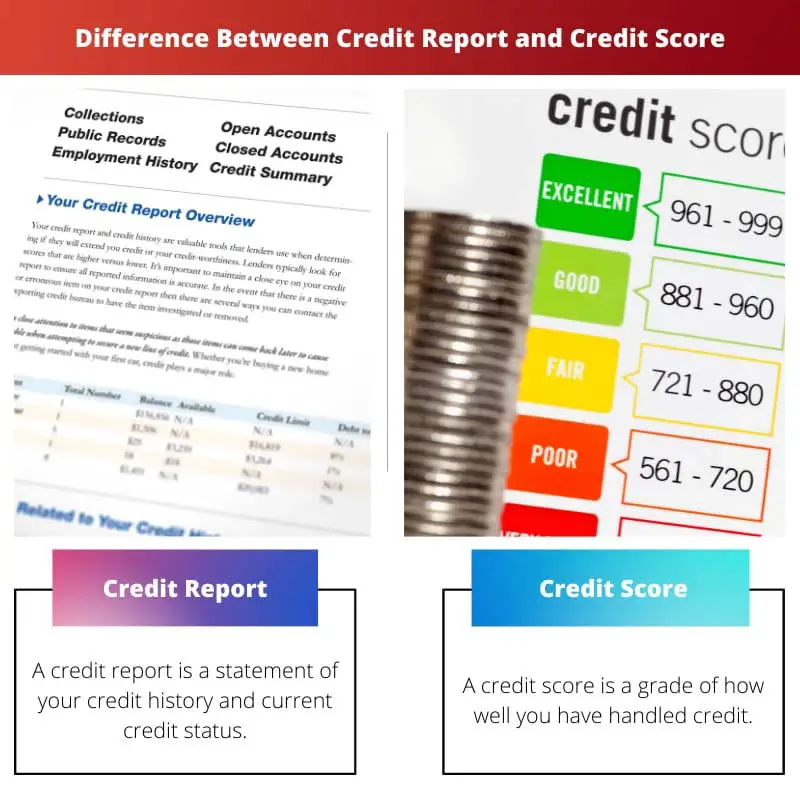

A credit report is a detailed record of a person’s credit history and financial activities. In contrast, a credit score is a numerical representation of an individual’s creditworthiness derived from the information in their credit report.

Key Takeaways

- A credit report is a detailed record of an individual’s credit history, including loans, credit cards, and payment behavior. In contrast, a credit score is a numerical representation of creditworthiness based on the information in the credit report.

- Credit reports are compiled by credit bureaus and contain personal, account, and inquiry information, whereas credit scores are calculated using credit scoring models, such as FICO or VantageScore.

- Lenders and creditors use credit reports and scores to assess an applicant’s risk and determine loan eligibility, interest rates, and credit limits.

Credit Report vs Credit Score

The difference between a Credit Report and a Credit Score is that a credit report is a report that shows the past history of all your payments, and a credit score is a number that evaluates your credit risk and whether you’re creditworthy or not for any loan. A credit report also includes all types of bank account and debts, credit score is evaluated through your credit file.

Furthermore, a credit report is the history of all credit activity and current credit. It includes public information from government entities as well as information from private companies.

A credit score summarizes your creditworthiness based on the credit report.

Comparison Table

| Feature | Credit Report | Credit Score |

|---|---|---|

| What it is | A detailed report of your credit history | A three-digit numerical summary of your creditworthiness |

| Information included | Payment history, credit accounts, balances, inquiries, public records, etc. | Based on information in your credit report |

| Purpose | To provide a comprehensive overview of your credit history | To provide a quick and easy way to assess your creditworthiness |

| Range | N/A | 300-850 (higher is better) |

| Impact on your credit | Errors or inaccuracies can negatively impact your credit score | Errors or inaccuracies can negatively impact your credit score |

| Who has access | You, lenders, creditors, and certain other authorized parties | You, lenders, creditors, and certain other authorized parties |

| How to obtain | You can request a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) annually | You can access your credit score through various websites and financial institutions |

| Cost | Free | There may be a fee to access your credit score |

| Updated frequency | Monthly | Monthly |

| Impact on credit applications | Lenders will review your credit report to make lending decisions | Lenders will use your credit score as a key factor in their lending decisions |

What is Credit Report?

A credit report is a detailed document that summarizes your borrowing history and financial obligations. It serves as a financial snapshot, providing lenders and other institutions with a comprehensive view of your creditworthiness. Think of it as your financial report card, showcasing how responsibly you have managed credit in the past.

Here’s a breakdown of its key features:

Information included:

- Payment history: This reveals how consistently you have made your loan and credit card payments on time.

- Credit accounts: This section lists all your open and closed credit accounts, including credit cards, loans, and mortgages.

- Balances: This shows the current balance of each of your credit accounts.

- Inquiries: This section lists any recent inquiries from potential lenders to your credit report.

- Public records: This section may include information about bankruptcies, liens, judgments, and foreclosures.

Purpose:

- To assess creditworthiness: Lenders use credit reports to determine your eligibility for loans, credit cards, and other forms of credit.

- To set interest rates and credit limits: The information in your credit report will influence the interest rate you pay on loans and the credit limits you are offered.

- To identify errors: Reviewing your credit report regularly can help you identify errors or fraudulent activity that could negatively impact your credit score.

Frequency and access:

- Updated monthly: Your credit report is updated monthly with the latest information from your creditors.

- Free access: You are entitled to an annual free credit report from each of the three major credit bureaus (Experian, TransUnion, and Equifax).

Impact on creditworthiness:

- Errors or inaccuracies can negatively impact your credit score: It’s crucial to review your credit report for any errors and dispute them if necessary.

- Payment history plays a significant role: Demonstrating a consistent history of on-time payments will positively impact your credit score.

What is Credit Score?

A credit score is a number that summarizes your creditworthiness. It’s a three-digit score ranging from 300 to 850, with a higher score indicating a better credit history and lower risk for lenders. Think of it as your financial grade, reflecting how likely you are to repay borrowed funds.

Here’s a closer look at its key features:

Purpose:

- Assesses creditworthiness: Lenders use credit scores as a key factor when deciding whether to approve you for loans, credit cards, and other forms of credit.

- Determines interest rates and credit limits: Your credit score significantly affects the interest rate you pay on loans and the credit limits you are offered.

- Predicts future credit behavior: The score helps lenders predict how likely you are to repay future loans based on your past credit history.

Factors influencing credit score:

- Payment history is the most significant factor, accounting for about 35% of your credit score. A consistent history of on-time payments can significantly boost your score.

- Credit utilization: This refers to the percentage of your available credit that you are currently using. Keeping your credit utilization ratio low (ideally below 30%) is important for maintaining a good score.

- Length of credit history: The longer your credit history, the more data lenders have to assess your creditworthiness. A longer history leads to a higher score.

- Credit mix: Having a mix of different types of credit, such as credit cards and installment loans, can demonstrate responsible credit management and positively impact your score.

- New credit inquiries: Applying for new credit can temporarily lower your score as it may suggest an increased risk of taking on more debt.

Benefits of a good credit score:

- Lower interest rates: You can qualify for lower interest rates on loans and credit cards, saving you money on interest payments.

- Better credit offers: You may be offered more favorable terms on loans and credit cards, such as higher credit limits and lower fees.

- Easier access to credit: A good credit score can make qualifying for loans and other forms of credit easier when needed.

Monitoring and maintaining your credit score:

- Review your credit report regularly: Check your credit report at least once a year to identify any errors or fraudulent activity that could negatively impact your score.

- Dispute errors promptly: If you find any errors on your credit report, dispute them with the credit bureau to correct them.

- Manage your credit utilization ratio wisely: Keep your credit utilization ratio low by paying down your credit card balances regularly.

- Make all your payments on time: A consistent history of on-time payments is crucial for maintaining a good credit score.

Main Differences Between Credit Report and Credit Score

A credit report and a credit score are related but distinct components of your financial profile that creditors and lenders use to assess your creditworthiness. Here are the main differences between a credit report and a credit score:

- Definition:

- Credit Report: A credit report is a detailed record of your credit history, including information about your credit accounts, payment history, public records, and inquiries. It provides a comprehensive view of your financial behavior.

- Credit Score: A credit score is a numerical representation of your creditworthiness based on the information in your credit report. It condenses your credit history into a single number.

- Contents:

- Credit Report: It lists all of your credit accounts (credit cards, loans, mortgages, etc.), records your payment history (including on-time and late payments), includes information about any public records (bankruptcies, tax liens, judgments), and shows inquiries made by creditors or lenders regarding your credit.

- Credit Score: A three-digit number ranges from 300 to 850 (the higher, the better). It is generated based on a mathematical algorithm that evaluates the information in your credit report and reflects your credit risk, with higher scores indicating lower risk.

- Purpose:

- Credit Report: Credit reports provide a comprehensive overview of your credit history to potential lenders, help creditors assess your creditworthiness and make lending decisions, and allow you to review your financial history for accuracy and identify areas for improvement.

- Credit Score: Credit scores simplify your credit history into a single number for quick assessment. Creditors use them to determine your credit risk and make lending decisions quickly. They may also be used by landlords, employers, and insurers for various purposes.

- Credit Reporting Bureaus:

- Credit Report: Credit reports are issued by major credit reporting bureaus, including Equifax, Experian, and TransUnion. You have a separate credit report with each bureau, which may contain slightly different information.

- Credit Score: Credit scores are generated by scoring models developed by companies like FICO or VantageScore. There are multiple versions and variations of credit scores, and they may vary based on the scoring model used.

- Access:

- Credit Report: You can request a free copy of your credit report from each of the three major credit bureaus once a year through AnnualCreditReport.com. You can also access your report for free if you are denied credit or are a victim of identity theft.

- Credit Score: Credit scores are unavailable for free through the official credit report website. However, many financial institutions and credit monitoring services offer access to your credit score for a fee or as part of their services.

- Impact on Credit Decisions:

- Credit Report: Credit reports provide detailed information lenders use to make lending decisions. They offer insights into your credit history, payment behavior, and potential risk factors.

- Credit Score: Credit scores are the first tool lenders use to assess your creditworthiness. A high score can lead to more favorable loan terms, while a low score may result in higher interest rates or credit denials.

- Factors Considered:

- Credit Report: Credit reports contain all the data contributing to your credit score. Lenders may review specific aspects of your credit report, such as payment history, outstanding balances, credit utilization, and derogatory marks.

- Credit Score: Credit scores are calculated based on various factors, including payment history, credit utilization, length of credit history, types of credit, and recent credit inquiries.

- Frequency of Updates:

- Credit Report: Credit reports are updated regularly, monthly, as creditors report your payment activity.

- Credit Score: Credit scores can be generated at any time using the data in your credit report, but they are updated less frequently, such as quarterly or when requested by a lender.

- Importance of Accuracy:

- Credit Report: Credit report accuracy is crucial, as errors can negatively impact your creditworthiness. Regularly reviewing your credit reports for inaccuracies is recommended.

- Credit Score: Credit score accuracy relies on the accuracy of the information in your credit report. Inaccuracies in your report can lead to an incorrect credit score. Reviewing and disputing inaccuracies in your credit report can help improve your score.

The comparison table effectively highlights the differences between credit reports and credit scores. It’s a valuable reference for consumers seeking clarity.

Absolutely, the ease of access to credit reports and scores is crucial in fostering financial responsibility and awareness.

Definitely, the clear breakdown of information empowers individuals to take control of their credit health.

The comprehensive overview of credit reports and credit scores is exceedingly helpful. It provides clarity on complex financial concepts.

The difference between a Credit Report and a Credit Score is quite nuanced and misunderstood. Thank you for the detailed explanation!

I appreciate the clear distinction between the two. It’s crucial for consumers to understand their credit health.

Yes, this information is valuable and can help people make more informed financial decisions.

The impact of credit reports and scores on credit applications is crucial to understand, especially for those seeking loans or credit cards.

Indeed, knowledge of credit reports and scores empowers consumers to navigate the lending process more effectively.

The purpose and impact of a credit report and credit score on creditworthiness are well articulated. This clarity is invaluable for consumers.

I couldn’t agree more. Understanding credit reports and scores is essential for responsible financial management.

Absolutely, the distinction between the credit report and credit score profoundly impacts consumers’ financial well-being.

Understanding the nuances of credit reports and scores can significantly impact financial decision-making. This article provides valuable insights.

I completely agree. The information provided here is instrumental in promoting financial knowledge and responsibility.

Absolutely, the in-depth explanation enhances financial literacy and empowers individuals to make more informed choices.

The breakdown of the key features of credit reports and credit scores is informative and well-structured. It clarifies many misconceptions.

I agree, the comparison table provides a succinct overview, making it easier for readers to grasp the differences.

Indeed, shedding light on the impact of errors or inaccuracies on credit scores underscores the importance of maintaining accurate credit reports.

The impact of credit errors on credit scores is overlooked. This article emphasizes the importance of maintaining accurate credit reports.

Absolutely, vigilant monitoring of credit reports is vital for protecting one’s credit health and financial well-being.

Indeed, raising awareness about the implications of credit errors is essential for consumers to safeguard their financial stability.

The availability of a free annual credit report is reassuring. It ensures individuals can monitor their credit health without financial barriers.

Absolutely, financial literacy is essential, and access to credit reports is a step in the right direction.

The detailed explanation of what constitutes a credit report and a credit score is immensely beneficial. This knowledge is indispensable for financial management.

Absolutely, the frequency and access to free credit reports contribute to greater financial literacy and responsibility.

I appreciate the comprehensive overview provided. Understanding credit health is integral to making informed financial decisions.