Accounting concepts refer to the fundamental assumptions underlying the preparation of financial statements, such as going concern, consistency, and accruals. Accounting principles, on the other hand, are specific rules and guidelines derived from these concepts, governing how transactions are recorded and reported, such as the matching principle or the principle of conservatism.

Key Takeaways

- Accounting concepts are the basic assumptions and ideas that form the foundation of the accounting process, such as the going concern, accruals, and consistency concepts.

- Accounting principles are the rules and guidelines for applying accounting concepts, such as revenue recognition, matching, and historical cost principles.

- Both accounting concepts and principles aim to ensure accuracy, consistency, and transparency in financial reporting, but concepts provide the foundational framework while principles guide specific applications.

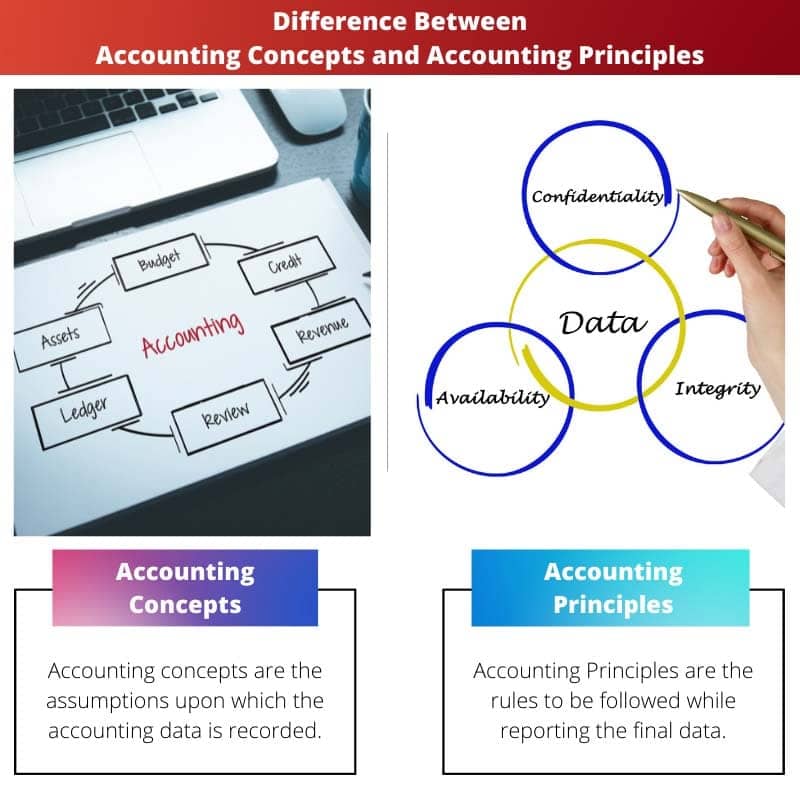

Accounting Concepts vs Accounting Principles

Accounting concepts refer to the basic assumptions, rules, and ideas that underpin the practice of accounting, providing a framework for recording and reporting financial transactions. Accounting principles are guidelines and rules that govern how financial transactions are recorded and reported.

Comparison Table

| Feature | Accounting Concepts | Accounting Principles |

|---|---|---|

| Definition | Fundamental assumptions that form the foundation for recording and reporting financial information. | Specific rules and guidelines that govern how accounting information is prepared and presented. |

| Focus | Provide a theoretical framework for understanding and interpreting financial statements. | Define the practical methods used to record, measure, and report financial transactions. |

| Examples | * Going concern * Accrual basis * Monetary unit assumption | * Revenue recognition principle * Matching principle * Materiality principle * Consistency principle |

| Level of detail | More general and broad. | More specific and prescriptive. |

| Development | Evolve over time based on accounting practice and experience. | Established by accounting standard-setting bodies like FASB (US) or IASB (international). |

| Objective | To ensure consistency and fairness in financial reporting. | To ensure reliability, relevance, and comparability of financial information. |

What are Accounting Concepts?

Accounting concepts, also known as accounting assumptions or principles, form the foundational framework upon which financial accounting is built. They provide a set of fundamental guidelines and assumptions that guide the preparation and presentation of financial statements. Understanding these concepts is crucial for accurately interpreting financial information.

Going Concern Concept

The going concern concept assumes that a business will continue to operate indefinitely unless there is evidence to the contrary. This concept implies that financial statements are prepared under the assumption that the entity will continue its operations for the foreseeable future, allowing for the use of accrual accounting methods.

Accruals Concept

The accruals concept states that revenue and expenses should be recognized when they are earned or incurred, regardless of when cash is received or paid. This concept ensures that financial statements reflect the economic reality of transactions, providing a more accurate representation of a company’s financial position and performance.

Consistency Concept

The consistency concept requires that accounting methods and principles should be applied consistently from one period to another. This ensures comparability between financial statements over time, enabling stakeholders to analyze trends and make informed decisions based on reliable data.

Prudence (Conservatism) Concept

The prudence concept, also known as the conservatism concept, advises accountants to exercise caution when making estimates or judgments. It suggests that when there are uncertainties or risks involved, accountants should err on the side of caution by recognizing potential losses or liabilities immediately, while being conservative in recognizing gains.

Materiality Concept

The materiality concept states that financial information should be disclosed if its omission or misstatement could influence the economic decisions of users. It allows accountants to focus on reporting information that is relevant and significant, while omitting trivial details that may not impact stakeholders’ decisions.

Entity Concept

The entity concept asserts that a business is separate from its owners or other entities. This means that the business’s financial transactions should be recorded and reported independently from those of its owners, ensuring clarity and transparency in financial reporting.

Money Measurement Concept

The money measurement concept stipulates that only transactions and events that can be expressed in monetary terms should be recorded in the accounting records. This concept simplifies accounting by focusing on quantifiable aspects of transactions, but it may overlook qualitative factors that could affect the business’s performance.

Time Period Concept

The time period concept, also known as the periodicity concept, divides the life of a business into distinct and regular intervals for financial reporting purposes. Typically, financial statements are prepared for specific time periods, such as monthly, quarterly, or annually, enabling stakeholders to track the company’s performance over time.

Realization (Recognition) Concept

The realization concept states that revenue should be recognized when it is earned, regardless of when cash is received. Similarly, expenses should be recognized when they are incurred, regardless of when they are paid. This concept ensures that financial statements reflect the economic substance of transactions rather than just their legal form.

Dual Aspect Concept

The dual aspect concept, also known as the duality principle, is the fundamental principle of double-entry bookkeeping. It states that every transaction has two aspects: a debit and a credit, which must be recorded in equal amounts in the accounting equation (Assets = Liabilities + Equity). This concept ensures that the accounting equation remains in balance at all times.

Historical Cost Concept

The historical cost concept dictates that assets should be recorded in the financial statements at their original purchase price, rather than their current market value. This concept provides a reliable and objective basis for valuing assets, but it may not accurately reflect their true economic worth over time.

Substance Over Form Concept

The substance over form concept requires accountants to focus on the economic substance of transactions rather than their legal form. This means that transactions should be recorded and reported based on their underlying economic reality, even if the legal documents or formalities suggest otherwise.

Full Disclosure Concept

The full disclosure concept mandates that all relevant and material information should be disclosed in the financial statements and accompanying notes. This ensures transparency and completeness in financial reporting, allowing stakeholders to make well-informed decisions based on all available information.

Understandability Concept

The understandability concept emphasizes that financial information should be presented in a clear, concise, and easily comprehensible manner to facilitate understanding by users with reasonable knowledge of business and economic activities. This concept encourages the use of plain language and clear formatting in financial reports.

What are Accounting Principles?

Accounting principles, also known as Generally Accepted Accounting Principles (GAAP), are a set of standardized guidelines and rules that govern the preparation and presentation of financial statements. These principles ensure consistency, comparability, and transparency in financial reporting, allowing stakeholders to make informed decisions based on reliable information.

Principle of Prudence (Conservatism)

The principle of prudence, also known as the conservatism principle, advises accountants to exercise caution when making estimates or judgments. It suggests that when there are uncertainties or risks involved, accountants should err on the side of caution by recognizing potential losses or liabilities immediately, while being conservative in recognizing gains.

Principle of Consistency

The principle of consistency requires that accounting methods and principles should be applied consistently from one period to another. This ensures comparability between financial statements over time, enabling stakeholders to analyze trends and make informed decisions based on reliable data.

Principle of Materiality

The principle of materiality states that financial information should be disclosed if its omission or misstatement could influence the economic decisions of users. It allows accountants to focus on reporting information that is relevant and significant, while omitting trivial details that may not impact stakeholders’ decisions.

Principle of Objectivity

The principle of objectivity requires that financial information should be based on verifiable evidence and free from bias. This ensures that financial statements reflect the true economic substance of transactions, rather than being influenced by personal judgments or opinions.

Principle of Consensus

The principle of consensus suggests that accounting standards should be developed through a collaborative process involving input from various stakeholders, including accountants, regulators, investors, and other interested parties. This ensures that accounting standards are widely accepted and reflect the needs and interests of the broader financial community.

Principle of Materiality

The principle of materiality states that financial information should be disclosed if its omission or misstatement could influence the economic decisions of users. It allows accountants to focus on reporting information that is relevant and significant, while omitting trivial details that may not impact stakeholders’ decisions.

Principle of Full Disclosure

The principle of full disclosure mandates that all relevant and material information should be disclosed in the financial statements and accompanying notes. This ensures transparency and completeness in financial reporting, allowing stakeholders to make well-informed decisions based on all available information.

Principle of Accruals

The principle of accruals states that revenue and expenses should be recognized when they are earned or incurred, regardless of when cash is received or paid. This concept ensures that financial statements reflect the economic reality of transactions, providing a more accurate representation of a company’s financial position and performance.

Principle of Going Concern

The principle of going concern assumes that a business will continue to operate indefinitely unless there is evidence to the contrary. This principle implies that financial statements are prepared under the assumption that the entity will continue its operations for the foreseeable future, allowing for the use of accrual accounting methods.

Principle of Cost

The principle of cost dictates that assets should be recorded in the financial statements at their historical cost, rather than their current market value. This principle provides a reliable and objective basis for valuing assets, but it may not accurately reflect their true economic worth over time.

Principle of Conservatism

The principle of conservatism, also known as the prudence principle, advises accountants to recognize potential losses or liabilities immediately, while being conservative in recognizing gains. This principle ensures that financial statements present a cautious and realistic view of an entity’s financial position and performance.

Main Differences Between Accounting Concepts and Accounting Principles

- Nature:

- Accounting Concepts: Fundamental assumptions underlying financial reporting.

- Accounting Principles: Standardized guidelines and rules governing financial reporting.

- Purpose:

- Accounting Concepts: Provide a conceptual framework for preparing financial statements.

- Accounting Principles: Offer specific rules and standards for recording and presenting financial information.

- Flexibility:

- Accounting Concepts: More flexible and broad, guiding the overall approach to accounting.

- Accounting Principles: Less flexible, providing specific instructions on how to account for transactions.

- Level of Detail:

- Accounting Concepts: Generally broader and more abstract, focusing on fundamental assumptions like going concern and accruals.

- Accounting Principles: More detailed and specific, outlining rules such as revenue recognition and depreciation methods.

- Application:

- Accounting Concepts: Lay the foundation for accounting practices and influence the development of accounting principles.

- Accounting Principles: Directly applied in recording transactions and preparing financial statements, ensuring consistency and comparability.

- https://www.jstor.org/stable/2490520

- https://pdfs.semanticscholar.org/f073/d4cf97ad4390c1756b032dfe9bd33816dcef.pdf

- https://heinonline.org/hol-cgi-bin/get_pdf.cgi?handle=hein.journals/taxlr15§ion=30

Last Updated : 02 March, 2024

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

This article provides a holistic view of accounting concepts and principles, delivered with utmost clarity and coherence. It’s a testament to the author’s intellectual acumen in this field.

The article presents a clear and concise overview of accounting concepts and principles, highlighting their significance in financial reporting. A must-read for aspiring accountants and finance professionals.

Absolutely, it’s an excellent educational piece on the fundamental aspects of accounting. It’s refreshing to see such well-explained content on this topic.

This article provides a comprehensive understanding of the importance of accounting and finance in business growth. It’s a great resource for anyone looking to learn more about these crucial aspects of business operations.

I found the section about accounting concepts and principles particularly enlightening. It’s crucial to understand these foundational elements to ensure accurate financial reporting.

I agree, the article does a great job of breaking down complex concepts into easily understandable information. It’s a valuable read for anyone interested in finance and accounting.

While reading this article, I couldn’t help but admire the lucidity with which it explains the relationship between accounting concepts and principles. It’s a valuable contribution to the discourse on financial reporting.

I completely agree. The article’s meticulous approach in elucidating these concepts is indeed impressive. It’s a testament to the author’s expertise in this field.

A masterful exposition of accounting principles and concepts. The post adeptly navigates complex terrain, making it an invaluable resource for those seeking a profound understanding of financial reporting.

The article’s comprehensive coverage of accounting standards and their implications is truly praiseworthy. It’s a cerebral dissection of a critical aspect of finance and accounting.

Absolutely, the sheer depth of insight offered in this article is commendable. It makes the discourse on accounting concepts and principles both enriching and enlightening.

The section on accounting concepts and principles is both illuminating and thought-provoking. It’s a testament to the article’s scholarly approach in explicating these critical elements of financial reporting.

The clarity with which the article delineates the nuances between accounting concepts and principles is praiseworthy. It’s a testament to the author’s erudition in this domain.

Indeed, the article’s elucidation of accounting principles is a breath of fresh air. It steers clear of jargon, making it accessible to a wide audience.

This post delves deep into the intricate details of accounting standards, providing a compelling and informative narrative. It’s a commendable effort to demystify this crucial aspect of business operations.

I appreciate the thoroughness of the article in discussing the importance of accounting concepts and principles in maintaining the integrity of financial data. It’s a refreshing take on a complex subject.

The comparison table provided in the article offers a succinct yet comprehensive view of the disparities between accounting concepts and principles. It’s an invaluable resource for professionals and enthusiasts alike.

Absolutely, the table condenses complex information into an easily digestible format. Kudos to the author for such an insightful inclusion.

The article’s elucidation of accounting concepts and principles is both enlightening and enriching. It’s a commendable effort to unravel the intricacies of financial reporting, resonating with experts and novices alike.

I couldn’t agree more. The article’s erudite exploration of these foundational elements is truly insightful. It’s a must-read for anyone delving into the realms of accounting and finance.

This post serves as a pivotal source of knowledge on accounting concepts and principles, strategically weaving intricate details into a coherent narrative. It’s an intellectually stimulating read.