distinctive attributes and transaction types is vital for readers seeking to comprehend the nuances of electronic funds transfer systems – a highly informative post!

The post provides valuable insights into the differences between EFT and ACH, allowing readers to gain a deeper understanding of these electronic funds transfer systems. The comparison table is particularly useful for highlighting the distinctions between the two methods.

Indeed, the detailed comparison table effectively clarifies the varying aspects of EFT and ACH, enabling readers to discern their unique features and functionalities.

The detailed characteristics and features of EFT presented in the post offer readers valuable insights into the broad spectrum of electronic financial transactions. The post effectively captures the nuances of EFT and ACH, enhancing readers’ understanding of both systems.

I completely agree, Patricia Lloyd. The post’s detailed breakdown of the characteristics and features of EFT provides readers with a comprehensive understanding of the multifaceted nature of electronic funds transfer.

The comprehensive explanation and comparison of EFT and ACH are highly beneficial for readers seeking to understand the complexities of electronic funds transfer systems. The detailed breakdown of transaction types and regulation offers readers a comprehensive view of the functionalities and oversight associated with EFT and ACH.

Absolutely, Qkennedy. The detailed breakdown of transaction types and regulation serves as a valuable resource for readers, providing them with an in-depth understanding of the distinctive aspects of EFT and ACH.

The post provides an exhaustive account of EFT and ACH, delving into the fundamental aspects, settlement processes, and international use. The detailed breakdown of the settlement process and accessibility of each method is particularly insightful for readers.

I share your perspective, Srogers. The detailed breakdown of the settlement process and accessibility enriches readers’ knowledge of the various facets of EFT and ACH, fostering a deeper understanding of their functionalities.

This post offers a clear and comprehensive explanation of EFT and ACH, making it easy for readers to grasp the differences between the two. The inclusion of key takeaways, comparison tables, and detailed characteristics of EFT is highly informative and helpful.

I agree with your assessment, Bwilson. The breakdown of EFT and ACH into key takeaways and the detailed comparison table is very beneficial for those seeking to understand the specifics of each method.

The comprehensive explanation and comparison of EFT and ACH provided in the post offers readers valuable insights into the distinct characteristics and functionalities of these electronic transaction systems. The detailed breakdown of the purpose, transaction types, and cost of each method is particularly beneficial for readers.

I completely agree, Stevens Eileen. The detailed breakdown of the purpose, transaction types, and cost offers readers a comprehensive understanding of the unique aspects and functionalities of EFT and ACH.

The post effectively delineates the key characteristics and features of EFT, highlighting its various transaction types, speed, costs, and accessibility. The inclusion of a comparison table contributes significantly to the post’s informational value and educational content.

Indeed, Vturner. The comprehensive delineation of the key features and comparison table offers readers a detailed and informative overview of EFT and ACH, fostering a thorough understanding of electronic funds transfer systems.

The post presents an in-depth analysis of EFT and ACH, shedding light on their distinct features, regulatory oversight, and typical use cases. The detailed comparison table effectively captures the variances between the two systems, offering readers an insightful perspective.

Absolutely, Darren Edwards. The detailed comparison table provides readers with a clear and concise overview of the differences between EFT and ACH, enhancing their knowledge and understanding of these electronic funds transfer methods.

The comprehensive elucidation of regulatory oversight and typical use cases of EFT and ACH enriches the readers’ comprehension of these electronic transaction systems – an outstanding post!