Accounting is a complex topic that has to consider various time periods and concepts to keep track of financial transactions both in cash and in credit.

Accrual and deferral concepts are used for dealing with accumulating and future transactions that have to be kept in mind while making deals.

Key Takeaways

- Accruals are accounting adjustments for revenues earned or expenses incurred but not recorded or paid, ensuring financial statements align with the accrual accounting method.

- Deferrals occur when a business receives or pays cash for transactions that will be recognized as revenues or expenses in future accounting periods.

- Accruals help match revenues and expenses to the appropriate period, while deferrals postpone the recognition of certain transactions to reflect their economic impact accurately.

Accruals vs Deferrals

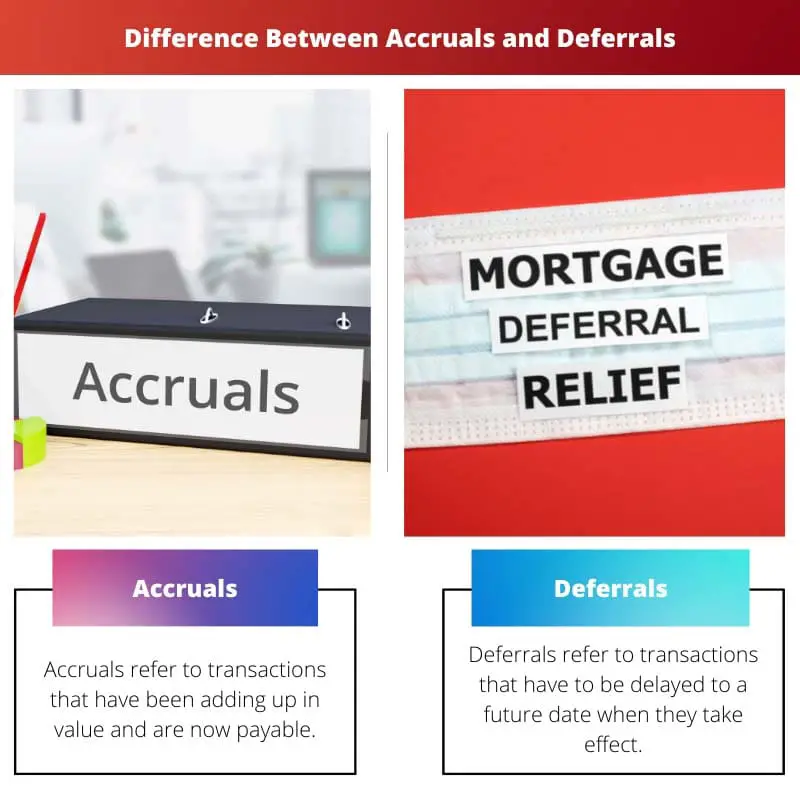

Accruals are transactions that have been earned or incurred but have not yet been recorded. Deferrals are transactions that have been recorded but have not yet been earned or incurred. Accruals are revenue earned but not yet received, while deferrals are liabilities recorded but not yet incurred.

The accrual concept in finance refers to the practice of recording transactions when they are made instead of when they are paid for. Accruals involve adding together sums over a period of time until they are paid for.

Accrued income refers to income for which work has been done but payment is left.

Deferrals refer to the incomes or expenses that have to be carried forward to the future and paid later even if they are having an effect in the present.

These also add sums over a period and they will become due in the later accounting periods. Taxes are deferrals in nature because they add on and become payable at the end of the year.

Comparison Table

| Parameters of Comparison | Accruals | Deferrals |

|---|---|---|

| Meaning | Accruals refer to transactions that have been adding up in value and are now payable. | Deferrals refer to transactions that have to be delayed to a future date when they take effect. |

| Nature | Accruals are based on the prudence concept of accounting where expenses are considered but incomes are not. | Deferrals emphasize the cash aspect of accounting where even if payment is received, recording is done when work is done. |

| Accounting Treatment | These are recorded in the current period and are due beforehand. | These will be recorded in the next accounting period. |

| Analogy | If a person takes a loan then he doesn’t pay interest immediately but later on. | If advanced payments are received by a firm for work not supplied then it is recorded later when work is done. |

| Examples | Credit Purchases, Taxes, Rent in advance, and Interest on loan. | Deferred revenue expenditures, Advertisements, and Subscription-based services. |

What is Accruals?

Accruals refer to incomes or expenses that have been accumulating over time and which have become due in the current accounting period.

This is done so that accounting transactions that have been accumulating and payments that are outstanding can be closed at the end of the accounting period.

An explanation of accruals can be given through accrued income, which refers to the income for which the work has been done but which has not yet been credited to the worker’s account. It is due to them and will be paid in the accounting period.

Accruals are considered because they affect the position and business of a company even though money has not been exchanged since work is actively involved and stock transfer might also be involved in the transaction.

They are necessary to keep track of financial activities which otherwise would be ignored due to lack of cash transfer.

Accruals function under the accrual concept of accounting which states that incomes and expenses are recorded in the books of accounts irrespective of the fact whether payment has been made in their regards or not.

They are cleared by paying or receiving payment at the end of the accounting period or contract.

What is Deferrals?

Deferrals refer to the transactions which although have taken place in the present time but will be recognized at some date in the future which depends upon the business.

They are made so that the financial statements being publicized by the business are more accurate in representing their financial and overall situation.

Deferrals are the payments received in advance that will affect the business in the future therefore they aren’t included in the current year.

It also includes expenses that have been paid for but which have not become due in the current period. They facilitate accurate tracking of payments by limiting them to the time they are actually made or received.

An example of a deferral would be prepaid rent in which case the rent has not become due in the present time but a tenant pays it prematurely. This is a deferral for the landlord since he hasn’t lent the service of his house but still received the money.

Deferrals also function under the accrual concept of accounting and facilitate accurate maintenance of financial records since a receipt has to be noted even if work is still due and it will be brought into term later.

Other examples of deferrals include subscriptions, product deposits, advanced income, prepaid bills, etc.

Main Differences Between Accruals and Deferrals

- Accruals refer to payments or incomes that have been carried forward to the present whereas deferrals refer to carrying incomes and expenses to the future.

- Accrued expenses refer to the payments that a company has to make in the present whereas deferred expenses refer to the expenses that have been paid in advance.

- Accrued incomes are the payments that are still to be received for work already done therefore they are assets whereas deferred incomes are received for undone work.

- In deferrals, money is exchanged first whereas in accruals, money is involved later and work is done first.

- Accruals lead to increase in assets and decrease in costs whereas deferrals lead to increase in liabilities and cost.

- https://www.elibrary.imf.org/view/journals/005/2009/002/article-A001-en.xml

- https://heinonline.org/hol-cgi-bin/get_pdf.cgi?handle=hein.journals/taxlr38§ion=21

Last Updated : 13 July, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The topic is complex but your detailed explanation makes it easier to understand. Great article!

Definitely. The comparison table is very effective in highlighting the differences between accruals and deferrals.

The article provides a comprehensive overview of accruals and deferrals, and how they contribute to accurate financial record-keeping.

Very informative article, especially for individuals looking to improve their understanding of accounting concepts.

This article effectively breaks down complex accounting concepts into understandable components. Well-written and insightful.

Absolutely, the information presented is crucial for a clearer understanding of accounting terminology and practices.

The comparison table was particularly useful in differentiating between accruals and deferrals. Great article!

I found the content to be quite helpful and well-presented. The examples provided add more clarity to the concepts.

The article offers detailed insights and the nature of accruals and deferrals, making it a valuable resource for those interested in accounting.

Indeed, the article effectively demonstrates the significance and implications of accruals and deferrals.

This is great information, thank you for presenting it in such a clear and concise manner.

Absolutely! The article is concise and helpful in understanding complex accounting concepts.