People consider every area and method of making their lives more comfortable and stress-free.

One of these planning and components revolves around retirement and what all measures and aspects should be examined for a pleasant post-work lifestyle.

You will discover the difference between 403b and 457 schemes, which are popular outside of the public sector.

Key Takeaways

- 403b plans are retirement savings plans for employees of non-profit organizations, while 457 plans are for government employees and certain non-profit organizations.

- Both plans offer tax-deferred growth and pre-tax contributions, but withdrawal rules and contribution limits differ.

- 457 plans allow penalty-free withdrawals before age 59.5, unlike 403b plans, which impose a 10% penalty for early withdrawals.

403b Vs 457

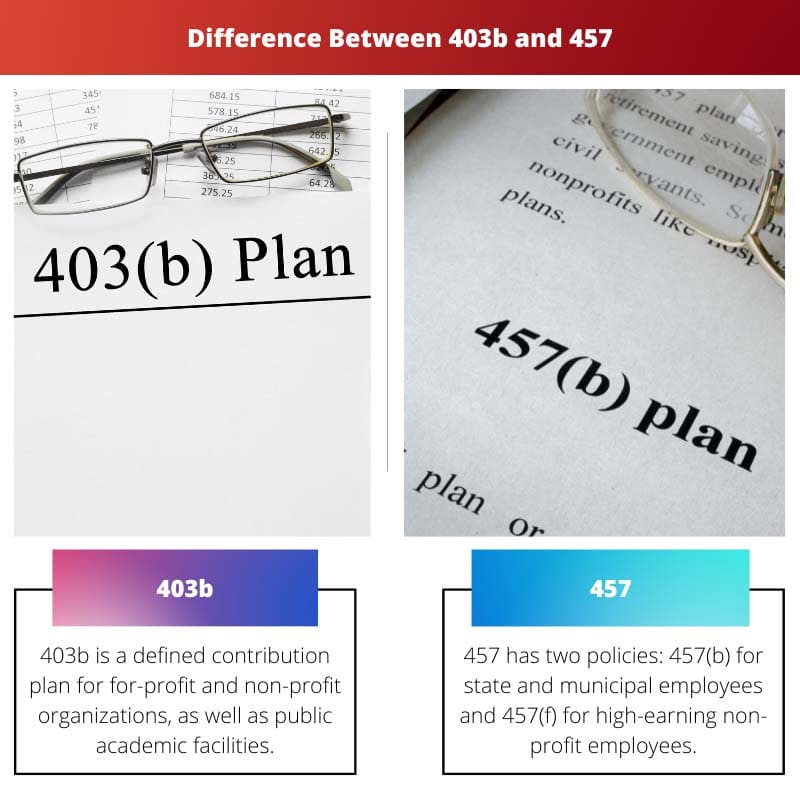

403(b) plans are available to non-profit organizations, public school employees, etc. 457 plans are offered to state and local government employees, including police officers, firefighters, etc. Insurance companies offer 403(b) plans, while Investment companies administer 457 plans.

Among the different retirement schemes and plans available, the 403b plan is primarily for employees of private organizations, public school employees, as well as other government workers. A 403b policy is a set of defined contribution policies that allow employees to save money for the future in a tax-deferred manner, similar to a 401(k) plan.

The 457 policy is a set of policies that includes two types. The first is 457 (b), which is presented to municipal and state employees and allows for contributions of up to $19,500 in 2021 and $20,500 in 2022, while the second is 457 (f), which is for top-tier non-profit executives and is chiefly used to enlist executives from the corporate sector.

Comparison Table

| Parameters of Comparison | 403b | 457 |

|---|---|---|

| Meaning | 403b is a defined contribution plan for for-profit and non-profit organizations, as well as public academic facilities. | 457 has two policies: 457(b) for state and municipal employees and 457(f) for high-earning non-profit employees. |

| Retirement Perks | 403b, will provide fewer benefits since only a limited amount of money may be invested. | 457, permits users to donate twice as much (100% of your salary), thus the benefits will be extremely good. |

| Withdrawal | Money in 403b is distributed at the age of 59.5, but if taken before then, a 10% penalty is levied. | There are no penalties for early withdrawal from the 457 policy. |

| Matching Contribution | 403b provides a matching contribution when an employer sponsors a pension plan based on the employee’s pay. | In 457, rare matching contributions are seen. |

| Choice | It is best to establish extra investing plans in 403(b). | Best in 457 when the additional time for investing is required. |

What Is 403b?

A 403b policy is a defined contribution policy that allows you to save money tax-free.

This regulation primarily applies to private and non-profit organizations, public academic facilities, and any other body that qualifies under the IRS as a “charity organization” working solely for a tax deduction.

Because the tax postponed under this policy was only invested in annuity agreements, it is known as a Tax-Deferred Annuity Plan.

Deferral refers to the saving of a small sum of cash for future revenue needs after retirement. Elective deferral is a term that refers to a capital contribution from one’s pay to a pension scheme (403(b)).

Every operation carried out by a worker must be authorized for security reasons. Worker deferrals are all made pre-tax. The amount removed will be recorded in the annual revenue.

Contribution restrictions for 403(b) plans are the same as for 401(k) plans.

All worker hardship deferments are given pretax, which reduces the individual’s altered net earnings. The yearly contribution maximum, known as the elective deferment, is $19,500 in 2021 and increases to $20,500 in 2022.

Individuals over the age of 50 can make an extra grab payment of $6,500 for 2021 and 2022.

Companies, like 401(k) plans, are permitted to implement automatic 403(b) policy donations for all employees, albeit they can drop out at their option.

Participants who are qualified may also be qualified for something like the Retirement Saver’s Credit.

What Is 457?

There are two types of 457 policy: a 457 (b) policy is available to state and municipal employees, while a 457 (f) policy is available to upper-edge nonprofit executives.

In a 457(b) policy, $19,500 in 2021 and $20,500 in 2022 can be contributed, with an extra $6,500 in 2021 and 2022 if the employee is 50 or older.

More contributions can be given if the worker is within three years of reaching standard retirement age. However, unless you are within three years of regular retirement age, your maximum contribution is restricted by prior contributions.

According to the Internal Revenue Service, this age limit is “the standard yearly restriction plus the amount of the standard restriction not used in the preceding years (primarily permitted if not using age 50 or over grab payments).”

The 457 (f) policy differs greatly from the 457 (b) policy. Pension benefits are referred to as “golden handcuffs” as they are linked to the length of employment and other performance criteria.

The 457 (f) policy is largely used to hire private-sector executives. Remuneration is exempt from taxation under 457 (f) programs.

Nonetheless, such retained earnings have to be exposed to a “substantial risk of forfeit,” which indicates that the manager may lose the benefit if they do not achieve the employment length or performance conditions.

When pay is assured and no longer in danger of forfeit, this becomes taxable as gross revenue.

Main Differences Between 403b and 457

- 403b is a defined contribution policy for for-profit and non-profit organizations, along with public educational institutions, 457, on the other hand, has two policies: 457(b) for state and city government workers and 457(f) for high in terms of earning non-profit employees.

- Because only a limited sum of funds can be invested in 403b, the benefits will be limited; however, 457 enables people to donate twice as much (100 percent of your salary), so the perks will be extremely good.

- Money in a 403b policy is distributed at the age of 59.5, but if taken before then, there is a 10% penalty, whereas there are no penalties for early withdrawal from a 457 insurance.

- When a firm supports a pension plan depending on the employee’s pay, 403b gives a matching contribution, but matching contributions are unusual in 457.

- 403b is the best way to build additional investment goals. When the additional time for investing is required, 457 is the best alternative.

- https://elibrary.ru/item.asp?id=4533581

- https://link.springer.com/content/pdf/10.1007/0-387-34450-0_4.pdf

Last Updated : 13 July, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

This article lacks in-depth analysis and fails to provide a critical view. A more detailed examination is needed to understand the potential drawbacks of these plans.

The article seems biased towards promoting these retirement schemes without addressing any negative aspects. There should be a focus on both advantages and disadvantages.

I agree with Fred. The article would have been more enriching if it had highlighted the possible limitations of 403b and 457.

The article thoroughly explains the features and differences between 403b and 457 plans. However, I believe it would have been more beneficial to include some case studies to provide a practical understanding.

The information provided in this article was insightful and comprehensive. It has undoubtedly enriched my knowledge about retirement planning and options.

The article effectively outlines the features and differences between 403b and 457 plans. However, it might be more engaging if real-life examples and success stories were included to make it more relatable.

I totally agree with you, Tim. Real-life illustrations would have added more value to the content.

This article provided me with all the essential information I needed to know about 403b and 457 plans. However, I’d like to see more insights into the tax implications and investment options for both these plans.

I found the article extremely informative, and the comparison table was really helpful in clarifying the difference between 403b and 457. Great piece of writing!