All countries and government bodies follow specific accounting standards for all businesses. These accounting standards include guidelines, rules, regulations, etc., for all companies.

These are followed as it is mandatory for companies to show their final financial report to government authorities. Two such accounting standards followed are IAS and GAAP.

Key Takeaways

- IAS (International Accounting Standards) provide a global framework, whereas GAAP (Generally Accepted Accounting Principles) apply to specific countries.

- IAS emphasize substance over form, while GAAP prioritize form over substance.

- GAAP allows for LIFO (Last In, First Out) inventory valuation, but IAS prohibits this method.

IAS vs GAAP

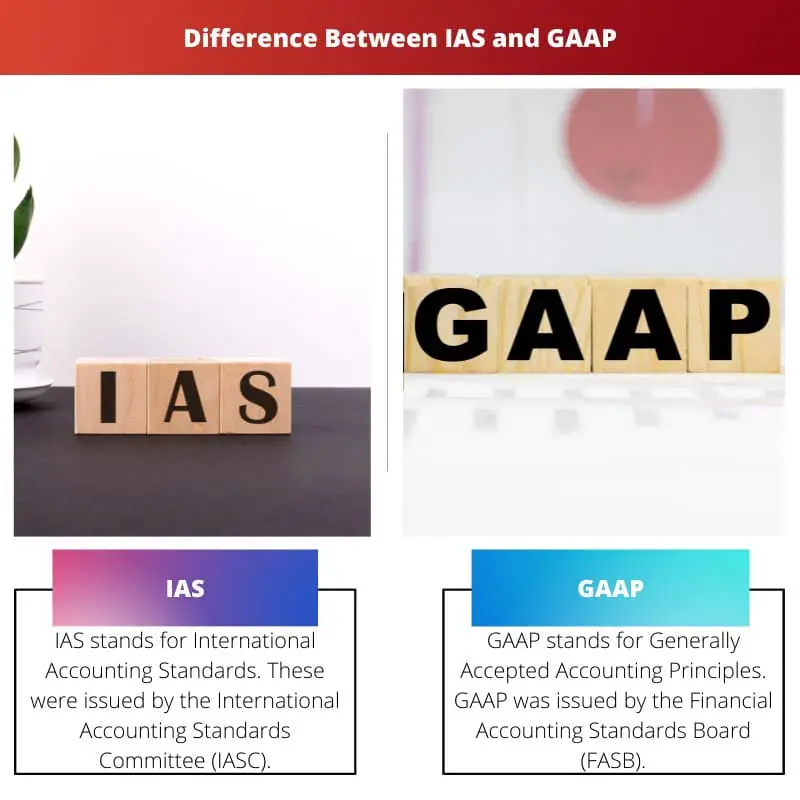

IAS stands for International Accounting Standards and is a global framework for presenting the account statements, issued by the International Accounting Standards Committee. GAAP means Generally Accepted Accounting Principles and is a country-specific method used mostly in the United States.

IAS stands for International Accounting Standards. These were issued by the International Accounting Standards Committee (IASC). However, IAS has now been replaced by International Financial Reporting Standards (IFRS).

IAS standards were used for presenting the account statements such as balance sheets, salary statements, cash flow statements, variations in equity, footnotes, etc.

GAAP stands for Generally Accepted Accounting Principles. GAAP was issued by the Financial Accounting Standards Board (FASB), the authority that controls and updates GAAP.

GAAP is a country-specific method and is only used mostly by companies in the United States. GAAP ensures that the financial transactions of companies, cash flow, equity statements, income, etc., are transparent and well-executed.

Comparison Table

| Parameters of Comparison | IAS | GAAP |

|---|---|---|

| Stands for | International Accounting Standards. | Generally Accepted Accounting Principles. |

| Basis | IAS includes principle-based standards which are fixed. | GAAP includes rule-based standards which can be edited according to the needs. |

| Active years | These standards were practised from 1973 to 2001. Then they were replaced by IFRS. | These standards were formed in 1933 and are still practised. |

| Countries | Accepted by over 120 countries. | Accepted only in the USA. |

| Total standards | A total of 41 IAS standards have been issued. | A total of 10 GAAP standards have been issued. |

What is IAS?

IAS stands for International Accounting Standards. These were the first international accounting standards throughout the world and were issued in 1973 by the International Accounting Standards Committee (IASC).

IASC was established in the same year by the finance representatives of 10 countries. These representatives devised the standards for International Accounting Standards (IAS).

In 2001, IASC was replaced by the International Accounting Standards Board (IASB). IASB continued developing international standards under the new International Financial Reporting Standards (IFRS).

Even though IAS standards are still practised, the new IFRS standards are an addition to the list of IAS standards. Hence, IAS standards are indirectly still indirectly active.

IAS is a planned method to understand a company’s financial status, future scope, tax payment, income levels, etc., so the company can be internationally compared to other companies in the same domain.

Ever since the European Union (EU) started practising IAS standards for their companies in 2005, IAS has been introduced to many countries, making it a global method for accounting.

Although IAS has become the most preferred accounting method, some countries, like the USA, Canada, UK, etc., are still an exception as they accept the GAAP method to handle their companies’ financial status.

What is GAAP?

GAAP stands for Generally Accepted Accounting Principles. GAAP standards were developed jointly by the Financial Accounting Standards Board (FASB) and the Governmental Accounting Standards Board (GASB).

The idea of GAAP was initiated when legislation passed the Securities Act of 1933 and the Securities Exchange Act of 1934. Since then, GAAP has undergone several reforms and gradual improvements to become the United States accounting method.

It is regarded as one of the best financial practices by many companies in the country.

GAAP devises objectives and guidelines for accounting statements and financial reports. It is mandatory for US-based companies to follow GAAP to compile their statements.

GAAP provides a strong framework for companies to report their accounting reports consistently every year.

GAAP standards are rules-based, so the GAAP procedures for the banking domain are different than those for the manufacturing domain and are different for all other businesses.

GAAP also practices full disclosure reporting, which means the inclusion of in-depth material in the financial reports so that the investors know exactly what they are investing their resources into.

This makes GAAP one of the most trusted accounting methods.

10 basic principles define GAAP’s foundation: Regularity, Consistency, Sincerity, Permanence of Methods, Non-compensation, Prudence, Continuity, Periodicity, Materiality, and Faith.

Main Differences Between IAS and GAAP

- IAS is a principle-based method of accounting, while GAAP is rules-based.

- IAS has a much wider reach and is practised globally, whereas GAAP is majorly practised by US-based companies.

- IAS uses the weighted-average method and the first-in-first-out method. On the other hand, GAAP uses the weighted-average method and both the last-in-first-out and first-in-first-out methods.

- IAS standards have a better future than GAAP because IAS has been expanding worldwide, and countries are slowly shifting towards the international method.

- In IAS, intangible assets are valued based on future economic benefits, whereas in GAAP, intangible assets are valued at a fair value.

Last Updated : 13 July, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The detailed analysis of IAS and GAAP is very comprehensive. Good post.

This content is quite enlightening. It’s great to know that IAS standards are expanding worldwide, offering a global method for accounting standards. Thanks for sharing.

This post is quite thought-provoking. It underscores the importance of understanding the global accounting standards.

This article sheds light on the global financial framework with great depth and clarity.

A well-researched and detailed article. Kudos to the writer!

This post brings to light the crucial details when it comes to the differences in accounting standards. It’s so informative and well-explained.

The stark differences between IAS and GAAP are quite astonishing, to say the least. Prominent post!

The thorough comparison between IAS and GAAP is quite commendable. I enjoyed reading the detailed analysis.