When we talk about resource management as well as cost allocation for ethereal assets, we take into account terms like; amortization and depletion.

Very commonly used by commerce and management field researchers, this term couple holds a lot of meaning in management and understanding of all types of resources.

This article looks into the deeper meaning as well as the differences between amortization and depletion, along with their usage in the real world.

Key Takeaways

- Amortization allocates an intangible asset’s cost over its useful life.

- Depletion refers to allocating the cost of a natural resource over its extraction period.

- Both methods are used to spread out the expense of an asset, but they apply to different types of assets: intangible and natural resources, respectively.

Amortization vs Depletion

Amortization is the allocation of the cost of an intangible asset across its useful life while depletion is the reduction in the value of a natural resource as its supply is extracted and utilised. The former applies to Intangible assets like patents, and the latter applies to tangible assets like coal mines.

Amortization is a very important accounting terminology that means lowering the cost or value of an intangible asset or resource throughout its shell life period.

It’s a very common practice in the accounting field of studies and is widely used by accountancy practitioners. It is partially similar to depreciation in physical assets.

To put it simply, amortization refers to lowering a loan or intangible debt in parts or phases while the asset is in its useful life period.

Depletion refers to the process in accounting when the net worth or value of a natural resource is reduced after its extraction and utilization for various uses.

Like amortization, depletion also is a non-cash expense as it lowers the value of a resource exponentially after its usage is progressed to the maximum. Depletion applies to all types of natural resources like coal, oil, timber, minerals, and metals.

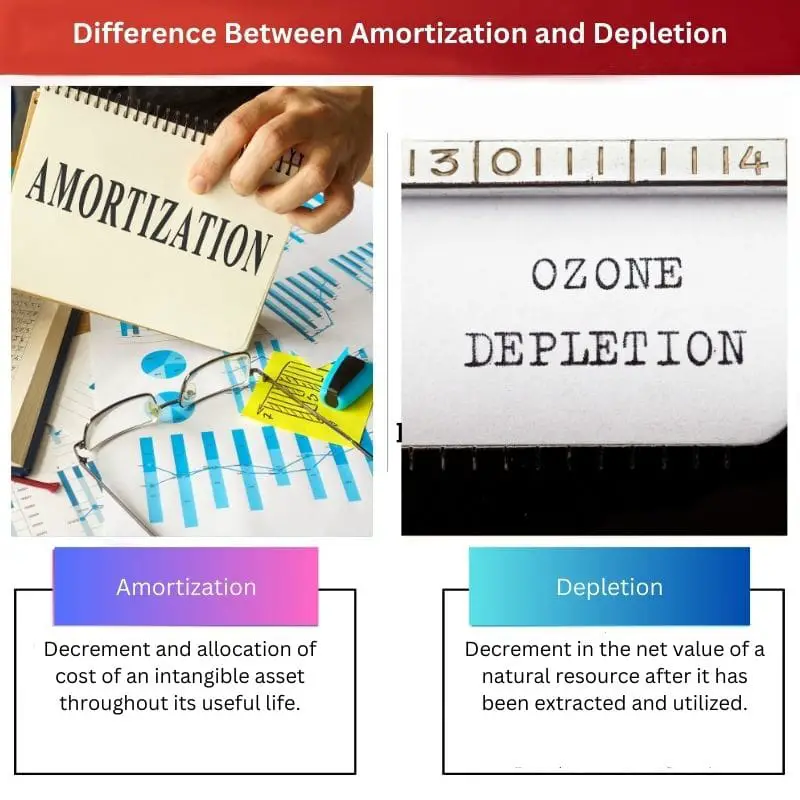

Comparison Table

| Parameters of comparison | Amortization | Depletion |

|---|---|---|

| Meaning | Decrement and allocation of cost of an intangible asset throughout its useful life. | Decrement in the net value of a natural resource after it has been extracted and utilized. |

| Asset type | Intangible assets like debts, loans and agreements. | Tangible natural resources like timber, coal, oil, mineral reserves etc. |

| Industry usage | Any industry that deals with intangible resources like loaning and business related organizations. | Industries which deal with usage of natural resources like mining industries, oil fields etc. |

| Basis of charge | Term of life and usage of the asset in terms of time in years or months. | Based on assessment and utilization and exhaustion of natural resources. |

| Formula | Total cost of the intangible asset/Useful life in years | Cost – salvage value/No. of units that can be extracted |

What is Amortization?

Amortization is a procedure used in the accounting and commerce field of business when the decrement and allotment of new costs are done for intangible assets.

Intangible assets are the assets that exist on paper only and cannot be touched physically example, loans, debts, and lend-over.

Amortization is commonly practised by money lending associations or loan-providing foundations to introduce the loan repayment schedule based on its date of maturation.

Banks commonly use this tactic to bring down the value of a debt, loan, or mortgage.

Sometimes an amortization technique is used for paying off debts and loans in due periodic slots (yearly or monthly).

An amortization schedule is used to make instalment payments on a loan, such as a mortgage or a car loan, to reduce the current balance.

To calculate the amortized cost of an intangible asset, we have to divide the ‘cost of the intangible asset’ by ‘number of useful years’.

Amortization is charged in a sequential manner, which means that the charge to profit and loss is similar to each year of its usefulness (calculated in terms of years).

One might ask the reason for this technique, and amortization is done because the shell life of intangible assets depends on its legal term value as well as economic value. Hence, amortization is only applicable to ethereal assets like loans and debts.

What is Depletion?

Depletion is a process in which the decrement of the value or cost of natural resources (exhaustible) is done to maintain its usage term life.

It is a non-cash expense process that simply decreases the net worth of natural, tangible resources according to their utilization and extraction.

When natural resource extraction costs are capitalized, they are systematically divided as well as categorized across different periods of time-based on the resources extracted and at the time they were utilized.

It is somewhat similar to the principle of amortization since both are non-cash expenses as well as both deal with the decrement of the cost of resources and assets (tangible and intangible, respectively).

Many factors influence the depletion of a natural resource, like; acquisition of the resource, exploration, development, and the restoration factor is primal for exhaustible natural resources.

To calculate the depletion value of a resource, one requires the cost of the resource, the salvage value of the resource, and the number of units that can be extracted in a unit of time.

These values give out the depletion value by using the formula: Cost – salvage value/No. of units that can be extracted.

Depletion is used because of the exhaustible factor of natural resources, and this also makes depletion an essential process in accounting.

Main Differences Between Amortization and Depletion

- Amortization is a procedure that is applicable to intangible assets, whereas depletion is applicable to tangible natural resources only.

- Amortization is for industries that deal with patents, warranties, loans, and other legalities, but depletion is practised by mining fields and oil-extracting companies.

- The year-on-year charge for amortization stays similar for intangible assets, whereas the year-on-year charge for depletion depends on the yearly number of units extracted (Natural resources).

- The formula for calculating amortization is; Total cost of the intangible asset/Useful life in years, and the formula for calculating depletion is; Cost – salvage value/No. of units that can be extracted.

- Amortizations are charged due to the limited legal window period of assets like loans, debts, and licenses, whereas depletions are charged because of the exhaustion and reformation rate of natural resources like timber, oil, and minerals.

Last Updated : 01 August, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The way the article describes amortization and depletion as non-cash expenses but crucial in cost allocation is quite enlightening.

The section on the application of depletion in natural resource industries was very well-presented.

I found the explanation of the formulae for amortization and depletion particularly insightful.

The distinction between intangible assets and tangible natural resources under amortization and depletion was well-explained.

The article truly delved into the depths of amortization and depletion, providing clarity on their complexities.

I found the comparison table to be a great visual summary of amortization and depletion differences.

The article was very informative and helpful in explaining the key differences and applications of amortization and depletion.

I agree, the article really simplified these complex accounting concepts.

The comparison table was especially useful in distinguishing between amortization and depletion.

The article effectively conveyed the importance of depletion and its impact on natural resource industries.

The relevance of the depletion process in maintaining the value of natural resources became very clear through the article.

The explanation of the process of depletion was particularly insightful, especially regarding its non-cash nature.

The amortization and depletion formulas provided a clear mathematical understanding of the processes, making them easier to grasp.

The use of formulas to explain amortization and depletion added a quantitative aspect to the article, enhancing its comprehensiveness.

The amortization schedule and its significance in loan repayments were well-described, making it easier to understand this concept.

I agree, the section on amortization schedules was very insightful and applicable to real-life scenarios.

The distinction between amortization for intangible assets and depletion for natural resources was articulated with great clarity in the article.

The article’s detailed explanation of amortization and depletion added a great deal of clarity to these complex concepts.

The clarity in differentiating between the applicability of amortization and depletion was truly commendable.

The amortization schedule and its relevance to the loan repayment structure were explained succinctly and effectively.

The impact of amortization on loan repayment schedules was thoroughly demonstrated in the article.

The practical implications of amortization schedules were very well-presented in the article.

It’s fascinating to see how amortization and depletion are utilized in different industries and for varied purposes.

The detailed explanation of amortization schedules and natural resource depletion made the article very comprehensive.

Definitely, the practical examples helped in understanding the real-world applications of these concepts.

The connection between legal term value and economic value in the context of amortization was elaborated quite effectively in the article.

The reasoning behind amortization due to legal and economic factors provided a comprehensive understanding of its necessity.