Management accounting focuses on providing internal information to support managerial decision-making, budgeting, and performance analysis within an organization. In contrast, cost accounting specifically deals with the identification, measurement, and analysis of costs associated with producing goods or services, aiming to improve cost efficiency and control within the production process.

Key Takeaways

- Management accounting focuses on providing managers with relevant financial and non-financial information for decision-making, planning, and controlling business activities.

- Cost accounting is a subset of management accounting, concentrating on recording, analyzing, and allocating costs to products, services, or departments for cost control and pricing.

- Both disciplines support informed decision-making, with management accounting providing broader insights, while cost accounting specifically targets cost management and efficiency.

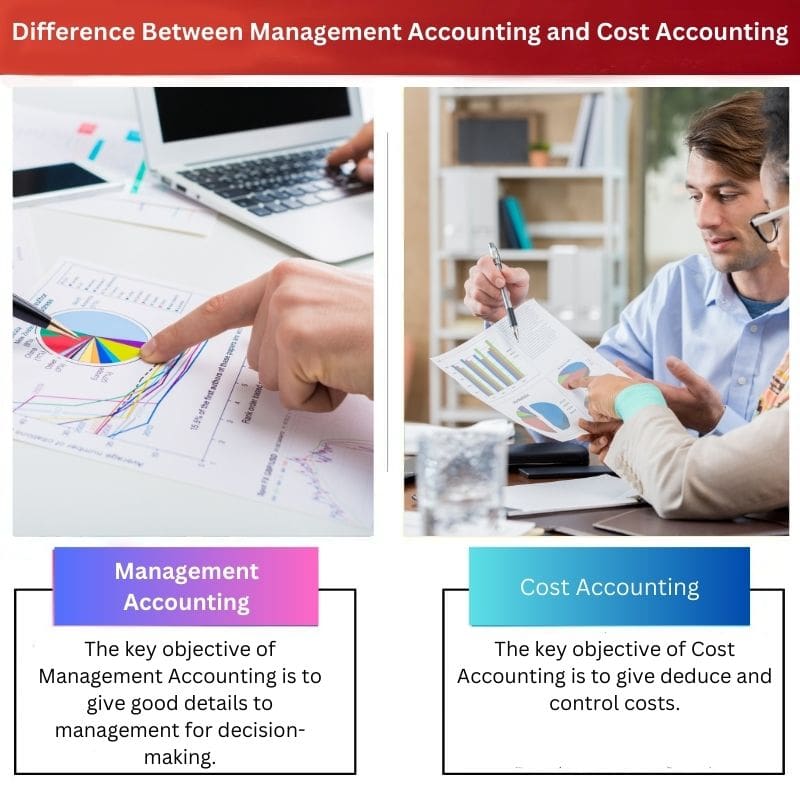

Management Accounting vs Cost Accounting

The difference between Management Accounting and Cost Accounting is that Management accounting gives us all accounting details, whereas Cost accounting gives us just cost points for managerial motives.

Comparison Table

| Feature | Management Accounting | Cost Accounting |

|---|---|---|

| Focus | Providing information for decision-making | Recording, analyzing, and reporting costs |

| Scope | Broader – includes both financial and non-financial information | Narrower – focuses primarily on costs |

| Objectives | Supports planning, controlling, and performance evaluation | Helps determine product costs, set selling prices, and control expenses |

| Information Type | Quantitative and qualitative | Primarily quantitative |

| Time Horizon | Past, present, and future | Primarily historical (past) |

| Users | Internal management (all levels) | Internal management (cost centers, production) |

| Examples | Budgeting, cost-volume-profit (CVP) analysis, performance reports | Cost allocation methods, variance analysis, activity-based costing (ABC) |

What is Management Accounting?

Purpose of Management Accounting

Management accounting, also known as managerial or cost accounting, is a branch of accounting that focuses on providing financial information and analyses to aid management in decision-making and control within an organization. It plays a crucial role in helping managers make informed choices to achieve organizational goals and enhance overall performance.

Decision Support

Management accounting provides valuable insights to support decision-making processes. By offering financial data and analysis, it assists managers in evaluating different options, making strategic choices, and allocating resources effectively.

Planning and Budgeting

One key aspect of management accounting is the formulation of plans and budgets. This involves setting financial goals, forecasting future expenses and revenues, and establishing a framework for monitoring and controlling financial performance.

Performance Measurement

Management accountants develop performance metrics and key performance indicators (KPIs) to assess how well the organization is meeting its objectives. These metrics help in evaluating departmental and individual performances, facilitating performance improvement initiatives.

Cost Accounting

Cost Classification

Cost accounting, a subset of management accounting, involves classifying and tracking different types of costs within an organization. These include direct costs, indirect costs, fixed costs, variable costs, and overhead costs.

Cost Control

Cost control is a critical function of management accounting. It involves monitoring and managing costs to ensure that they align with budgeted amounts. This helps in preventing cost overruns and improving overall cost efficiency.

Cost Analysis

Management accountants analyze costs to identify areas where efficiencies can be improved. This involves comparing actual costs to budgeted costs, conducting variance analysis, and recommending cost-saving measures.

Financial Analysis

Financial Statements

Management accounting contributes to the preparation of financial statements such as income statements, balance sheets, and cash flow statements. These statements provide a comprehensive overview of an organization’s financial health and performance.

Ratio Analysis

Ratio analysis is a common tool used in management accounting to assess financial performance. It involves calculating and analyzing various financial ratios, such as liquidity ratios, profitability ratios, and efficiency ratios, to evaluate the organization’s financial health.

Strategic Management

Strategic Planning

Management accounting supports strategic planning by providing financial information that aids in the formulation of long-term goals and strategies. It helps in assessing the financial feasibility of different strategic options.

Risk Management

Identifying and managing financial risks is a crucial aspect of management accounting. This involves assessing potential risks, developing risk mitigation strategies, and ensuring that the organization is financially resilient in the face of uncertainties.

What is Cost Accounting?

Objectives of Cost Accounting

1. Cost Ascertainment

Cost accounting aims to determine and analyze the various costs incurred in the production or provision of goods and services. This involves the identification of direct and indirect costs, fixed and variable costs, and explicit and implicit costs associated with business operations.

2. Cost Control

One of the primary objectives of cost accounting is to establish effective control mechanisms to manage and regulate costs. By comparing actual costs with budgeted costs, management can identify areas where costs exceed expectations and take corrective actions to bring them under control.

3. Cost Reduction

Cost accounting facilitates the identification of inefficiencies and redundancies in the production process. This information enables management to implement cost reduction strategies, thereby improving overall operational efficiency and increasing profitability.

4. Profit Planning

Cost accounting provides valuable insights for profit planning and forecasting. By understanding the cost structure, management can set realistic pricing strategies, sales targets, and profit margins to achieve long-term financial objectives.

Elements of Cost

1. Direct Costs

Direct costs are expenses directly attributable to the production of goods or services. Examples include raw materials, direct labor, and direct expenses. These costs can be easily traced to specific cost centers.

2. Indirect Costs

Indirect costs are expenses that cannot be directly traced to a specific product or service. These costs, also known as overhead costs, include rent, utilities, and administrative expenses. Allocation of indirect costs is done through cost allocation methods.

3. Fixed Costs

Fixed costs remain constant regardless of the production volume. These include salaries, rent, and insurance. Fixed costs per unit decrease as production levels increase, leading to economies of scale.

4. Variable Costs

Variable costs vary in direct proportion to the level of production. Examples include raw materials and direct labor. Variable costs per unit remain constant, but the total variable costs increase as production levels rise.

Methods of Costing

1. Job Costing

Job costing is used when production is based on specific customer orders or projects. Costs are allocated to each job or project separately, allowing for accurate tracking of expenses related to individual units.

2. Process Costing

Process costing is suitable for industries with continuous production processes, such as chemical manufacturing or food processing. Costs are averaged over the total production output during a specific period.

3. Activity-Based Costing (ABC)

ABC allocates costs based on the activities that drive them. It provides a more accurate representation of the actual cost of products or services by considering the specific activities required to produce them.

Main Differences Between Management Accounting and Cost Accounting

- Scope:

- Management Accounting: Focuses on providing information and analysis for internal decision-making within an organization. It includes a broader range of activities beyond cost-related information, such as budgeting, forecasting, and performance evaluation.

- Cost Accounting: Primarily concerned with the recording, analysis, and control of costs within an organization. It is a subset of management accounting, specifically dealing with cost-related aspects.

- Purpose:

- Management Accounting: Aims to assist management in making informed decisions by providing relevant financial and non-financial information. It helps in planning, controlling, and evaluating the performance of the organization.

- Cost Accounting: Primarily focuses on determining and controlling the costs associated with producing goods or services. It helps in assessing the cost efficiency and profitability of different products or services.

- Time Orientation:

- Management Accounting: Emphasizes both historical and future-oriented information. It involves analyzing past performance and making projections for future decision-making.

- Cost Accounting: Primarily concerned with historical costs, tracking and analyzing expenses that have already been incurred in the production process.

- Users:

- Management Accounting: Information is used by internal management, including top-level executives, department heads, and other decision-makers within the organization.

- Cost Accounting: Information is used by internal managers for cost control purposes, as well as by external stakeholders, such as investors and creditors, to assess the cost structure and efficiency of the organization.

- Reporting:

- Management Accounting: Involves flexible and customized reporting formats tailored to the specific needs of management for strategic decision-making.

- Cost Accounting: Typically involves standard reports focused on costs, cost variances, and cost trends, which are essential for cost control and performance evaluation.

- Regulatory Compliance:

- Management Accounting: Not subject to external regulations or reporting standards. It is designed to meet the internal needs of the organization.

- Cost Accounting: May need to comply with certain external reporting standards, particularly if the organization is required to disclose cost information to regulatory bodies or stakeholders.

- Nature of Information:

- Management Accounting: Provides both financial and non-financial information, including qualitative data, to support a wide range of managerial decisions.

- Cost Accounting: Primarily deals with quantitative financial data related to the costs incurred in the production process.

- Decision Focus:

- Management Accounting: Supports strategic decision-making, such as product pricing, market analysis, and resource allocation.

- Cost Accounting: Primarily focuses on tactical decisions related to cost control, process improvement, and efficiency in production.

This is helpful and informative.

It’s quite thought-provoking.

Yes, many interesting points are made.

It would be interesting to see some real-world examples.

Yes, real-world examples would add value.

I agree, it would make it more relatable.

This seems very useful for businesses looking to manage and control costs.

It seems helpful, but are there any drawbacks to consider?

Sure, there are some drawbacks like it only deals with financial transactions.

This is a great article!

I have to disagree; there’s some misleading information.

I was looking for this information, thanks for sharing this.

This article is full of useful information.

Yes, the information provided is quite valuable.

I found it to be quite insightful, a worthwhile read.

I’ve found this to be quite informative.

It’s certainly eye-opening.

This is a bit biased.

Agreed, there are aspects to consider that weren’t included in the article.

It seems a little one-sided.

Thanks for shedding light on this subject

Agreed, this sheds new light on the topic.

Can’t argue with data!

Definitely, the data speaks for itself.