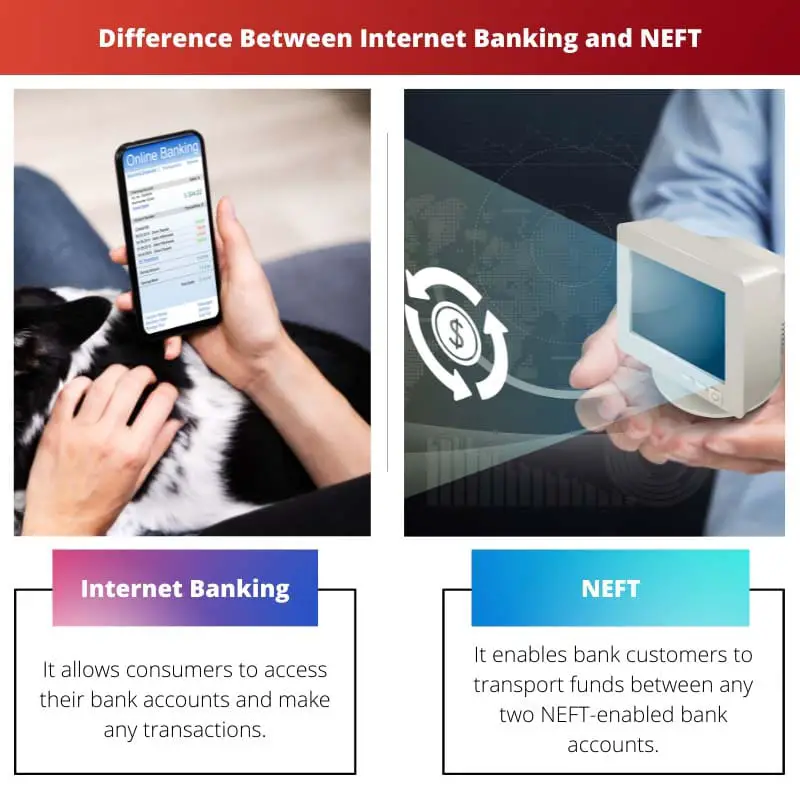

Internet Banking allows users to manage their accounts, transfer funds, and conduct various financial transactions online through a bank’s website or app. NEFT (National Electronic Funds Transfer) is a specific electronic funds transfer system in India that enables interbank transactions, typically requiring the sender and recipient to have accounts with participating banks.

While Internet Banking is a comprehensive platform, NEFT is a specific service for transferring funds between banks electronically.

Key Takeaways

- Banks offer Internet banking, which allows customers to conduct various financial transactions online, such as account management, bill payments, and fund transfers.

- National Electronic Funds Transfer (NEFT) is a specific electronic fund transfer system in India that enables interbank transfers with predetermined settlement cycles.

- Internet banking is a broader term that encompasses multiple online banking services, whereas NEFT is a specific type of fund transfer service within the Indian banking system.

Internet Banking vs NEFT

The difference between Internet banking and NEFT is that Internet banking is very effective for the customers as they do not need to go to the bank for numerous banking activities, and only after a few simple clicks is the job done while just sitting in the comfort of home. In contrast, NEFT provides the faculty to such people who do not have a bank account can also deposit their cash at the NEFT-enabled departments with instructions to transport funds using NEFT.

Internet Banking is the faculty to operate financial transactions through a safe and secure website, whereas NEFT is an electronic fund transfer system in which dealings are resolved in assortments during specific timings.

Internet Banking allows the user to perform monetary transactions via the internet. It is moreover understood as online banking or web banking.

Through this, one can do the primary transfer of money i.e. the individual can transfer funds between accounts and compensate bills effortlessly at any time per their comfort.

NEFT, or National Electronic Funds Transfer, is upheld by the Reserve Bank of India and was launched in November 2005. It is a network through which funds are transferred electronically.

The Institute for Development and Research in Banking Technology organised and upheld the format.

Comparison Table

| Feature | Internet Banking | NEFT (National Electronic Funds Transfer) |

|---|---|---|

| Function | Overall online banking platform for various financial activities | Electronic funds transfer method for transferring money between bank accounts |

| Scope | More comprehensive | Specific to transferring funds |

| Activities | * Account balance checks * Money transfers (including NEFT, IMPS etc.) * Bill payments * Recharges * Investment management * Loan applications * And more | Transferring funds from one bank account to another (within India) |

| Transfer Speed | Varies depending on the type of transfer (NEFT, IMPS etc.) | Transfers are batched and processed periodically (usually within 2 hours) |

| Availability | 24/7 (depending on bank) | Working hours of banks participating in NEFT |

| Transaction Limits | Varies depending on the bank and type of transfer | Limits vary by bank, typically higher than NEFT |

| Charges | May have charges for certain transactions (e.g., money transfers) | May have charges for NEFT transactions (depending on bank) |

What is Internet Banking?

Advantages of Internet Banking

1. Convenience

Internet banking eliminates the need for physical visits to brick-and-mortar branches, enabling customers to access their accounts and perform transactions from the comfort of their homes or offices. This round-the-clock availability enhances convenience.

2. Time Efficiency

Traditional banking transactions often involve time-consuming processes. Internet banking streamlines these processes, allowing users to execute transactions swiftly, saving valuable time.

3. Accessibility

The ubiquity of the internet ensures that customers can access their bank accounts from anywhere globally. This level of accessibility is particularly beneficial for travelers or individuals residing in remote locations.

4. Cost Savings

Both customers and banks benefit from cost savings associated with internet banking. Customers can avoid travel expenses, and banks can reduce operational costs related to maintaining physical branches.

Core Features of Internet Banking

1. Account Management

Users can view their account balances, transaction history, and download statements. Account management features provide a real-time snapshot of financial activities.

2. Fund Transfers

Internet banking facilitates electronic funds transfer between accounts, both within the same bank and to external accounts at different financial institutions.

3. Bill Payments

Customers can pay utility bills, credit card bills, and other payments directly through the internet banking platform, streamlining the bill payment process.

4. Online Investments

Many internet banking platforms offer the option to invest in various financial instruments, such as mutual funds, stocks, and fixed deposits.

Security Measures in Internet Banking

1. Encryption

Internet banking platforms employ encryption techniques to secure the transmission of sensitive information, such as login credentials and transaction data.

2. Two-Factor Authentication (2FA)

To enhance security, banks often implement 2FA, requiring users to provide two forms of identification before accessing their accounts.

3. Secure Socket Layer (SSL)

SSL protocols ensure a secure and encrypted connection between the user’s device and the bank’s servers, safeguarding data during online transactions.

Challenges and Concerns

1. Security Risks

While security measures exist, internet banking faces ongoing threats from cybercriminals, including phishing attacks and malware.

2. Technological Barriers

Some users, especially in less technologically advanced regions, may face challenges in adapting to internet banking due to a lack of access to reliable internet or digital devices.

What is NEFT?

How NEFT Works

1. Initiation of Transaction

Customers who wish to transfer funds using NEFT initiate the process by providing details such as the recipient’s bank name, branch, account number, and the amount to be transferred.

2. Transaction Processing

- NEFT transactions are typically processed in batches at scheduled intervals throughout the day.

- The transactions are cleared and settled by the Reserve Bank of India (RBI), which acts as the intermediary between participating banks.

3. Settlement Cycle

- NEFT operates on a settlement cycle, and transactions are settled in hourly batches during the NEFT working hours.

- The settlement cycle ensures timely processing and completion of transactions.

NEFT Timings

1. Working Days

- NEFT transactions can be initiated on all working days, i.e., Monday to Friday.

- Saturdays are also available for NEFT transactions, with specific time slots.

2. Timing Slots

- NEFT transactions are typically processed in hourly batches, and customers need to initiate transactions within the specified time slots.

NEFT Charges

1. Transaction Fees

- Banks may levy charges for outward NEFT transactions, and the fees can vary across different banks.

- Some banks offer free NEFT transactions for certain account types or specific customer segments.

2. Service Charges

- Additional service charges may be applicable for certain value-added services related to NEFT transactions, such as immediate payment service (IMPS).

Advantages of NEFT

1. Convenience

- NEFT offers a convenient and paperless way to transfer funds between banks.

- Customers can initiate transactions from the comfort of their homes using online banking or visit the bank branch.

2. Safety and Security

- NEFT transactions are secure, with encrypted channels ensuring the confidentiality and integrity of the transferred data.

- The involvement of the RBI adds an extra layer of security to the entire process.

3. Widespread Availability

- NEFT is widely adopted by banks across India, making it accessible to a large number of customers.

Main Differences Between Internet Banking and NEFT

- Nature of Transaction:

- Internet Banking: It is a broader term that encompasses a range of financial activities conducted online, including but not limited to fund transfers. It involves managing various banking services through a bank’s website or mobile app.

- NEFT (National Electronic Funds Transfer): It is a specific electronic funds transfer system in India that facilitates one-to-one fund transfers between bank accounts.

- Scope of Services:

- Internet Banking: Offers a wide array of services such as account balance inquiries, bill payments, account management, and more, in addition to fund transfers.

- NEFT: Primarily focused on facilitating interbank electronic funds transfers. It is designed specifically for transferring funds from one bank account to another.

- Initiation of Transactions:

- Internet Banking: Users can initiate various transactions themselves, including fund transfers, without the need for a specific NEFT service. It’s a comprehensive platform for multiple banking activities.

- NEFT: Requires a specific initiation for fund transfers. Users need to provide beneficiary details, and transactions are processed in batches at set intervals.

- Real-time vs. Batch Processing:

- Internet Banking: Depending on the type of transaction, some activities may be processed in real-time, providing immediate results.

- NEFT: Operates in batches, with specific settlement periods during the day. Transactions may not be instantaneous and are subject to scheduled processing times.

- Applicability:

- Internet Banking: Globally applicable and offered by banks worldwide as part of their online services.

- NEFT: Specific to India and is a domestic funds transfer system within the country.

- Transaction Limits:

- Internet Banking: Transaction limits may vary based on the user’s banking relationship, account type, and the specific policies of the bank.

- NEFT: Typically, there are predefined transaction limits set by the Reserve Bank of India (RBI) for NEFT transactions.

- Costs:

- Internet Banking: The costs associated with using internet banking services vary and may include subscription fees or transaction charges, depending on the bank and the type of account.

- NEFT: Generally involves nominal charges, if any, for the fund transfer service.

- Accessibility:

- Internet Banking: Accessible 24/7 from any location with an internet connection.

- NEFT: Availability is subject to the operating hours of the NEFT system, and transactions may not be processed on bank holidays or outside specified hours.

The article does a great job of highlighting the benefits and drawbacks of internet banking, making it easier for readers to make an informed decision.

Definitely, understanding the pros and cons of online banking is crucial, and this article does a great job of that.

The detailed comparison of Internet banking and NEFT, including their service timings and transaction charges, helps readers make informed decisions.

Absolutely, the breakdown of differences in the operation of these services is a valuable addition to this article.

Understanding the nuances of online banking and fund transfers is made simpler with the precise details laid out in this article.

This article provides a detailed comparison of Internet banking and NEFT, offering a clear understanding of their respective services.

The article presents Internet banking and NEFT in a clear and concise manner, enabling readers to grasp the nuances of these financial services.

Indeed, the clarity and detail in discussing Internet banking and NEFT are commendable in this article.

The informative content of this article makes it a worthwhile read for anyone interested in understanding online banking and fund transfers.

This article effectively outlines the purpose and benefits of Internet banking and NEFT, delivering valuable knowledge about these services.

I agree, the article serves as an insightful resource for individuals seeking to comprehend the functionalities of online banking and fund transfers.

The inclusion of key features and advantages of Internet banking in this article adds depth to the understanding of this banking service.

This article offers a balanced view of the advantages and disadvantages of Internet banking, providing valuable insights for readers.

I appreciate the detailed exploration of the benefits and risks associated with Internet banking. It’s a well-researched piece.

The comprehensive analysis of the pros and cons of online banking in this article makes it an enlightening read.

The article effectively describes the features and drawbacks of Internet banking, offering a well-rounded perspective on the service.

This article provides a comprehensive overview of Internet banking and NEFT, outlining their differences and key features. Very informative!

It’s a very well-structured comparison and explanation of Internet banking and NEFT. A useful read for anyone interested in banking services.

I agree, this article is a great source of information on online banking and fund transfer services.

I find the comparison table between Internet banking and NEFT quite helpful, as it succinctly outlines the differences in key parameters.

Absolutely, the detailed comparison enables readers to grasp the distinctions between these banking services effectively.

The table is a useful visual aid that complements the textual information about Internet banking and NEFT in this article.