Short-term loans have a shorter repayment period, within a year, with higher monthly payments but lower overall interest costs. In contrast, long-term loans offer extended repayment periods, several years, resulting in lower monthly payments but higher total interest expenses over the loan term. The choice between short and long-term loans depends on the borrower’s financial goals and ability to meet varying payment structures.

Key Takeaways

- Short-term loans are loans with a repayment period of up to one year, while long-term loans have repayment periods extending beyond one year, spanning several years or even decades.

- Short-term loans are used for temporary cash flow needs, such as working capital or emergency expenses. In contrast, long-term loans are used for larger investments or long-term projects, such as business expansion or purchasing a home.

- Interest rates for short-term loans are higher than long-term loans due to the increased risk associated with shorter repayment periods.

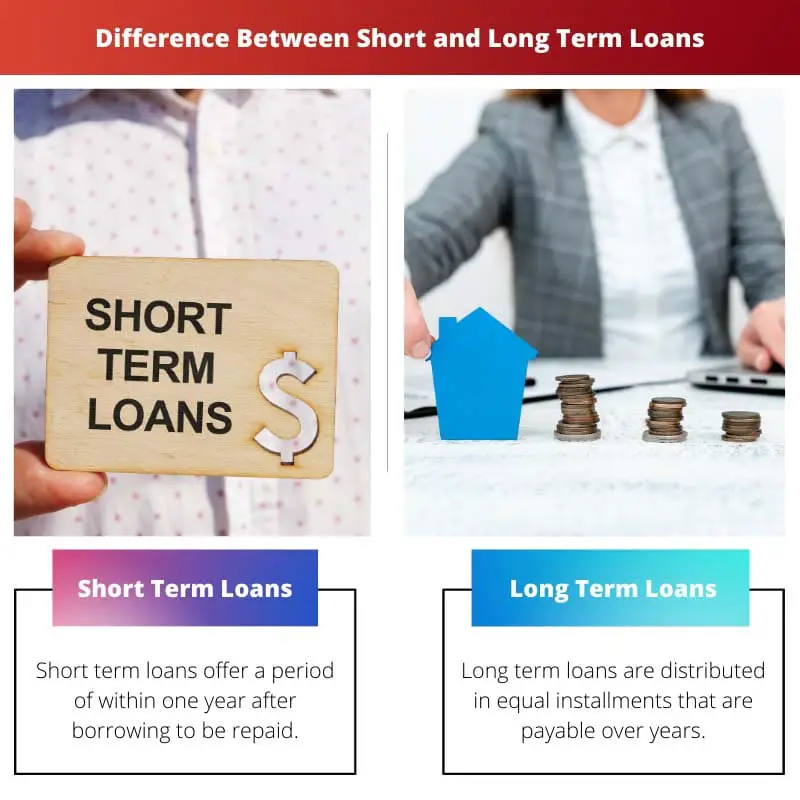

Short vs Long Term Loans

The difference between Short Term and Long Term loans is the amount of time required to repay the funds borrowed.

This means Short Term Loans are issued and repaid within a short time frame, within one year, while Long Term Loans, upon borrowing, are paid back over the years. The period varies from over one year up to even 30 years, depending on the type of loan.

Comparison Table

| Feature | Short-Term Loan | Long-Term Loan |

|---|---|---|

| Loan Term | Up to 3 years, less than 1 year | Over 1 year, 3-30 years |

| Loan Purpose | Emergency expenses, unexpected costs, small business needs, debt consolidation | Buying a home, car, major equipment, educational costs, investments |

| Loan Amount | Smaller amounts, under $25,000 | Larger amounts, depending on the type of loan |

| Interest Rates | Higher interest rates due to shorter repayment period | Lower interest rates due to longer repayment period and perceived lower risk |

| Repayment Plan | Fixed monthly payments over a shorter period | Fixed monthly payments over a longer period, resulting in smaller payments |

| Application Process | Generally faster and easier to qualify | More complex and may require collateral |

| Credit Requirements | Less stringent credit requirements, although approval depends on lender | stricter credit requirements and higher credit score needed |

| Flexibility | Less flexible in terms of use and repayment options | More flexible repayment options available in some cases |

| Fees | May have origination fees, late fees, and other charges | May have origination fees, appraisal fees, and other charges |

| Examples | Personal loans, payday loans, lines of credit, credit card cash advances | Mortgages, auto loans, student loans, business loans |

What is Short Term Loan?

Short-term loans are financial instruments with a brief repayment period, spanning from a few weeks to a year. These loans are designed to address immediate financial needs, offering a quick injection of capital. Understanding the key features, advantages, and considerations associated with short-term loans is crucial for individuals and businesses seeking temporary financial solutions.

Key Features of Short-Term Loans:

- Duration:

- Short-term loans have a brief repayment window, distinguishing them from longer-term financing options. The shorter timeframe is beneficial for borrowers who require immediate funds and intend to repay the loan quickly.

- Loan Amounts:

- Short-term loans provide smaller amounts compared to long-term loans. Lenders assess the borrower’s creditworthiness and financial stability when determining the loan amount, ensuring it aligns with the borrower’s ability to repay within the short timeframe.

- Interest Rates:

- While short-term loans may have higher interest rates compared to long-term loans, the overall interest cost tends to be lower due to the shorter repayment period. Borrowers should carefully evaluate the interest rates to gauge the affordability of the loan.

Advantages of Short-Term Loans:

- Quick Access to Funds:

- Short-term loans offer a rapid approval process, providing borrowers with timely access to the funds they need. This speed is crucial for addressing urgent financial situations or seizing immediate business opportunities.

- Flexibility:

- These loans offer flexibility in terms of purpose. Borrowers can utilize short-term financing for various needs, such as covering unexpected expenses, managing cash flow gaps, or taking advantage of time-sensitive business initiatives.

- Less Interest Expense:

- Despite higher interest rates, the total interest paid on short-term loans is lower than that of long-term loans. This makes short-term financing cost-effective for borrowers who prioritize minimizing interest expenses.

Considerations When Opting for Short-Term Loans:

- Monthly Repayment Obligations:

- Short-term loans require higher monthly repayments compared to long-term loans. Borrowers must assess their cash flow and ensure they can meet these obligations without straining their finances.

- Impact on Cash Flow:

- While short-term loans can address immediate financial needs, borrowers must consider the potential impact on their overall cash flow. It’s essential to evaluate how the loan will influence day-to-day operations and long-term financial stability.

- Qualification Criteria:

- Lenders have stringent qualification criteria for short-term loans. Borrowers should be prepared to demonstrate their creditworthiness and provide necessary documentation to secure approval.

What is Long Term Loan?

Long-term loans are financial instruments characterized by extended repayment periods, exceeding one year. These loans are designed to provide borrowers with substantial capital for large-scale investments, such as real estate purchases, business expansions, or significant projects. Understanding the key features, advantages, and considerations associated with long-term loans is essential for individuals and businesses seeking extended financial support.

Key Features of Long-Term Loans:

- Extended Repayment Period:

- Long-term loans have a prolonged repayment duration, spanning several years. This extended timeframe allows borrowers to distribute the repayment over a more extended period, resulting in lower monthly installment amounts.

- Loan Amounts:

- Compared to short-term loans, long-term loans offer larger loan amounts. Lenders assess the borrower’s creditworthiness and the purpose of the loan to determine the appropriate funding level for substantial and strategic financial undertakings.

- Interest Rates:

- Long-term loans may have lower interest rates compared to short-term loans. While the total interest cost over the loan term can be higher due to the extended repayment period, the lower monthly payments make it more manageable for borrowers.

Advantages of Long-Term Loans:

- Lower Monthly Payments:

- The extended repayment period of long-term loans results in lower monthly installment amounts. This is advantageous for borrowers who need significant capital but prefer to manage their cash flow with more affordable monthly payments.

- Strategic Investments:

- Long-term loans are well-suited for strategic investments, such as acquiring real estate, expanding business operations, or funding projects with a substantial impact. The extended repayment period aligns with the long-term nature of these endeavors.

- Stability and Predictability:

- Borrowers benefit from the stability and predictability of long-term loans. Fixed interest rates and consistent monthly payments make it easier for individuals and businesses to plan and budget over an extended period.

Considerations When Opting for Long-Term Loans:

- Total Interest Cost:

- While monthly payments are lower, the extended repayment period may result in a higher total interest cost. Borrowers should carefully assess the overall cost of the loan and consider its impact on the project’s or investment’s profitability.

- Qualification Criteria:

- Long-term loans have stringent qualification criteria. Lenders may scrutinize the borrower’s credit history, financial stability, and the purpose of the loan. Meeting these criteria is crucial for securing approval.

- Commitment and Flexibility:

- Committing to a long-term loan requires careful consideration of the borrower’s financial stability and long-term goals. While the extended repayment period provides stability, it may limit flexibility for changes in financial strategy or unforeseen circumstances.

Main Differences Between Short and Long-Term Loans

- Repayment Period:

- Short-term loans have a brief repayment period, within a year, while long-term loans feature extended repayment durations, spanning several years.

- Loan Amounts:

- Short-term loans provide smaller amounts compared to long-term loans, catering to immediate financial needs. Long-term loans, on the other hand, offer larger sums suitable for significant investments or projects.

- Interest Rates:

- Short-term loans may have higher interest rates, but the total interest cost is lower due to the shorter repayment period. Long-term loans may have lower interest rates, but the extended term results in higher overall interest expenses.

- Monthly Payments:

- Short-term loans require higher monthly payments, making them suitable for those capable of meeting immediate financial obligations. Long-term loans offer lower monthly payments, providing greater flexibility but leading to higher total interest costs.

- Purpose:

- Short-term loans are ideal for addressing urgent financial needs, managing cash flow gaps, or seizing immediate opportunities. Long-term loans are designed for substantial investments, such as real estate acquisitions, business expansions, or large-scale projects.

- Approval Criteria:

- Short-term loans may have less stringent qualification criteria, given the smaller loan amounts and shorter repayment periods. Long-term loans involve more thorough scrutiny of the borrower’s credit history, financial stability, and the purpose of the loan.

- Flexibility:

- Short-term loans offer quick access to funds, providing flexibility for addressing immediate financial challenges. Long-term loans provide stability and predictability but may limit flexibility for changes in financial strategy or unforeseen circumstances.

- Total Interest Cost:

- Short-term loans may have higher interest rates, but the overall interest cost is lower due to the shorter repayment period. Long-term loans may have lower interest rates, but the extended term leads to a higher total interest expense over the loan term.