Consumer-driven health care treats people through HSAs or MSAs but with high-deductible insurance coverage. This high-deductible coverage protects the policyholder from unexpected, catastrophic medical expenditures.

Several individuals with insurance do not understand the distinction between a Health Savings Account and a Medical Savings Account, even though there are significant distinctions between both plans.

Key Takeaways

- Both HSA and MSA are tax-advantaged savings accounts for healthcare expenses.

- HSA is available to individuals with high-deductible health plans, while MSA is only available to self-employed individuals and small businesses.

- HSA allows for higher contribution limits and rollover of funds from year to year, while MSA has lower contribution limits and does not allow rollover.

HSA vs MSA

HSA means health savings account and is an income savings account with tax advantages for individuals that are covered by high deductible health plans (HDHPs). MSA means medical savings account and is a tax-free income savings account used to pay for specific medical costs by eligible persons.

HSA is an abbreviation for Health Savings Account. It is the most used savings account for those with a high deductible health plan (HDHP).

Prior to the introduction of HSAs in 2003, individuals who were self-employed or engaged in small businesses may contribute to a similar kind of savings account known as an Archer Medical Savings Account (MSA), provided they were registered in an HDHP.

MSA is a full form of medical savings account. It is a health insurance plan with a $0 premium and a unique contribution that you may utilize for qualifying medical costs.

An MSA is a Medicare Advantage plan but is organized quite differently. The unique contribution made available to you for eligible medical costs is specific to the Medical Savings Account (MSA) and may alter yearly.

Comparison Table

| Parameters of Comparison | HSA | MSA |

|---|---|---|

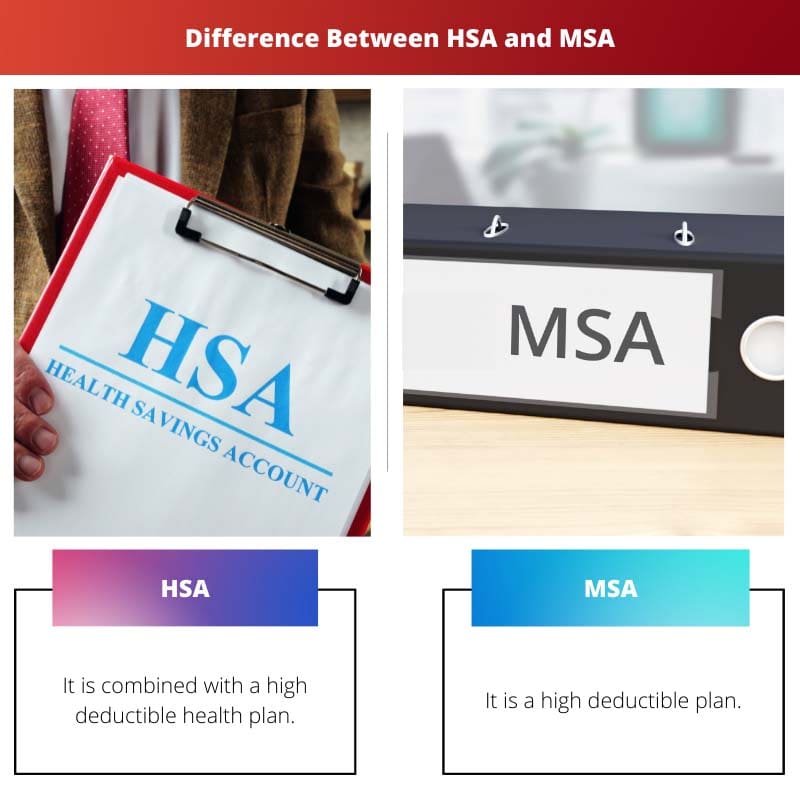

| Meaning | It is combined with a high-deductible health plan | It is a high-deductible plan |

| Contributions | Contributions to the account may be made by you or your employer. | The insurance agency makes a contribution to the account. |

| Eligibility | An HDHP is required. | Must be a Medicare beneficiary |

| Premium | There is a monthly fee for the HDHP. | There is no premium. |

| Operating | Most HDHPs have a network, such as an HMO or PPO plan. | There are no networks; you can see any doctor who takes Medicare. |

What is HSA?

A Health Savings Account (HSA) is an income, tax-advantaged savings account designed for those who receive their healthcare coverage via high-deductible health plans (HDHPs).

The individual or an organization makes regular payments to the account that can be used to pay for qualifying medical expenditures not reimbursed by the HDHPs.

Payments have an annual cap and could be used to pay for medical, dental, and eye care, as well as prescription drugs. An HSA is a savings account for individuals and families that are members of a high-deductible health plan (HDHP).

These can be obtained via both workplace and individual health insurance. They are accessible whether you are self-employed or employed by a corporation.

Most consumers who seem to have high-deductible medical insurance policies can establish an HSA. Typically, the two are linked together.

Qualified individuals who purchase their own coverage can create an HSA at certain banking institutions. Salary deductions are used by people who have employer-sponsored insurance coverage to fund their HSAs.

High-deductible health plans (HDHPs) feature larger yearly deductibles but lower healthcare costs than conventional health plans.

In other words, the monthly payments are cheaper, but the persons insured are accountable for their own medical expenditures up to a certain limit.

The financial value of an HDHP’s low-premium and high-deductible structure is dependent on your individual circumstances.

What is MSA?

Medical savings accounts are income savings accounts that may be used to pay for eligible medical costs by eligible individuals. The primary advantage of an MSA is that income utilized to help pay for qualifying medical expenditures is tax-free.

Archer MSAs and Medicare MSAs are the two primary forms of MSAs. Although Archer MSAs have been mostly tapered down and haven’t been accessible for new participants since 2007.

Individuals on Medicare have the opportunity of using a Medicare MSA. You can no longer participate in an HSA once you qualify for Medicare.

If you’re using a high-deductible Medicare Advantage Plan, you will not have to pay any premiums. As a direct consequence, you face larger deductibles and out-of-pocket expenditures upfront.

Your health insurance provider deposits payments into your Medicare MSA. You cannot contribute on your own. Those payments are made at the start of the year, but if you enter a plan later that year, you may receive delayed payments.

The concept behind a Medicare MSA is that you utilize the money in your account to spend on qualifying costs until your bill is paid. However, not all “qualifying” costs are deducted from your deductible.

Because your deductibles are greater than the amount you get in your fund, you may have to show up with cash on your own to cover a percentage of your expenditures.

Main Differences Between HSA And MSA

- HSAs must be used in conjunction with a high-deductible health plan (HDHP), whereas MSAs are a kind of HDHP.

- In HSA, you are the one who contributes to it or contributions from your job, or a mix of the two. However, in MSA, that money is paid to you. You and your employer cannot contribute to the account at the same time.

- The HDHP that you must have with your HSA will have a monthly fee. The MSA has a $0 premium.

- HDHPs are channel-based, which means you must see doctors inside the network. If you don’t, you’ll have to pay extra. Whereas you can use the MSA to see any doctor who takes Medicare and acknowledges new patients.

- Individuals who work will be a good match for the HSA. An MSA is a simple transition once they retire.

- https://europepmc.org/article/med/21348571

- https://jamanetwork.com/journals/jama/article-abstract/403187

Last Updated : 13 July, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The comparison table provided is very helpful in understanding the key differences between HSAs and MSAs. This approach to healthcare finance is complex, and this breakdown makes it easier to comprehend.

The information on the operating and main differences between HSAs and MSAs is enlightening. I appreciate the insights provided, as they contribute to a deeper understanding of these healthcare options.

The breakdown of HSA and MSA, along with their structures and how they operate, is well presented. This content is beneficial for individuals wanting to comprehend the nuances of healthcare savings accounts.

This is a comprehensive explanation of HSA and MSA. I appreciate the inclusion of the differences and eligibility criteria for both. It’s essential to have this knowledge when making decisions about healthcare coverage.

The distinction between HSA and MSA, as well as the specific details, is very informative. The in-depth analysis serves as a valuable resource for those interested in learning about these healthcare finance options.

The overview of the contributions, eligibility, and premiums associated with HSAs and MSAs is very informative. This will be beneficial to individuals who are considering these options for their healthcare needs.

The details provided on how HSAs and MSAs work, as well as the key differences between them, offer a clear understanding of these healthcare financing options. This article serves as a valuable resource for those seeking information on this topic.

I appreciate the detailed explanation of the difference between HSAs and MSAs. It’s important for individuals to understand the distinctions between these plans to make informed decisions about their healthcare coverage.