Taking loans can be highly helpful for people when they are in need. But lately, it can convert into a severe headache, too, If the loans are not paid in time or the debt continues to rise.

The majority of people make use of credit cards for small loans. However, later the debt becomes piled up and caused financial distress and disaster. Two ways can help you if you have a lot of credit card debt. The first is credit card refinancing, and the other is debt consolidation.

Key Takeaways

- Credit card refinancing transfers the high-interest debt to a lower-interest card, while debt consolidation combines multiple debts into a single loan with a fixed interest rate.

- Credit card refinancing requires a good credit score to qualify for lower-interest cards, whereas debt consolidation loans may be available to those with lower credit scores.

- Debt consolidation simplifies debt management with a single monthly payment, while credit card refinancing demands careful planning to avoid incurring additional debt.

Credit Card Refinancing vs Debt Consolidation

Credit Card Refinancing comes with a 0% interest rate, which expires in 12-18 months. If you don’t pay off your debt by then, you must pay 16-20% interest along with the transfer fee. Debt consolidation loan comes with interest between 4%-36%, depending on your credit score or collateral.

Only one credit card or loan can be refinanced when refinancing credit cards. When it comes to credit card refinancing, the typical annual percentage rate, or APR, fluctuates depending on the amount of debt owed.

In the case of credit card refinancing or debt transfer deals, there is almost no set repayment period. Credit scores range from good to exceptional for credit card refinancing.

Debt consolidation is the process of combining several debts into a single larger debt. The average annual percentage rate for debt consolidation is 16.13%. In the event of debt consolidation, the repayment period is set between five and twenty years, and it is agreed upon with trustworthy lenders.

A lump-sum payment or a large amount is given or paid to the borrower in the case of debt consolidation, and some lenders can pay the creditors directly.

Comparison Table

| Parameters of Comparison | Credit Card Refinancing | Debt Consolidation |

|---|---|---|

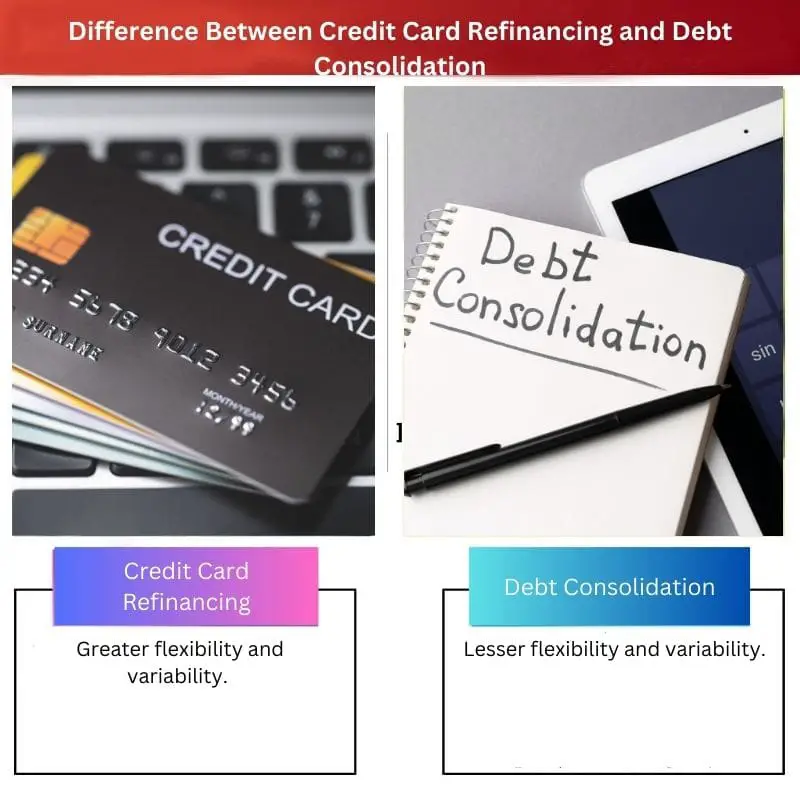

| Flexibility and variability | Greater flexibility and variability. | Lesser flexibility and variability. |

| Characteristic | Only one credit card loan can be taken care of. | All the debts are merged. |

| Average APR | Varies | 16.13% |

| Repayment time | Not fixed. | Fixed from 5-20 years |

| Credit score | Good- excellent. | Good- excellent. |

| Funding of loans | Transferring the balance of the amount into a new card. | Lumpsum amount is paid to the borrower. |

What is Credit Card Refinancing?

If the loans are not paid on time or if the debt grows. Credit cards are commonly used for minor loans by the majority of people. Debt, on the other hand, accumulates over time, resulting in financial trouble and calamity. Refinancing the credit card is simply a way to pay your debt.

In comparison to debt consolidation, credit card refinancing provides more flexibility and versatility. Only one credit card or loan can be refinanced with credit card refinancing. In the case of credit card refinancing, the average annual percentage rate, or APR, ranges from one debt amount to the next.

In the case of credit card refinancing or debt transfer programmes, there is almost no set repayment period. To refinance a credit card, you’ll need decent to excellent credit. In the case of credit card refinancing, the loan is funded by moving the balance of the amount into a new card.

What is Debt Consolidation?

In comparison to credit card financing, debt consolidation has a lower level of unpredictability and flexibility. Debt consolidation is the process of combining various debts into a single larger debt. In the case of debt consolidation, the annual percentage rate is set at 16.13 per cent on average.

In the event of debt consolidation, the repayment period is set between five and twenty years, and it is agreed upon with reliable lenders. In the case of debt consolidation, your credit score should range from good to exceptional.

In the case of debt consolidation, the borrower receives a lump-sum payment or a large payment, and some lenders have the option of paying the creditors directly.

Main Differences Between Credit Card Refinancing and Debt Consolidation

- Credit card refinancing possesses greater flexibility and variability in comparison to the process of debt consolidation. On the other hand, Debt Consolidation possesses comparatively lesser variability and flexibility in comparison to credit card financing.

- In credit card refinancing, only one credit card or a loan can be refinanced. On the other hand, debt consolidation is all about merging one than one debt or multiple debts into one bigger debt.

- The average amount of the annual percentage rate or APR in the case of Credit card refinancing varies from one debt amount to another. On the other hand, in the case of debt consolidation, the average amount of the annual percentage rate is fixed at 16.13%.

- There is almost no fixed repayment time in the case of credit card refinancing. On the other hand, the repayment time fixed in the case of debt consolidation is around five to twenty years, which is fixed with lenders of credible partners.

- The credit needed in case of credit card refinancing is from good to excellent. On the other hand, the credit score in the case of debt consolidation should also be from good to excellent.

- The mode in which the loan is funded in the case of credit card refinancing is by transferring the balance of the amount into a new card. On the other hand, In the case of Debt Consolidation, a lump sum amount or a heavy amount is sent or paid to the borrower, and some lenders have the option to pay the creditors directly.

- https://search.proquest.com/openview/03d503844566daf8a99daa434b4ec976/1?pq-origsite=gscholar&cbl=4849

- https://www.consumerinterests.org/assets/docs/CIA/CIA2002/hogarth-hilgert_financial%20knowledge.pdf?fbclid=IwAR1QROKqWoFdyTMZye3Q-4cazaxg06wTxPehfahmS1nj–YPpfROLSagBVY

Last Updated : 11 August, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The distinctions between credit card refinancing and debt consolidation are crucial in understanding the implications of each method when managing credit card debt. This information is beneficial for making well-informed decisions.

Absolutely, understanding these differences contributes to making informed choices regarding the most suitable approach to managing credit card debt effectively.

The distinction between credit card refinancing and debt consolidation when it comes to flexibility, repayment time, and funding of loans is a key factor in optimizing the management of credit card debt. Understanding these differences is crucial.

Absolutely, the specifics highlighted regarding the discrepancies between credit card refinancing and debt consolidation are essential for individuals looking to address their credit card debt effectively.

The explanations of both credit card refinancing and debt consolidation are highly detailed and informative, providing clarity on the nuances of each method and their implications for managing credit card debt.

The detailed descriptions of credit card refinancing and debt consolidation are enlightening and offer valuable insights for individuals seeking to address their credit card debt effectively.

Indeed, being well-informed about the differences between credit card refinancing and debt consolidation is essential. It’s crucial knowledge for individuals grappling with credit card debt.

It is important to understand that obtaining loans can lead to serious financial problems if not handled properly. It’s essential to be well-informed about different ways to manage credit card debt effectively.

I completely agree. Financial education is crucial and understanding the intricacies of debt management is essential for maintaining sustainable financial health.

The detailed comparison between credit card refinancing and debt consolidation serves as a valuable resource for individuals looking to gain a comprehensive understanding of the options available for managing credit card debt.

Thank you for providing such detailed insights into credit card refinancing and debt consolidation. This knowledge is indispensable for individuals seeking effective strategies to handle their credit card debt.

I completely agree. This detailed comparison provides vital information for making informed decisions about addressing credit card debt and working towards financial well-being.

The detailed expositions on the intricacies of credit card refinancing and debt consolidation are enlightening. They serve as a guide for those navigating through the complexities of managing credit card debt.

I appreciate the comprehensive breakdown of credit card refinancing and debt consolidation. These insights are invaluable for making informed decisions about managing credit card debt.

I couldn’t agree more. The comparisons provided are immensely helpful for those seeking to gain a comprehensive understanding of the available options for addressing credit card debt.

The comparison between credit card refinancing and debt consolidation provides a clear overview of the differences, aiding individuals in evaluating the best strategy for managing credit card debt and achieving financial stability.

I couldn’t agree more. This information is essential for individuals looking to make well-informed decisions about addressing their credit card debt.

Thank you for highlighting the nuances between credit card refinancing and debt consolidation. This knowledge is pivotal for developing effective strategies in managing credit card debt.

The comprehensive explanations of credit card refinancing and debt consolidation offer valuable insights into the dynamics of managing credit card debt, empowering individuals to make informed choices.

Absolutely, being well-informed about credit card refinancing and debt consolidation is vital for effectively addressing credit card debt and taking the necessary steps to achieve financial stability.

The detailed comparison between credit card refinancing and debt consolidation helps shed light on the pros and cons of each method. It’s valuable information for anyone dealing with credit card debt.

Absolutely, having a clear understanding of the options available can be beneficial to make informed decisions regarding managing debt.

The comparison table provided assists in gaining a better understanding of the nuances between credit card refinancing and debt consolidation. It’s informative and insightful for individuals struggling with credit card debt.

Thank you for emphasizing the importance of understanding the differences between credit card refinancing and debt consolidation. This knowledge is fundamental to effectively managing debt and improving financial stability.

Indeed, the details presented are essential for evaluating the best approach to tackle credit card debt and make the right financial decisions.