Firms in the United States employ GAAP or accepted accounting principles, whereas multinational investors use IFRS or International Financial Reporting Standards.

Key Takeaways

- GAAP and IFRS have different revenue recognition guidelines, affecting how companies report their earnings.

- GAAP requires revenue to be recognized when it is realized or earned. In contrast, IFRS requires revenue to be recognized when it is probable that the economic benefits associated with the transaction will flow to the entity.

- Companies operating may need to comply with GAAP and IFRS standards when reporting their financial statements.

GAAP vs IFRS

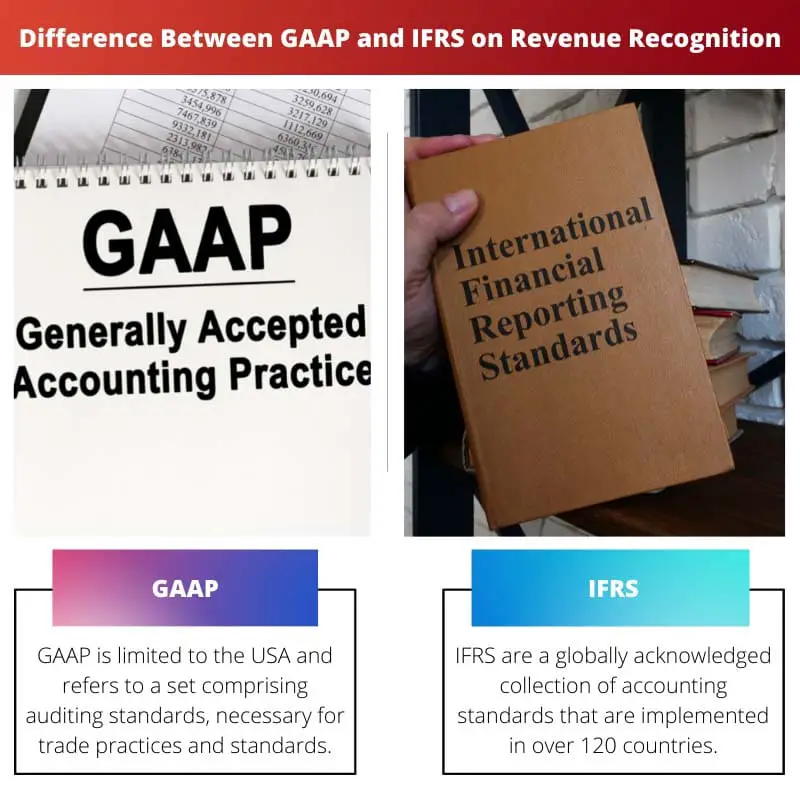

The difference between GAAP and IFRS is that in the United States, GAAP refers to a set comprising auditing standards but is not always internationally abided, whereas the International Financial Reporting Standards (IFRS) is a globally acknowledged collection of accounting standards that are implemented in over 120 countries spanning European, African, and Asian subcontinents. In other words, GAAP rules and regulations are followed in the USA, and IFRS is a solid worldwide set of regulations followed everywhere.

GAAP, aka accepted accounting, is a set of standards that defines and accounts for the precise criteria under which income is earned.

The cash basis, as defined by GAAP, requires revenue to be recognized when it is earned rather than when it is received.

IFRS, on the other hand, The International Financial Reporting Standards (IFRS) are a collection of principles that ensure balance sheets are uniform, fair, and equivalent all around the planet.

Comparison Table

| Parameters of Comparison | GAAP | IFRS |

|---|---|---|

| Definition | GAAP is limited to the USA and refers to a set comprising auditing standards, necessary for trade practices and standards. | The International Financial Reporting Standards (IFRS) are a globally acknowledged collection of accounting standards that are implemented in over 120 countries. |

| Functions | Income statement accountants follow all of the laws and regulations that have been set.Throughout corporate governance, identical criteria are applied. | A balance sheet is another name for this. The International Financial Reporting Standards (IFRS) have an impact on how balance sheet components are reported. |

| Country | United States of America | 120 countries are European, African and Asian countries. |

| Features | The Office Of Management And Budget establishes financial reporting procedures in the U. S., which are based on financial statements (GAAP). | The International Accounting Standards Board (IASB) issues IFRS, which governs how lawyers must keep and disclose corporate records. |

| Principles | The GAAP follows strict principles and laws only in the states under the USA. | IFRS has an international board of law enforcers who look upon financial records and trades. |

What is GAAP?

Generally Accepted Accounting Principles is an acronym for GAAP. GAAP is a collection of tax laws and customary business practices that have evolved through time.

Tax receipts must be recognized pursuant to the following calculation, which is a characteristic of accrual accounting, according to GAAP (accepted accounting principles).

For an operating income activity to be used in revenue within a sales transaction, it must be entirely or substantially completed. There has to be a sufficient level of assurance that the generated income payment will be received.

Some principles of GAAP are listed below:

- Regularity principle: Financial statements professionals rigorously follow established norms and regulations.

- Materiality principle: Quarterly accounts completely reflect the financial status of the organization.

- Prudence principle: Gambling has no bearing on business information reporting.

What is IFRS?

The International Financial Reporting Standards (IFRS) are a collection of principles that ensure balance sheets are uniform, fair, and equivalent all around the planet.

The International Financial Reporting Standards (IFRS) were created to provide a traditional budgeting language so that firms and their income reports could be appropriate and adequate from one firm to the next and from one country to another.

Whereas the United States and a few other nations do not utilize IFRS, the majority of nations do, rendering IFRS the most widely used worldwide set of rules.

In many aspects, the IFRS structure is founded on rules; the report sets a collection of fundamentals, as well as a set of needed papers that make up the business report.

Main Differences Between GAAP and IFRS

- The GAAP board of directors are not internationally governed, but in the case of IFRS, it is internationally governed.

- GAAP stands for Generally Accepted Accounting Principles, and IFRS stands for International Financial Reporting Standards.

- https://www.investopedia.com/terms/i/ifrs.asp

- https://www.accountingtools.com/articles/what-is-gaap.html

The explanation of IFRS and its universal applicability provides a broad understanding of its significance in the global financial landscape.

This article effectively outlines the key differences between GAAP and IFRS, offering valuable insights for financial professionals and organizations.

Definitely, the global reach of IFRS demonstrates its importance in standardizing financial reporting practices.

The detailed explanation of GAAP and IFRS offers valuable insights into the specific differences between these accounting standards, making it a useful resource for individuals and organizations alike.

Definitely, the depth and clarity of the article make it an informative guide for those seeking to comprehend GAAP and IFRS.

Indeed, the article effectively captures the nuances of GAAP and IFRS, providing a comprehensive understanding of their respective functions.

This is a really thorough and well-written explanation of the differences and purposes of GAAP and IFRS!

I agree, it’s great to have such a detailed comparison.

As an accountant, I know firsthand how important it is to understand these differences. A very useful article.

These standards are essential to global business operations, and it’s essential that companies and professionals understand and adhere to them.

Absolutely, it’s crucial for accounting professionals to be well-versed in GAAP and IFRS.

The article presents a comprehensive comparison of GAAP and IFRS, providing a clear understanding of their distinct functions and applications.

Absolutely, this article serves as an excellent reference for anyone interested in delving into the details of GAAP and IFRS.

The section explaining the principles of GAAP and IFRS is enlightening, offering a deep understanding of their underlying concepts.

Absolutely, understanding these principles is essential for sound financial reporting practices.

The comprehensive overview of GAAP and IFRS provides a solid foundation for understanding these critical accounting standards.

Indeed, the clear and comprehensive explanations make this article a valuable resource for anyone seeking to understand GAAP and IFRS.

The comparison table is especially helpful in highlighting the differences between GAAP and IFRS in a clear and concise manner.

Agreed, the detailed breakdown of the parameters of comparison is very informative.

The principles of GAAP and IFRS are clearly articulated, offering a thorough understanding of these fundamental frameworks.

Agreed, the in-depth exploration of principles makes this article a valuable educational resource.

The key differences highlighted in the comparison table are instrumental in distinguishing GAAP from IFRS, allowing for a precise understanding of their unique aspects.

Absolutely, the comparison table effectively captures the nuances of GAAP and IFRS, shedding light on their distinct features.