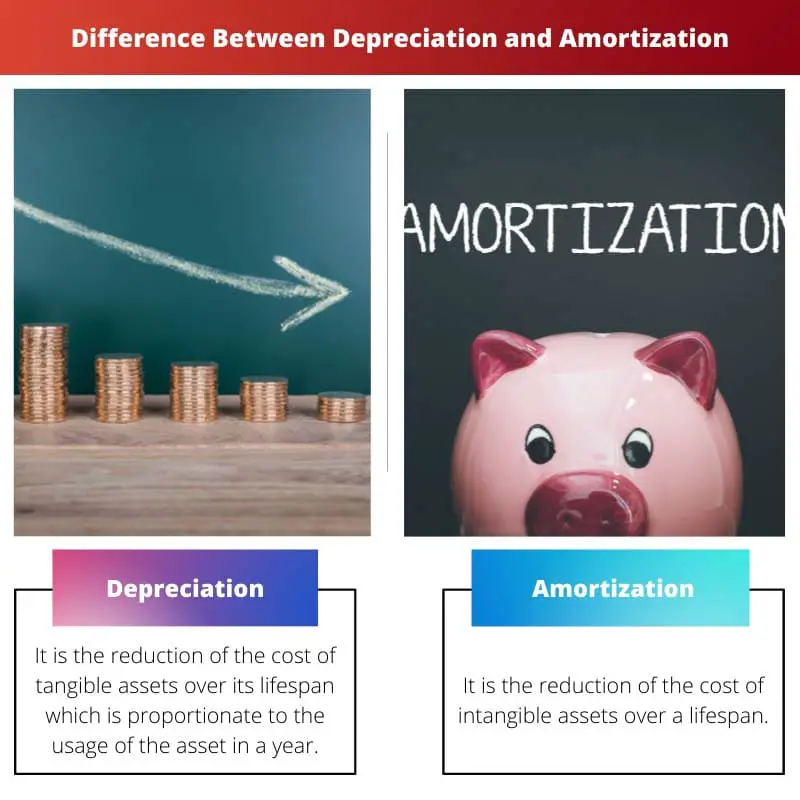

Depreciation is the allocation of tangible asset costs over its useful life, mainly for physical items like machinery. Amortization, on the other hand, is the gradual expensing of intangible asset costs, such as patents or copyrights, over their estimated useful life. Both methods aim to match expenses with the asset’s economic benefits.

Key Takeaways

- Depreciation is allocating the cost of a tangible asset over its useful life. At the same time, amortization allocates an intangible asset’s cost over its useful life.

- Depreciation applies to physical assets such as buildings, vehicles, and machinery, while amortization applies to intangible assets such as patents, copyrights, and licenses.

- Both depreciation and amortization are accounting methods used to allocate costs and reduce taxable income, but they apply to different types of assets.

Depreciation vs Amortization

Depreciation accounts for the decline in the value of tangible assets, such as machinery, equipment, and buildings, due to wear and tear or obsolescence. The asset’s cost is spread out over its useful life and recorded as a series of expenses on the company’s financial statements. Amortization accounts for the decline in the value of intangible assets, such as patents, copyrights, and trademarks. Similar to depreciation, the intangible asset’s cost is spread out over its useful life and recorded as a series of expenses on the financial statements.

Comparison Table

| Feature | Depreciation | Amortization |

|---|---|---|

| What it applies to: | Tangible assets: Physical assets that lose value over time, like buildings, machinery, equipment, furniture, vehicles. | Intangible assets: Non-physical assets with a finite useful life, like copyrights, patents, trademarks, software licenses, goodwill. |

| Purpose: | To recognize the expense of a tangible asset’s declining value over its useful life and match it to the revenue it generates. | To spread the cost of an intangible asset over its useful life and match it to the benefits it provides. |

| Calculation method: | Varies depending on the asset and tax regulations. Common methods include straight-line, double-declining balance, and sum-of-the-years’-digits. | Usually uses the straight-line method, spreading the cost evenly over the asset’s useful life. |

| Salvage value: | Considered in some depreciation methods, reducing the overall depreciable base. | Usually not considered in amortization, the entire cost is spread over the useful life. |

| Impact on financial statements: | Reduces both the asset’s value on the balance sheet and the company’s net income, creating a depreciation expense. | Reduces the intangible asset’s value on the balance sheet and creates an amortization expense on the income statement. |

| Tax implications: | Depreciation expenses are tax-deductible, reducing taxable income. | Amortization expenses are also tax-deductible, but rules may vary depending on the asset and jurisdiction. |

| Overall goal: | Accurately reflect the asset’s decreasing value over time and provide a realistic picture of the company’s financial health. | Ensure fair allocation of the intangible asset’s cost over its useful life and accurately match it to the benefits it generates. |

What is Depreciation?

Depreciation is an accounting method used to allocate the cost of a tangible asset over its useful life. It reflects the gradual decrease in the value of an asset as it is utilized in business operations.

Purpose:

- Expense Allocation: Depreciation allows businesses to spread the cost of an asset over several accounting periods, aligning expenses with the revenue generated by the asset.

- Asset Valuation: It reflects the true economic value of an asset on the balance sheet by accounting for its decreasing worth over time.

Methods:

- Straight-Line Method: Allocates an equal amount of depreciation expense each year, calculated as (Cost – Salvage Value) / Useful Life.

- Declining Balance Method: Front-loads depreciation, assigning higher expenses in the early years, using a fixed percentage of the remaining book value.

- Units of Production Method: Charges a varying amount based on the asset’s actual usage or output, ideal for assets whose wear and tear depend on production levels.

Examples:

- If a company purchases machinery for $50,000 with a useful life of 5 years and no salvage value, using the straight-line method, the annual depreciation expense would be $10,000 ($50,000 / 5).

- In the declining balance method, if the depreciation rate is 20%, the first-year expense would be $10,000 ($50,000 * 20%), and the next year’s expense would be based on the remaining book value.

Importance:

Depreciation is crucial for accurate financial reporting, tax deductions, and assessing the true cost of asset usage over time. It helps businesses make informed decisions regarding asset replacement, repair, or disposal.

What is Amortization?

Amortization is the process of spreading the cost of an intangible asset over its estimated useful life. This accounting method applies to assets like patents, copyrights, trademarks, and goodwill.

Purpose

Amortization aims to match the cost of intangible assets with the revenue they generate over time. It accurately reflects the economic benefits derived from the intangible asset in financial statements.

Calculation

The amortization amount is calculated using a systematic allocation approach, straight-line or another method reflecting the asset’s consumption pattern. The straight-line amortization formula is:

Amortization Expense = (Cost of Intangible Asset – Residual Value) / Estimated Useful Life

Where:

- Cost of Intangible Asset is the initial cost.

- Residual Value is the estimated value at the end of useful life.

- Estimated Useful Life is the anticipated period of economic benefits.

Financial Reporting

Amortization expenses are recorded on the income statement, reducing reported income. Accumulated amortization is reflected on the balance sheet, reducing the intangible asset’s carrying value.

Example

For a $100,000 patent with a 10-year useful life and no residual value, annual amortization expense is $10,000. This amount is recorded annually on the income statement until full amortization.

Main Differences Between Depreciation and Amortization

- Type of Assets:

- Depreciation: Applies to tangible assets like machinery, buildings, and vehicles.

- Amortization: Applies to intangible assets such as patents, copyrights, trademarks, and goodwill.

- Nature of Assets:

- Depreciation: Involves the wear and tear or physical deterioration of tangible assets over time.

- Amortization: Relates to the gradual expensing of intangible asset costs over their estimated useful life.

- Calculation Method:

- Depreciation: Calculated based on factors like cost, useful life, and salvage value, using methods such as straight-line or declining balance.

- Amortization: Calculated similarly, considering cost, useful life, and residual value, using straight-line amortization.

- Asset Examples:

- Depreciation: Includes assets like machinery, buildings, vehicles, and furniture.

- Amortization: Includes assets like patents, copyrights, trademarks, and goodwill.

- Physical vs. Non-Physical:

- Depreciation: Primarily linked to the physical deterioration or obsolescence of tangible assets.

- Amortization: Pertains to the allocation of costs for non-physical, intangible assets.

- Financial Statement Impact:

- Depreciation: Reduces the book value of tangible assets on the balance sheet and impacts the income statement.

- Amortization: Reduces the book value of intangible assets on the balance sheet and affects the income statement.

- Common Business Application:

- Depreciation: Commonly used in manufacturing, construction, and industries with significant tangible assets.

- Amortization: Frequent in industries dealing with intellectual property, brand development, and intangible assets.

- https://academic.oup.com/qje/article-abstract/69/2/191/1873131

- https://www.ebr.edu.pl/pub/2014_2_63.pdf

Last Updated : 11 February, 2024

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

This article does a great job of explaining the differences between depreciation and amortization, and how they are both crucial accounting methods for businesses. It’s a valuable resource for anyone looking to understand these concepts.

Absolutely, this article provides a comprehensive overview of depreciation and amortization, making it accessible for readers of all backgrounds.

I couldn’t agree more, Tony! The clear examples and detailed explanations make this complex topic much easier to understand.

The article’s breakdown of the purposes and methods of both depreciation and amortization provides a comprehensive understanding of these accounting practices for business professionals and individuals alike.

Indeed, the article’s focus on the implications of depreciation and amortization for financial statements enhances its relevance for readers interested in financial management and analysis.

I found the discussion on the impact of depreciation and amortization on financial statements to be particularly insightful, as it elucidates their significance in financial reporting and analysis.

The article’s detailed comparison and clear explanations of depreciation and amortization make it a valuable resource for individuals seeking to deepen their understanding of accounting principles and practices.

I couldn’t agree more, Jane. The comprehensive coverage of these accounting methods in the article offers a robust learning experience for readers.

Absolutely, the detailed explanations and structured approach of this article contribute to its effectiveness in imparting knowledge on depreciation and amortization.

The comparison between depreciation and amortization is presented in a clear and organized manner, making it easy for readers to grasp the distinctions between the two methods.

I completely agree, Olivia. The structured approach of this article enhances its value as an educational resource.

Yes, the cohesive layout of the comparison table and the subsequent detailed explanations contribute to the article’s effectiveness in conveying the differences between depreciation and amortization.

This post is quite informative and helpful for business owners and individuals who need to navigate the world of asset management and accounting methods. It lays out the key differences and purposes of depreciation and amortization clearly.

I found the comparison table particularly useful, as it succinctly outlines the different features of depreciation and amortization.

I appreciate how this article breaks down the calculation methods for both depreciation and amortization, providing a thorough understanding of the processes involved.

The examples provided for the calculation methods of depreciation and amortization are clear and illustrative, aiding in the comprehension of these accounting practices.

Absolutely, the practical application of the calculation methods through examples enriches the learning experience offered by this article.

I couldn’t agree more, Nyoung. The use of concrete examples enhances the article’s educational value for readers seeking to apply these concepts in real-world scenarios.

The thorough breakdown of the calculation methods and purposes of both depreciation and amortization in this article provides a comprehensive understanding of their roles in financial reporting and taxation.

I found the detailed discussion on the tax implications of depreciation and amortization particularly enlightening, shedding light on their significance in tax planning for businesses.

Absolutely, Maisie. The attention to tax implications adds a practical dimension to the article’s exploration of these accounting methods.

While the article is well-written and thorough, I do think it could benefit from more real-world examples to further illustrate the concepts of depreciation and amortization.

I understand your point, Parker. Including more practical scenarios would definitely enhance the application of these accounting methods.

While the article effectively delineates the differences between depreciation and amortization, it could benefit from a more engaging presentation style to ensure sustained reader engagement.

I see your point, Ruth. Incorporating interactive elements or case studies could enhance the article’s engagement and applicability for readers.

I agree, Ruth. A more interactive approach would likely contribute to a more dynamic learning experience for readers engaging with this content.

The article’s in-depth exploration of depreciation and amortization provides a comprehensive foundation for understanding these essential accounting methods, benefiting professionals and learners in the field of finance.

Absolutely, Lcollins. The use of practical examples enriches the educational value of this article, making it accessible and relatable for a wide audience.

I found the tangible examples used to explain the concepts of depreciation and amortization to be particularly effective in facilitating comprehension and retention of the material.