Accounting is necessary as it gives a summary of financial details. All companies and organizations do accounting to know their final budget and expenses.

There are several methods available with the help of which accounting is done. And for making it easier, there are hundredths of software in the market that does the accounting job.

GAAP Accounting and Tax Accounting are accounting methods, but both are used for different purposes. Both of them have different approaches and procedures.

GAAP Accounting is more difficult and requires more knowledge as it requires some technical skills which can be gained after years of experience.

Key Takeaways

- GAAP accounting Generally follows Accepted Accounting Principles to present financial statements, while tax accounting adheres to tax laws and regulations.

- GAAP accounting emphasizes transparency and comparability, while tax accounting focuses on compliance and minimization.

- GAAP accounting allows for accrual-based accounting, while tax accounting primarily uses cash-based accounting.

GAAP Accounting vs Tax Accounting

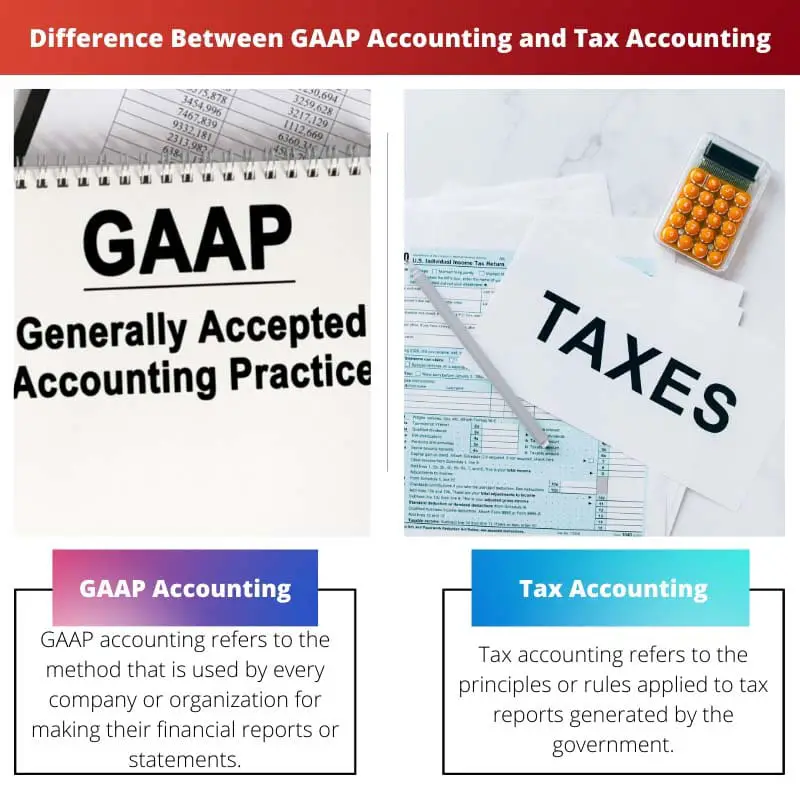

The difference between GAAP accounting and Tax accounting is that GAAP accounting is created by the financial accounting standard board and is based on standardized accounting and principles. On the other hand, Tax accounting is generated by a country’s Tax department, handled by the government and is based on Tax principles and rules.

GAAP is also called accepted accounting principles. It is a set of accounting principles and rules which is created by the FASB or financial accounting standard board. It is the most common method for generating financial reports or records which are easily comparable and understandable.

Tax accounting is a taxation rule or principle that is applied while calculating tax. It is not related to public financial statements. The internal revenue code issues or controls Tax accounting principles and guidelines.

And the rules generated by the internal revenue code are followed by the organizations and individuals for making or preparing Tax reports or returns.

Comparison Table

| Parameters of Comparison | GAAP Accounting | Tax Accounting |

|---|---|---|

| Definition | GAAP accounting refers to the method that is used by every company or organization for making their financial reports or statements. | Tax accounting refers to the principles or rules applied to tax reports generated by the government. |

| Principles applied | The rules applied in GAAP are standardized rules and principles set by FASB. | In Tax accounting tax rules and principles are applied which are set by the Tax department. |

| Basis of accounting | The basis of GAAP accounting is accrual. | The basis of Tax accounting can be accrual, modified, or cash basis. |

| Operated by | GAAP accounting methods are regulated by accounting and regulatory operators. | Tax accounting methods are regulated by tax regulatory operators. |

| Included transactions | In GAAP all types of transactions are included and are reported in the financial statement. | In Tax accounting method only transactions related to taxable income are included. |

| Intricacy or complexity | GAAP Accounting method includes more complex steps and rules. | Tax Accounting does not require too many technical skills and is less complex. |

What is GAAP Accounting?

GAAP Accounting is a standard accounting method used by most companies and organizations for maintaining their financial data records briefly and clearly. The reports generated by using this method are easily comparable and easy to understand.

Balance sheets, financial statements, income statements, etc., are created by using this.

GAAP Accounting uses some principles and rules which are set by FASB or the financial accounting standard board. It stands for accepted accounting principles. This method is very complex because many things are calculated during the application of the GAAP method.

This method requires skills as well as experience. The final report created by using this method also includes extraordinary items, which are shown below the statements. The inventory cost method used here is the last in, first out, or LIFO method.

What is Tax Accounting?

The Tax Accounting method is totally related to tax report preparation. The rules and guidelines applied in this method are set by the government, and the total method is controlled by the internal revenue code.

And the rules issued should be followed by each company and individual while preparing tax reports.

The Tax Accounting method differs in individual and organisational calculation ways. As for an individual, it is focused mostly on income, investment profits, or losses, etc. But when it comes to a company, it becomes complicated as many things are calculated with proper security measures.

In Tax Accounting, both last in, first out, and first in, last out methods are used. If Taxes are not calculated properly or if some malicious practices are included, these accounts of criminal activity and specified actions can be taken by the government.

Main Differences Between GAAP Accounting and Tax Accounting

- GAAP accounting refers to the method that is used by every company or organization for making their financial reports or statements. On the other hand, Tax accounting refers to the principles or rules applied to tax reports generated by the government.

- In Tax accounting, tax rules and principles are applied, which are set by the Tax department. In contrast, the rules applied in GAAP are standardized rules and principles set by FASB.

- In GAAP, all types of transactions are included and reported in the financial statement. Whereas in the Tax accounting method, only transactions related to taxable income are included.

- Tax Accounting does not require too many technical skills and is less complex. Whereas in GAAP accounting, more skills are required as it needs experience because of its complicated steps.

- The basis of Tax accounting can be accrual, modified, or cash basis. While the basis of GAAP accounting is accrual which makes the statements clear.

- http://public.kenan-flagler.unc.edu/faculty/langm/bllw_0302.pdf

- https://www.emerald.com/insight/content/doi/10.1108/02686900610661397/full/html

Last Updated : 08 August, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The distinction between GAAP and tax accounting in terms of the basis of accounting and complexity provides valuable insights into their unique characteristics and applications.

These fundamental differences highlight the diverse nature of accounting methods and their impact on financial management and compliance.

The comparison table effectively delineates the key differences between GAAP and tax accounting, providing a comprehensive understanding of their principles and applications.

It’s important for organizations and individuals to recognize these differences to ensure accurate and compliant financial reporting.

The complexity of GAAP accounting is evident with its technical skills requirements and the inclusion of all types of transactions, which makes it more comprehensive than tax accounting.

GAAP accounting’s emphasis on transparency and comparability provides a solid foundation for standardized financial reporting and analysis.

Absolutely, the different methods used in accounting reflect the diverse nature of financial reporting and management.

The complexities and intricacies of GAAP accounting reflect the need for specialized skills and experience, while tax accounting focuses on tax-specific transactions and compliance.

The different requirements and priorities of GAAP and tax accounting underscore their distinct roles in financial management and reporting.

GAAP accounting principles offer a standardized and comprehensive approach to financial reporting, which requires in-depth knowledge and experience to apply effectively.

The level of detail and complexity involved in GAAP accounting is crucial for generating accurate and comparable financial statements.

It’s fascinating to see how GAAP accounting emphasizes transparency and accuracy, while tax accounting is geared towards tax compliance and specific transactions that impact taxable income.

The rules and principles set by each accounting method contribute to the overall complexity and structure of financial records and reports.

The basis of GAAP accounting is accrual, while tax accounting can be based on accrual, modified, or cash basis. These differences highlight the contrasting nature of these two accounting methods.

Absolutely, the basis of accounting can significantly impact financial reporting and decision making.

These parameters of comparison provide a clear understanding of the complexity and intricacy involved in different accounting methods.

Accounting is crucial for any organization as it provides a clear summary of financial details and helps in budgeting and expense management.

I agree, accounting allows organizations to keep track of their financial health and make informed decisions.

In addition, there are various accounting methods available including GAAP and Tax Accounting, each with its own purpose and approach.

The role of regulatory operators in governing accounting methods ensures the integrity and reliability of financial records and statements.

Absolutely, the regulatory oversight contributes to the trustworthiness of financial reporting across various organizations and industries.

GAAP accounting is based on standardized principles and focuses on transparency and comparability, while tax accounting is governed by tax laws and regulations and emphasizes compliance and minimization of tax liabilities.

It’s interesting to see how different accounting methods serve different purposes and priorities for organizations and governments.