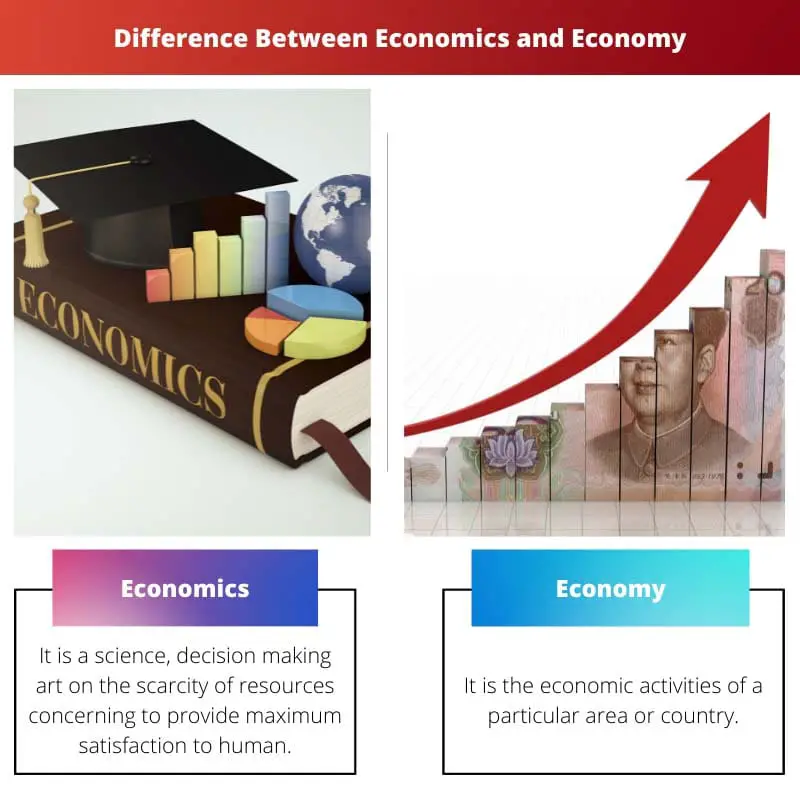

Economics refers to the study of how individuals, businesses, and governments allocate resources to satisfy unlimited wants in a society, encompassing theories, principles, and policies. On the other hand, the economy refers to the system of production, distribution, and consumption of goods and services within a specific region or country, often characterized by factors such as GDP growth, inflation rates, and employment levels.

Key Takeaways

- Economics is the social science that studies the production, distribution, and consumption of goods and services; the economy refers to resource allocation and wealth creation within a specific region or country.

- Economics involves theoretical concepts, models, and analytical methods; the economy is a practical manifestation of economic activity and outcomes.

- Both economics and the economy are interconnected, as economics aims to understand, explain, and potentially influence the functioning of an economy.

Economics vs Economy

Economics refers to the academic and scientific discipline that investigates how societies allocate scarce resources to meet needs and wants. An economy is a practical, real-world system in which goods and services are produced, distributed, and consumed within a specific region or country.

Whenever we talk or think about the economy, the first thing that comes to mind is Money. Is money the only thing that the economy and economics handle? Or it includes certain other things as well?

A person’s everyday life includes the food he wants to eat, the dress to wear, or how he wants to live. Economics and the Economy are vital in every man’s daily life.

There is no particular answer set for economics. It is the study of the economy or the study of the logical choice of humans. It analysis the decision of an individual, businesses, government, or firms on resources for maximum output.

The economy is a system indicated about a particular region or a country of production, consumption, money supply, goods and services distribution and exchange among the organization or people.

It gives standard value to different types of goods and services.

Comparison Table

| Feature | Economics | Economy |

|---|---|---|

| Definition | A social science that studies how individuals, societies, and governments make choices under scarcity, focusing on production, distribution, and consumption of goods and services. | The actual system of production, distribution, and consumption of goods and services within a specific region, country, or the world as a whole. |

| Focus | Theoretical frameworks, models, and analysis to understand how economic systems function and how different factors affect them. | The practical application of these principles, including specific activities, industries, institutions, and resources. |

| Goals | To understand, explain, and predict economic phenomena, develop policies to improve economic outcomes, and contribute to societal well-being. | To efficiently produce and distribute goods and services to meet the needs and wants of individuals and societies. |

| Examples | Studies market structures, supply and demand, economic growth, inflation, unemployment, taxation, and international trade. | Includes specific industries (manufacturing, agriculture, service), employment levels, trade activities, and financial markets |

What is Economics?

Introduction to Economics:

Economics is a social science that examines how societies allocate scarce resources to satisfy unlimited human wants and needs. It encompasses the study of production, distribution, and consumption of goods and services within economies, both on micro and macro levels. At its core, economics seeks to understand how individuals, businesses, and governments make decisions regarding resource allocation to maximize utility, efficiency, and overall well-being.

Branches of Economics:

- Microeconomics: Microeconomics focuses on the behavior of individual agents, such as consumers, producers, and firms, and the interactions between them in specific markets. It analyzes how these agents make decisions regarding resource allocation, pricing, production, and consumption, considering factors like supply and demand, market competition, and consumer preferences. Microeconomics also examines issues such as elasticity, market failures, and the role of government intervention in regulating markets.

- Macroeconomics: Macroeconomics deals with the aggregate behavior of economies as a whole, studying phenomena such as economic growth, inflation, unemployment, and fluctuations in output and income. It explores the determinants of national income, the role of monetary and fiscal policies in stabilizing economies, and the effects of globalization and international trade on national economies. Macroeconomics also delves into topics like economic indicators, business cycles, and economic development.

Key Concepts in Economics:

- Scarcity: Scarcity is the fundamental economic problem arising from limited resources and unlimited wants. It necessitates choices and trade-offs as individuals, businesses, and societies allocate resources among competing uses. Understanding scarcity is crucial in analyzing economic decision-making and resource allocation across different sectors and levels of society.

- Supply and Demand: Supply and demand are central concepts in economics, determining the prices and quantities of goods and services in markets. Supply refers to the quantity of a good or service that producers are willing and able to offer for sale at various prices, while demand represents the quantity of that good or service that consumers are willing and able to purchase at different price levels. The interaction between supply and demand influences market equilibrium, where the quantity demanded equals the quantity supplied, establishing the equilibrium price and quantity in a market.

- Opportunity Cost: Opportunity cost refers to the value of the next best alternative forgone when a decision is made. It reflects the trade-off involved in choosing one option over another and is a critical concept in understanding the cost of decision-making in economics. By considering opportunity costs, individuals and businesses can assess the benefits and drawbacks of different choices and make more informed decisions about resource allocation.

What is Economy?

Introduction to Economy:

An economy is a complex system that encompasses the production, distribution, and consumption of goods and services within a specific region, country, or even the global community. It represents the sum total of all economic activities and interactions among individuals, businesses, and governments within a defined geographic area. Understanding the economy involves analyzing various factors, including economic growth, employment levels, inflation rates, income distribution, and the overall standard of living.

Components of an Economy:

- Production: Production is the process of creating goods and services using various inputs such as labor, capital, and natural resources. It involves activities ranging from manufacturing and agriculture to services like healthcare, education, and transportation. The level of production within an economy determines its capacity to meet the demands of consumers and contribute to overall economic output.

- Distribution: Distribution refers to the allocation of goods and services among individuals, businesses, and institutions within an economy. It involves mechanisms such as markets, trade, and government policies that determine how resources are distributed across different sectors and segments of society. Distribution also encompasses issues related to income inequality, wealth disparities, and access to essential goods and services.

- Consumption: Consumption is the utilization of goods and services by individuals and households to satisfy their wants and needs. It encompasses spending on necessities like food, clothing, and shelter, as well as discretionary purchases such as entertainment, travel, and luxury goods. Consumer behavior and spending patterns play a significant role in shaping economic activity, influencing production decisions, market demand, and overall economic growth.

Types of Economies:

- Market Economy: In a market economy, the allocation of resources is primarily determined by the forces of supply and demand operating in competitive markets. Individuals and businesses make decisions based on their own self-interest, and prices serve as signals guiding resource allocation and production decisions. Market economies are characterized by private ownership of resources, minimal government intervention, and a focus on efficiency and innovation.

- Command Economy: In a command economy, the government centrally plans and controls economic activities, including production, distribution, and resource allocation. Prices, production levels, and investment decisions are dictated by government authorities rather than market forces. Command economies are associated with state ownership of resources, extensive government regulation, and a focus on collective welfare rather than individual profit motives.

- Mixed Economy: A mixed economy combines elements of both market and command economies, with varying degrees of government intervention and market regulation. In a mixed economy, governments play a role in regulating markets, providing public goods and services, and addressing market failures while allowing for private ownership and market-driven allocation of resources. Mixed economies aim to achieve a balance between efficiency, equity, and stability by leveraging the strengths of both market mechanisms and government intervention.

Main Differences Between Economics and Economy

- Scope:

- Economics refers to the academic discipline that studies how individuals, businesses, and governments allocate resources to satisfy unlimited wants within a society.

- Economy, on the other hand, refers to the actual system of production, distribution, and consumption of goods and services within a specific region, country, or the global community.

- Focus:

- Economics focuses on theories, principles, and policies related to resource allocation, market behavior, and economic decision-making.

- Economy focuses on real-world phenomena such as economic growth, employment levels, inflation rates, income distribution, and overall economic performance.

- Level of Analysis:

- Economics analyzes economic phenomena at both micro and macro levels, studying individual behavior, market interactions, and aggregate economic indicators.

- Economy represents the aggregate outcome of economic activities within a particular geographic area, encompassing all economic agents and their interactions in the production, distribution, and consumption of goods and services.

I appreciate the detailed comparison between economics and economy. It really helped clarify the distinction for me.

I don’t agree, the article could have been more concise.

I’m with you on this, Nrobinson. The article was very detailed and helpful.

Very informative article. I finally understand the difference between economics and economy, something that has always confused me. Thank you!

I couldn’t agree more, Ccarter. This article was very enlightening.

I have to disagree, I didn’t find this informative at all.