In today’s world, having health insurance and other plans, privileges, and provisions has become essential. Health issues are unavoidable.

Thus, these health insurance plans and savings accounts help save some money for unforeseen medical emergencies.

In such scenarios, plans and organizations such as HMO (Health Maintenance Organization), PPO (Preferred Provider Organization), EPO (Exclusive Provider Organization), and POS (Point of Service) come into existence.

Key Takeaways

- HSAs (Health Savings Accounts) are tax-advantaged savings accounts for medical expenses, whereas PPOs (Preferred Provider Organizations) are insurance plans with preferred provider networks.

- HSAs can be paired with high-deductible health plans, offering potential long-term savings, while PPOs provide more comprehensive coverage and may have higher monthly premiums.

- PPO plans allow for greater flexibility in choosing healthcare providers without referrals, whereas HSA plans require careful spending decisions based on available funds.

HSA vs PPO

A Health Savings Account (HSA) is a tax-advantaged medical savings account available to U.S. taxpayers who are enrolled in a high-deductible health plan. A Preferred Provider Organization (PPO) is a type of health insurance plan that offers more flexibility in choosing healthcare providers and does not require a primary care physician.

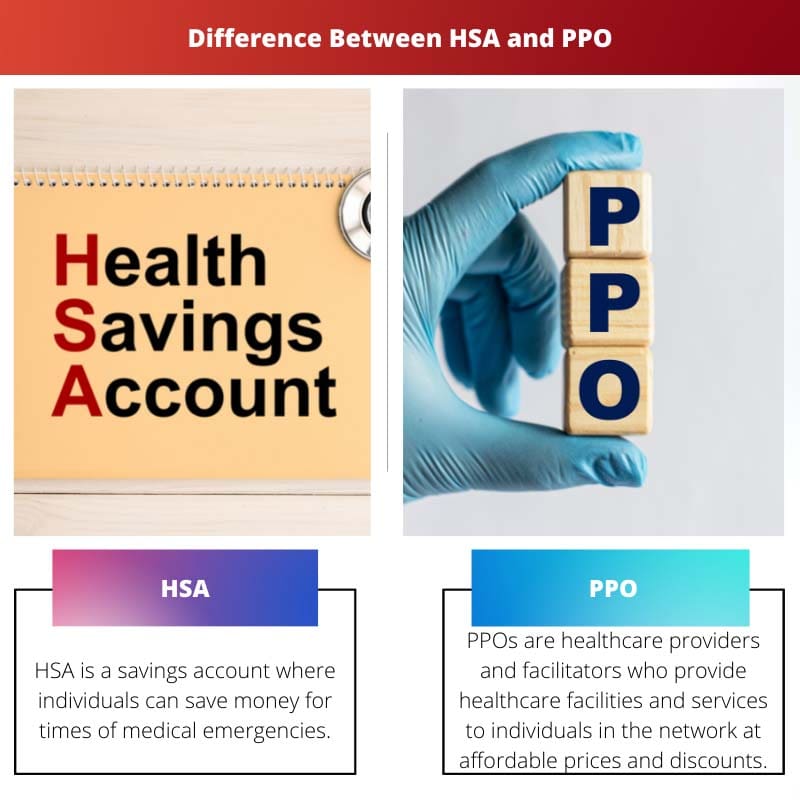

HSA is a savings account where individuals can save money for times of medical emergencies. All these accounts’ contributions, savings, and withdrawals aren’t taxable.

Moreover, in case of being unleft, the amount saved gets accumulated and rolls over to the upcoming years. A person with an HDHP plan can open an HSA account.

PPOs are healthcare providers and facilitators who provide healthcare facilities and services to individuals in the network at affordable prices and discounts.

Availing of the services within the network of PPA would cost low for an individual. Moreover, the expenses will be shared between healthcare providers and the individual.

However, if the person avails services and facilities outside the network of PPA, then the providers don’t bear the patient’s expenses.

Comparison Table

| Parameters of Comparison | HSA | PPO |

|---|---|---|

| Definition | HSA refers to a conventional savings account where an individual can save and manage their hospital expenses and gain healthcare insurance coverage under HDHPs. | PPO refers to the network of healthcare providers & facilitators offering health insurance plans just like HMOs. |

| Eligibility | An individual needs to be under the umbrella of HDHPs in order to own an HSA account. | Generally, employers offer PPO plans. Sometimes, individuals also purchase PPO plans from Healthcare.gov. |

| Provider Network | HSA is a savings account and thus has no provider network. It just acts like a savings fund, which an individual can use at any time. | PPO has a network of healthcare providers & facilitators where individuals can avail themselves of health care facilities with incentives and discounts. |

| Advantages | The advantages of HSA include:The contributions, withdrawals, and account management funds are non-taxable.HSA also has many investment potentials such as in stocks and investment funds such as mutual funds. | The advantages of PPO includes:It’s more flexible as you don’t need any kind of referrals or connections with PCP.It has a specialized network of healthcare providers & facilitators who offer discounts to eligible persons. |

| Disadvantages | The disadvantages of using HSA include:People who fall under any Medicaid or Medicare coverage aren’t eligible for HSA. Persons with HDHPs can only have an HSA.Sometimes, maintenance fees are even charged for the growth of the account. | The disadvantages of using PPO includes:The expenses included in monthly premium and out of pocket are high.Sometimes, PPO plans don’t include basic Medicare expenses. |

What is HSA?

HSA, standing for Health Savings Account, is a convenient savings account by which people can make some savings for handling their medical expenses well

and gaining medical insurance coverage under HDHPs (high-deductible health plans).

As HSAs fall under the ownership of individuals, they won’t stand taxable by federal income tax. Moreover, these funds stack up and get rolled over to the upcoming years when saved unused.

In order to be eligible for opening an HSA account, an individual needs to be under the umbrella of HDHPs (high-deductible health plans), where the government has some minimum deductible amount.

This deductible amount is updated in various years by the government. People who fall under any Medicaid or Medicare coverage aren’t eligible for HSA.

Moreover, people who are dependent on someone else’s tax returns are also not eligible to open an HSA.

HSAs over many tax advantages. Firstly, the contributions made through HSA are tax-deductible in cases where the individuals open the account themselves and are pre-tax in cases where the employer opens it.

Moreover, no taxes are levied on any withdrawals, deposits, or account maintenance. HSAs also help in reducing the tax burden as the funds deposited in HSAs are non-taxable.

HSA also has many investment potentials. People also invest funds of HSA in stocks and investment funds such as mutual funds.

What is PPO?

PPO, the acronym for Preferred Provider Organization, refers to some healthcare providers & facilitators offering health insurance plans just like HMOs (Health Maintenance Organizations).

PPOs have a connected network of healthcare providers and facilitators ranging from physicians to labs and therapists to hospital equipment providers and surgery centres.

When an individual uses the healthcare services to visit any of these healthcare providers falling under the network of PPO, he gets some incentives for his medical coverage.

Moreover, PPO also has the feature of cost-sharing, where these healthcare providers share half of the medical expenses.

This way, they keep individuals restricted to a group of specialized and top-skilled healthcare providers and help them financially in choosing the best medical service.

PPOs allow an individual to choose the medical health provider, proving to be more expensive than other managed health care options.

Moreover, in PPOs, the patient doesn’t need to be connected or have the referral of a PCP or a physician for primary care. In PPO, you don’t need any referral from a PCP or a PCP.

Moreover, it’s more flexible and has more control over your choices. However, there are some downsides to using PPO.

The expenses included in monthly premiums and out of pocket are also high.

Main Differences Between HSA and PPO

- HSA refers to a conventional savings account where an individual can save and manage their hospital expenses and gain healthcare insurance coverage under HDHPs. Whereas PPO refers to the network of healthcare providers & facilitators offering health insurance plans just like HMOs.

- An individual needs to be under the umbrella of HDHPs in order to own an HSA account. But, generally, employers offer PPO plans. Sometimes, individuals also purchase PPO plans from Healthcare.gov.

- HSA is a savings account and thus has no provider network. It just acts like a savings fund, which an individual can use at any time. On the other hand, PPO has a network of healthcare providers & facilitators where individuals can avail healthcare facilities with incentives and discounts.

- The contributions, withdrawals, and account management funds are non-taxable. HSA also has many investment potentials, such as in stocks and investment funds, such as mutual funds. On the other hand, PPO is more flexible as you don’t need any referrals or connections with PCP. Moreover, it has a specialized network of healthcare providers & facilitators who offer discounts to eligible persons.

- HSA has some minor disadvantages, such as people who fall under any Medicaid or Medicare coverage aren’t eligible for HSA. Persons with HDHPs can only have an HSA. Sometimes, maintenance fees are even charged for the growth of the account. On the other hand, The expenses included in PPO’s monthly premium and out of pocket are high. Sometimes, PPO plans also don’t include basic Medicare expenses.

Last Updated : 13 July, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The tone of the article is more on the formal side. A more light-hearted or comical approach could make the topic more engaging and interesting for readers.

This article provides a comprehensive breakdown of the differences and advantages of HSA and PPO. It’s nice to see such detailed information.

The arguments presented seem biased towards HSA, without thoroughly exploring the benefits of PPO. A more balanced approach would be appreciated.

While the content is informative, the article could use more practical examples to make it more relatable to the readers.

The sarcastic tone used in explaining the disadvantages of both HSA and PPO is quite amusing. It adds an element of humor to an otherwise technical subject.

Health insurance and savings accounts are indeed essential in this day and age. The information provided about HSA and PPO is quite thorough and insightful. Thanks for sharing!

I completely agree, Uadams. The detailed comparison between HSA and PPO is very informative. It clears up a lot of confusion!