Both financial accounting and managerial accounting are major fields of accounting. Despite numerous parallels in technique and usage, financial and managerial accounting have considerable distinctions.

Key Takeaways

- Managerial accounting is focused on internal decision-making and helps managers make strategic decisions, while financial accounting is focused on external reporting and provides financial information to stakeholders.

- Managerial accounting includes budgeting and forecasting, while financial accounting includes preparing financial statements and reports.

- Managerial accounting is used by management to control costs and make business decisions, while financial accounting is used to comply with accounting standards and regulations.

Managerial Accounting vs Financial Accounting

Managerial accounting, also known as management accounting, is concerned with providing information to internal stakeholders such as managers, executives, and other decision-makers within an organization. Financial accounting is concerned with providing information to external stakeholders such as investors, creditors, and regulatory bodies. It provides accurate and reliable financial statements of an organization.

Recognizing, analyzing, analyzing, evaluating, and conveying monetary information to the management for the achievement of a company’s objectives is the profession of managerial accounting.

In the branch of accounting known as financial accounting, the business statements of a firm are summarized, analyzed, and reported.

Comparison Table

| Parameters of Comparison | Managerial Accounting | Financial Accounting |

|---|---|---|

| Significance | Managerial Accounting is the accountancy system that gives managers the information they need to make informed decisions about policies, plans, & tactics for leading the company efficiently. | An accountancy system that concentrates on the financial reporting for an organization in order to offer financial data for relevant parties is called Financial Accounting (FA). |

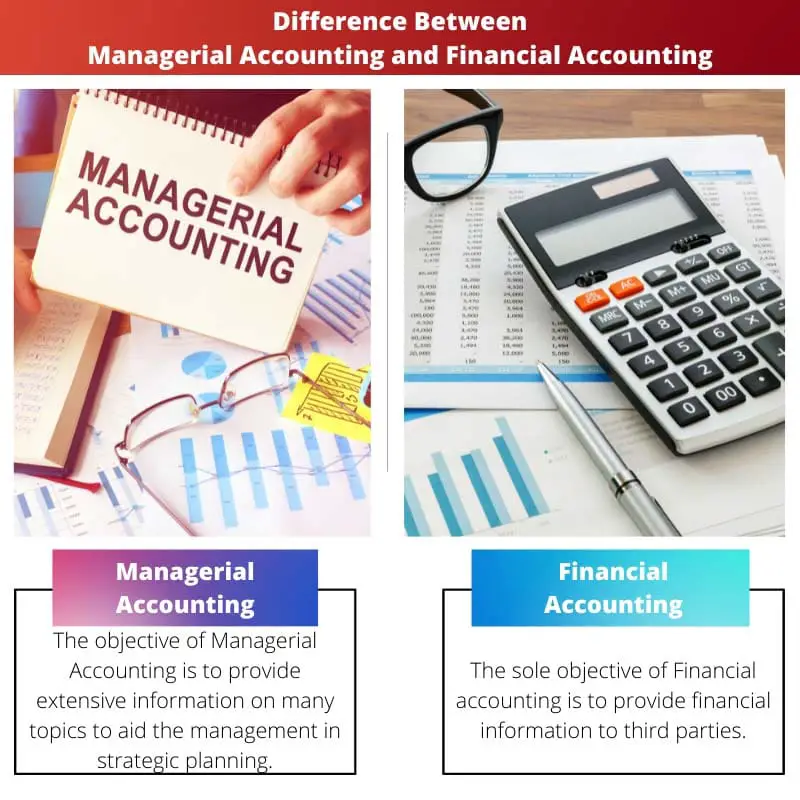

| Objective | The objective of Managerial Accounting is to provide extensive information on many topics to aid the management in strategic planning. | The sole objective of Financial accounting is to provide financial information to third parties. |

| Time Period | In Managerial accounting, the reports are produced according to the organization’s needs and specifications. | Financial Statements are generated at the conclusion of a year-long accounting cycle. |

| Reports | Informational reports that are complete and comprehensive are made in managerial accounting. | Organizational Audited Financials in Summarized Form are generated in financial accounting. |

| Publishing and auditing | Statutory auditors have neither disclosed nor examined the data in the case of managerial accounting. | Publication and inspection by statutory auditors are needed in Financial Accounting. |

What is Managerial Accounting?

Recognizing, analyzing, analyzing, evaluating, and conveying monetary information to the management for the achievement of a company’s objectives is the profession of managerial accounting.

Accountants use managerial accounting to improve the information they provide to management regarding business operations metrics, and it includes a wide range of accounting techniques.

When it comes to managing a company’s total manufacturing costs, cost accounting takes into consideration both the variable and the fixed costs of each phase of production.

To make capital expenditure selections, managers use managerial accounting professionals to assess and convey information. The use of working capital metrics, like the cost of capital as well as residual value, is one example.

What is Financial Accounting?

Accountants who specialize in the area of financial accounting summarise, monitor, and evaluate financial transactions for businesses.

Instances of those who are interested in getting such evidence for strategy-making purposes include shareholders, vendors, banks, staff, government entities, business owners, and some other stakeholders.

As a generic accountant, a financial accountant’s tasks may vary from that of a general accountant, who is self-employed and does not work for an organization.

The company’s regulatory as well as reporting obligations will determine which accounting standards are used throughout financial accounting.

Main Differences Between Managerial Accounting and Financial Accounting

- Informational reports that are complete and comprehensive are made in managerial accounting, whereas Audited organizational Financials in Summarized Form are generated in financial accounting.

- Statutory auditors have neither disclosed nor examined the data in the case of managerial accounting. Publication and inspection by statutory auditors are needed in Financial Accounting.

Last Updated : 14 August, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

This article does a great job explaining the key differences between managerial accounting and financial accounting.

I couldn’t agree more. The description of each type of accounting is very informative and useful.

This article encapsulates the differences clearly and concisely. It’s a valuable resource for those aiming to understand the distinctions between managerial and financial accounting.

Absolutely, the article provides a comprehensive overview of the distinctions between the two branches of accounting.

I couldn’t agree more, the article does a fantastic job clarifying the nuances of both accounting types.

Accountants and professionals in the field will find this article particularly insightful for understanding the contrasting requirements and purposes of managerial and financial accounting.

Absolutely, the article effectively distinguishes the roles and responsibilities of managerial and financial accounting professionals.

The table provided to compare managerial accounting and financial accounting is well-organized and easy to understand.

Absolutely, the detailed comparison table makes it easier to grasp the distinctions between the two fields.

The comprehensive comparison table is particularly helpful in understanding the differences in significance, objectives, and reports between managerial and financial accounting.

Absolutely, the article does a great job at highlighting the distinctions between managerial and financial accounting through this comparison.

Yes, the detailed comparison table enables a clear comprehension of the distinctions between the two accounting branches.

This article is an excellent resource for those aiming to grasp the differences between managerial accounting and financial accounting.

Absolutely, it offers a thorough examination of the distinctions between the two fields.

I found the article particularly valuable in clarifying the objectives of each type of accounting.

I appreciate the emphasis on the importance of managerial accounting in aiding the strategic planning of management.

Yes, the article effectively conveys the significance of managerial accounting in supporting the decision-making process by management.

Absolutely, the distinction between internal and external stakeholders is clearly articulated.

I found the article very useful for understanding the differences between managerial and financial accounting; it provides a great overview of the distinctions.

Absolutely, the article is a valuable resource for understanding and distinguishing between the two fields of accounting.

The definitions of managerial accounting and financial accounting are well-distinguished and clear.

I agree, the article provides a comprehensive understanding of the two branches of accounting.

The focus on the objectives and differing reporting requirements is really helpful in understanding the contrasting roles of managerial and financial accounting.

Absolutely, understanding the objectives and needs of the two types of accounting is crucial for professionals in the field.

Yes, the article effectively distinguishes the purpose of managerial and financial accounting in this regard.