An invoice is a document issued by a seller to a buyer, detailing the products or services provided, their quantities, prices, and payment terms, sent after a purchase. A statement, on the other hand, is a summary of transactions over a period, a month, showing all invoices, payments, and balances owed by the buyer to the seller, serving as a reminder of outstanding obligations.

Key Takeaways

- An invoice is a document that outlines a specific transaction, while a statement provides an overview of a customer’s account activity.

- An invoice is sent before payment, whereas a statement is sent after payment.

- An invoice includes details such as the quantity, price, and description of goods or services, while a statement summarizes the customer’s balance and payment history.

Invoice vs. Statement

An Invoice has a direct impact on the accounts of an organization. In contrast, a statement is just informational and is derived from the account itself; thus, it does not have any impact on an organization’s accounts. In simple words, an invoice calls for action, while a statement is just a reminder.

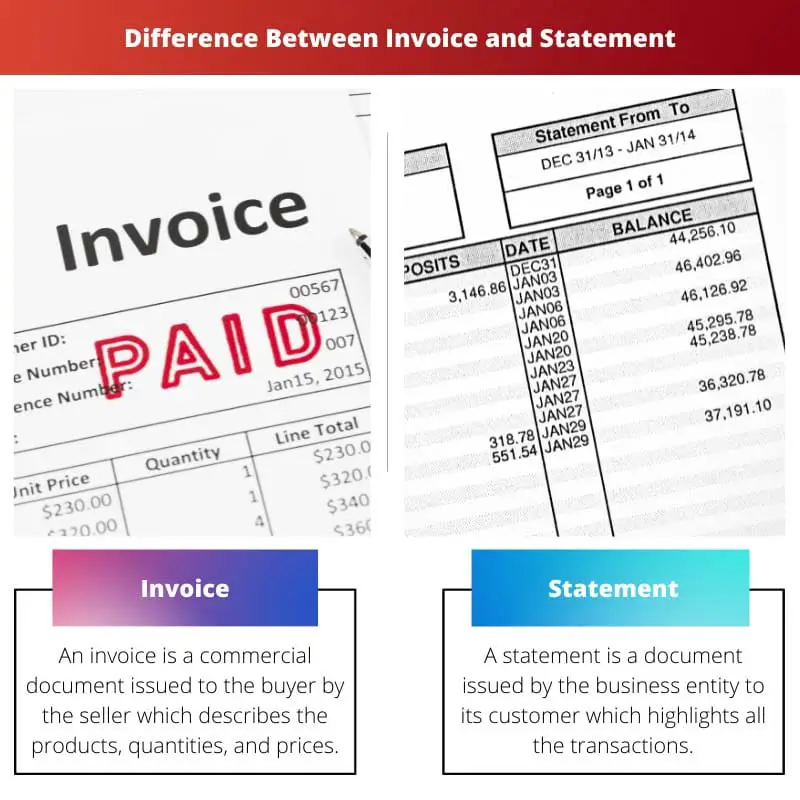

An invoice is a commercial document issued to the buyer by the seller describing the products, quantities, and prices involved in the transaction between the buyer and seller.

A statement is a document issued by the business entity to its customer that highlights all the transactions between them in a particular period.

Comparison Table

| Feature | Invoice | Statement |

|---|---|---|

| Purpose | Request for payment for a specific transaction or service. | Provides a summary of account activity over a specific period, including outstanding invoices and potentially other transactions (payments, credits, etc.). |

| Issued for | Each individual transaction or service rendered. | A specific time period (e.g., monthly, quarterly). |

| Content | Details of a specific transaction, including: * Date of sale or service * Description of goods or services provided * Quantity * Unit price * Total amount due * Payment terms (due date, discounts, penalties) | Overview of account activity, including: * List of outstanding invoices with brief details (date, amount) * Total amount due for the period * Payment history (payments received) * Remaining balance |

| Payment request | Yes, explicitly requests payment for the specific transaction. | No, does not directly request payment, but serves as a reminder of outstanding balances. |

| Legal document | Yes, serves as a legal record of the transaction and the amount owed. | No, not a legally binding document for requesting payment. |

| Frequency | Issued for each individual transaction. | Issued periodically (e.g., monthly). |

| Recipient | Customer or client who owes the payment. | Customer or client who has an open account with the business. |

What is an Invoice?

An invoice is a commercial document issued by a seller to a buyer, detailing the specifics of a transaction for goods or services provided. It serves as a formal request for payment from the buyer to the seller.

Components of an Invoice

- Header Information: This includes details such as the seller’s name, address, contact information, and the invoice number for identification and tracking purposes.

- Billing Information: It comprises the buyer’s name, address, and contact details to ensure accurate delivery and payment processing.

- Invoice Date: This indicates the date when the invoice is issued, establishing the timeline for payment.

- Payment Terms: These outline the conditions under which the buyer is expected to make payment, including due date, acceptable payment methods, and any applicable late fees.

- Description of Goods or Services: Each item or service provided is listed along with its quantity, unit price, and total cost, allowing the buyer to verify the accuracy of the transaction.

- Subtotal and Taxes: The subtotal reflects the total cost of the goods or services before taxes, while any applicable taxes, such as sales tax or value-added tax (VAT), are itemized separately.

- Total Amount Due: This is the final amount owed by the buyer to the seller, including the subtotal, taxes, and any additional charges.

- Payment Instructions: Clear instructions are provided to guide the buyer on how to remit payment, including bank account details or online payment options.

Importance of Invoices

- Legal Document: An invoice serves as a legally binding record of the transaction, providing evidence of the agreement between the buyer and the seller.

- Tracking and Accountability: It helps both parties keep track of their financial transactions and ensures accountability for payments and deliveries.

- Cash Flow Management: Invoices facilitate efficient cash flow management for businesses by providing visibility into expected revenue and pending payments.

- Tax Compliance: Properly documented invoices are essential for tax compliance, enabling accurate reporting of sales revenue and tax liabilities.

What is a Statement?

A statement is a financial document that provides a summary of transactions over a specific period, a month, between a buyer and a seller. It serves as a record of all invoices, payments, and outstanding balances, offering a comprehensive view of the financial relationship between the parties involved.

Components of a Statement

- Account Information: The statement includes details such as the buyer’s account number, name, and contact information, along with the seller’s information for identification purposes.

- Statement Period: This indicates the timeframe covered by the statement, a month, allowing both parties to track transactions over a specific period.

- Transaction Summary: The statement provides a detailed summary of all transactions conducted during the statement period, including invoices issued, payments received, and any credits or adjustments applied.

- Invoice Details: Each invoice issued during the statement period is listed individually, including the invoice number, date, description of goods or services, and the total amount due.

- Payment History: The statement displays a record of all payments made by the buyer, showing the payment date, amount, and any outstanding balances carried forward from previous periods.

- Outstanding Balances: It highlights any outstanding balances owed by the buyer to the seller, including overdue payments from previous invoices, ensuring clarity on current financial obligations.

- Credits and Adjustments: Any credits or adjustments applied to the account, such as refunds or discounts, are documented in the statement to reflect accurate account balances.

- Total Amount Due: The statement calculates the total amount owed by the buyer to the seller, considering all invoices issued, payments received, and any outstanding balances, providing a clear picture of the buyer’s financial obligation.

Importance of Statements

- Financial Transparency: Statements offer transparency and accountability by providing a detailed summary of financial transactions between parties, helping to resolve discrepancies and disputes.

- Payment Reminders: They serve as effective payment reminders for buyers by highlighting outstanding balances and overdue invoices, encouraging timely payment.

- Budgeting and Planning: Statements assist both parties in budgeting and financial planning by providing insights into past transactions and forecasting future expenses and revenues.

- Auditing and Compliance: Properly maintained statements are essential for auditing purposes and ensuring compliance with accounting standards and regulatory requirements.

Main Differences Between Invoice and Statement

- Nature:

- Invoice: An invoice is a document issued by a seller to a buyer, detailing the specifics of a particular transaction, including the goods or services provided, quantities, prices, and payment terms.

- Statement: A statement is a summary of transactions over a period, a month, between a buyer and a seller, encompassing all invoices, payments, and outstanding balances.

- Purpose:

- Invoice: The primary purpose of an invoice is to request payment from the buyer for goods or services provided by the seller, serving as a formal record of the transaction.

- Statement: The main purpose of a statement is to provide a comprehensive overview of the financial relationship between the buyer and the seller, detailing all transactions and outstanding balances.

- Content:

- Invoice: An invoice includes header information, billing details, invoice date, payment terms, description of goods or services, subtotal, taxes, total amount due, and payment instructions.

- Statement: A statement comprises account information, statement period, transaction summary, invoice details, payment history, outstanding balances, credits and adjustments, and total amount due.

- Timing:

- Invoice: Invoices are issued by the seller to the buyer after a specific transaction has occurred, outlining the details of that transaction and requesting payment.

- Statement: Statements are generated at regular intervals, such as monthly, summarizing all transactions and financial activities between the buyer and the seller over that period.

- Function:

- Invoice: Invoices initiate transactions by specifying the details of a specific purchase and requesting payment from the buyer.

- Statement: Statements provide an overview of ongoing financial interactions between the buyer and the seller, facilitating transparency, tracking, and reconciliation of transactions.

This article is a valuable resource for businesses and individuals involved in financial transactions. It clarifies the finer details of invoices and statements.

Absolutely, Maria. The article’s meticulous approach in explaining the main differences is commendable.

The clarity of the article deserves recognition. It’s an essential read for those dealing with invoices and statements.

The article successfully conveys the essence of an invoice and a statement, shedding light on their distinctive characteristics.

Indeed, Greg. The article serves as a comprehensive guide for understanding these crucial financial documents.

The clear and concise explanation of invoices and statements in this article is a testament to its informative value.

The article provides a comprehensive explanation about invoices and statements. It’s very informative and helpful.

The comparison of intent between an invoice and a statement is quite enlightening.

I appreciate how the article delves into the accounting effects of invoices and statements.

The article is an excellent resource for anyone seeking to understand the fundamental disparities between invoices and statements.

The detailed comparison table is a highlight of this article. It succinctly summarizes the disparities between an invoice and a statement.

I couldn’t agree more, Nick. The comparison table effectively delineates the key contrasts between the two.

The article elucidates the nuances between invoices and statements, providing a thorough understanding of their respective roles in business transactions.

The article’s clear differentiation between the two documents is commendable, and it serves as a valuable educational resource.

I found the tone of the article to be quite formal and serious, but it effectively communicates the distinctions between invoices and statements.

The discussion of scope and time period in the comparison of invoices and statements is thought-provoking.

I agree, Joel. The article raised compelling points that prompt further introspection.

The article’s attention to detail in explaining the nuances of an invoice and a statement is commendable.

This article clearly distinguishes the differences between an invoice and a statement. It provides valuable information for those involved in business transactions.

I found the comparison table very useful, it simplifies the information for better understanding.

I agree, the article does a great job at explaining the key differences between the two.

I think the article lacks real-life examples to illustrate the differences. It would make the content more relatable.

I see your point, Matilda. Real-life examples could definitely enhance the article’s clarity.