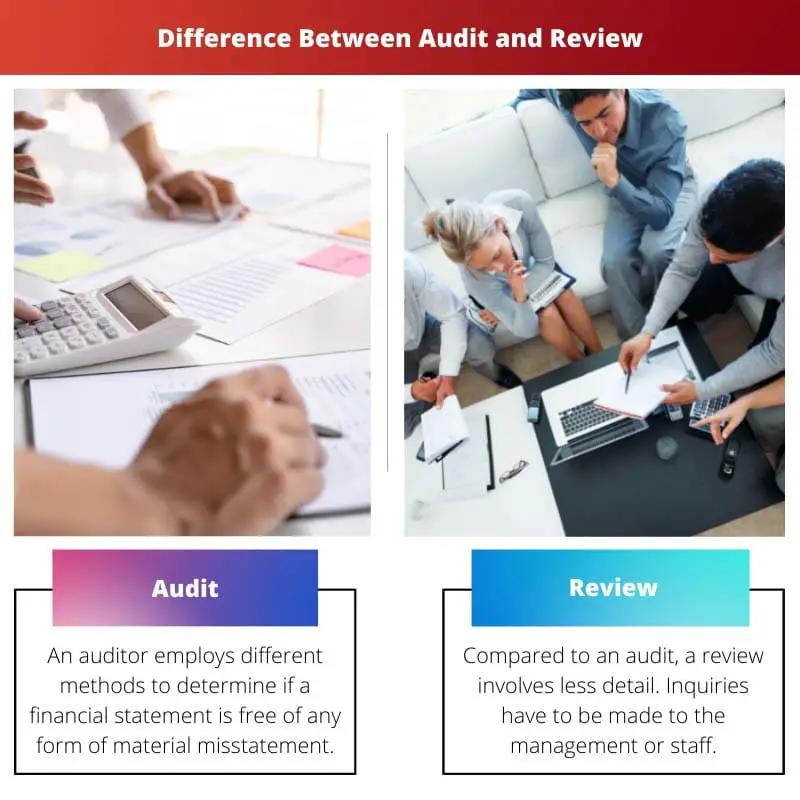

An audit involves a comprehensive examination of financial statements and internal controls to express an opinion on their fairness. A review is a less extensive assessment that provides limited assurance, focusing on analytical procedures and inquiries to detect material misstatements. Audits are more rigorous and suitable for situations requiring a higher level of assurance.

Key Takeaways

- An audit thoroughly examines an organization’s financial statements, internal controls, and accounting practices. At the same time, a review is a less intensive assessment of financial statements for reasonableness and accuracy.

- Audits provide a higher level of assurance than reviews, with auditors expressing an opinion on the financial statements’ fairness, whereas reviews offer a limited guarantee with no formal idea.

- Due to the difference in scope and depth, audits are more time-consuming and costly than reviews, but they provide greater confidence in the accuracy of financial statements.

Audit vs Review

Audit is checking the accuracy and rightfulness of the transaction procedures in an organization or a company by an auditor. Review is the process of rechecking, or a moderate reassurance of the assessment conducted by an auditor on the accounts or transactions of a company.

A review is simply the evaluation of the financial records to check if there is any chance for any modification.

Comparison Table

| Feature | Audit | Review |

|---|---|---|

| Purpose | Provides high level of assurance on the accuracy of financial statements | Provides limited assurance on the accuracy of financial statements |

| Level of scrutiny | Extensive testing of internal controls and transactions | Limited testing of internal controls and transactions |

| Procedures | In-depth analysis of financial records, including: * Analytical procedures * Tests of controls * Substantive procedures | Primarily focuses on: * Analytical procedures * Inquiry of management |

| Opinion issued | Auditor expresses unqualified opinion (financial statements are fairly presented), qualified opinion (with exceptions), adverse opinion (misstatements are material), or disclaimer of opinion (unable to express an opinion) | No opinion is expressed on the financial statements |

| Cost | More expensive due to the extensive procedures involved | Less expensive than an audit |

| Regulation | May be required by law or regulations for certain entities | Generally not required, but may be performed for various reasons |

| Suitability | For entities with high financial risk, complex operations, or regulatory requirements | For entities with lower financial risk, simpler operations, or seeking a cost-effective option |

What is an Audit?

An audit is a systematic and independent examination of financial information, statements, records, operations, and processes. It is conducted to provide assurance regarding the accuracy, reliability, and fairness of financial statements and to assess the effectiveness of internal controls within an organization.

Purpose of an Audit

- Financial Statement Assurance:

- The primary objective is to express an opinion on the fairness of financial statements, ensuring they present a true and fair view of the organization’s financial position, performance, and cash flows.

- Compliance Verification:

- Audits also verify compliance with relevant laws, regulations, and accounting standards, ensuring that financial reporting adheres to the required guidelines.

Key Steps in an Audit

- Planning:

- Auditors plan the engagement, assess risks, and determine the scope of the audit. This involves understanding the business, identifying significant accounts, and designing audit procedures.

- Fieldwork:

- This phase involves gathering evidence through various audit procedures, such as substantive testing and analytical procedures. Auditors may also assess internal controls during this stage.

- Reporting:

- After completing the audit procedures, auditors issue an audit report that includes their opinion on the financial statements’ fairness. The report also highlights any material misstatements and provides recommendations for improvement.

- Follow-Up:

- Post-audit, auditors may communicate with management to address any concerns or provide additional insights. Continuous improvement and feedback are integral aspects of the audit process.

Types of Audits

- External Audit:

- Conducted by independent auditors, external audits provide stakeholders, such as investors and creditors, with confidence in the accuracy of financial statements.

- Internal Audit:

- Internal auditors, part of the organization, focus on evaluating and improving internal controls, risk management, and operational efficiency.

- Government Audit:

- Conducted by government agencies, these audits assess compliance with laws and regulations, as well as the efficient use of public funds.

Importance of Audits

- Stakeholder Confidence:

- Audits enhance trust and confidence among stakeholders, including investors, creditors, and regulatory bodies, by providing an objective assessment of financial information.

- Risk Mitigation:

- Audits help identify and address potential financial and operational risks, contributing to improved organizational governance and overall risk management.

- Legal Compliance:

- Organizations must comply with various regulations, and audits ensure adherence to these requirements, reducing the risk of legal consequences.

What is a Review?

A review is a type of financial examination conducted by auditors, providing a level of assurance that is less comprehensive than an audit. It is performed to assess the reasonableness of financial statements, making it a valuable service for entities requiring a moderate level of assurance.

Purpose of a Review

- Limited Assurance:

- A review aims to obtain limited assurance that the financial statements are free from material misstatements. However, this level of assurance is not as rigorous as that provided by an audit.

- Analytical Procedures:

- Unlike audits, reviews primarily rely on analytical procedures and inquiries. Auditors use various analytical techniques to identify any unusual trends or fluctuations in financial data.

Key Characteristics

- Procedures Undertaken:

- The review process involves inquiries with company personnel and analytical procedures applied to financial data. This includes comparing current financial figures with historical data and industry benchmarks.

- No Physical Inspection:

- Unlike audits, reviews do not involve physical inspection of assets or direct confirmation with third parties. The focus is on assessing the plausibility of financial information through analytical means.

Reporting

- Review Report:

- At the conclusion of a review, auditors issue a review report expressing limited assurance. The report outlines the scope of the review, the procedures performed, and any identified issues or concerns.

- Usefulness for Stakeholders:

- The review report is beneficial for stakeholders who require a basic level of assurance on financial statements but may not necessitate the extensive procedures and cost associated with a full audit.

Main Differences Between Review and Audit

- Objective:

- Review: The objective of a review is to provide a moderate level of assurance that the financial statements are free from material misstatements. The reviewer aims to detect any obvious errors or inconsistencies in the financial statements.

- Audit: The objective of an audit is to provide a high level of assurance that the financial statements are free from material misstatements and that they present a true and fair view. Auditors seek reasonable assurance through a comprehensive examination of financial records and processes.

- Scope:

- Review: Reviews have a limited scope. They involve analytical procedures and inquiries to identify unusual items or errors in financial statements. The scope is narrower compared to an audit.

- Audit: Audits have a comprehensive scope. They involve detailed testing of transactions, internal controls evaluation, verification of account balances, and extensive documentation. The scope is broader compared to a review.

- Procedures:

- Review: Review procedures primarily consist of analytical procedures and inquiries with management and personnel. There is no verification of transactions or detailed testing.

- Audit: Audit procedures include substantive testing, tests of controls, verification of transactions, sampling, and extensive documentation. Auditors perform a wide range of procedures to gather evidence.

- Assurance Level:

- Review: Reviews provide a moderate level of assurance. The reviewer concludes that nothing came to their attention to suggest material misstatements.

- Audit: Audits provide a high level of assurance. Auditors issue an opinion on the fairness of the financial statements and explicitly state whether the statements are free from material misstatements.

- Materiality Threshold:

- Review: Reviews use a higher materiality threshold. Smaller errors or misstatements may not be identified during the review.

- Audit: Audits use a lower materiality threshold, making it more likely to detect smaller errors or misstatements.

- Independence:

- Review: Reviewers are required to be independent, but the independence requirements may be less stringent than audits.

- Audit: Auditors must be independent and free from conflicts of interest to maintain objectivity and integrity.

- Documentation:

- Review: Reviews require documentation of review procedures, inquiries, and analytical procedures performed. The documentation is less extensive compared to audits.

- Audit: Audits require comprehensive documentation of audit procedures, findings, conclusions, and supporting evidence.

- Reporting:

- Review: Reviewers issue a review report that includes a conclusion regarding whether the financial statements appear free from material misstatements.

- Audit: Auditors issue an audit report that includes an opinion on the fairness of the financial statements, along with an explanation of the audit procedures performed.

Last Updated : 25 February, 2024

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The article provides a comprehensive and clear comparison between audits and reviews, highlighting the key differences in terms of scope, assurance level, and procedures. It’s very informative and helpful for understanding the importance of both processes in evaluating financial statements.

I completely agree, Scarlett. The detailed explanation of the characteristics and objectives of an audit is particularly insightful, and it underscores the critical role of auditors in providing reasonable assurance about the accuracy and fairness of financial statements.

The article’s detailed explanation of the characteristics, procedures, and assurance levels of audits and reviews serves as an invaluable resource for those seeking to comprehend the intricacies of financial statement evaluation. It’s a comprehensive and insightful analysis of these fundamental assessment processes.

Well articulated, Donna. The article’s comprehensive coverage of the audit and review processes is a commendable effort in elucidating the intricacies of financial statement assessment, offering readers a profound insight into the fundamental disparities between these evaluation mechanisms.

Absolutely, Donna. The article’s meticulous dissection of the key differences between audits and reviews provides readers with a definitive guide to understanding the complexities and nuances inherent in these critical financial evaluation methods.

I find the comparison table of key differences between audits and reviews to be particularly beneficial for those seeking a clear understanding of the distinction between the two processes. This article truly provides a comprehensive breakdown of these essential financial evaluation procedures.

Absolutely, Aiden. The comparison table effectively highlights the nuances in objectives, scope, procedures, and assurance level, making it easier to grasp the intricacies of audits and reviews.

The article presents an insightful and thorough comparison of audits and reviews, providing readers with a comprehensive understanding of the distinctive features and purposes of these financial statement evaluation processes. It’s a highly informative and educative piece that effectively clarifies the complexities of audits and reviews.

I completely agree, Amanda. The article’s meticulous analysis of the critical differences between audits and reviews serves as a definitive guide for anyone seeking to gain a profound understanding of the intricacies that underpin financial statement assessment.

Absolutely, Amanda. The article offers a comprehensive and enlightening comparison of audits and reviews, shedding light on the specific nuances and disparities that distinguish these pivotal financial evaluation procedures.

The article’s thorough exploration of the critical characteristics and differences between audits and reviews is a testament to its informative and enlightening value. It presents a compelling analysis of these essential financial statement evaluation processes, offering readers deep insights into their significance and implications.

The article offers a valuable analysis of the critical features and significance of audits and reviews in assessing financial statements. It’s a well-structured and informative piece, providing clarity on the differences in approach and level of assurance between the two processes.

The detailed comparison between audits and reviews is exceptionally well-crafted, elucidating the nuanced disparities in procedures, assurance levels, and materiality thresholds. It’s an excellent resource for anyone seeking to grasp the intricacies of financial statement evaluation processes.

Absolutely, Morgan. The meticulous breakdown of audit and review processes in the article not only informs but also enlightens readers about the critical distinctions that underpin these financial evaluation mechanisms.

I couldn’t agree more, Morgan. The article’s clarity and precision in dissecting the characteristics and purposes of audits and reviews make it an invaluable source for understanding the fundamental differences between these two vital financial assessment procedures.

While the article presents a thorough comparison of audits and reviews, it may benefit from including real-world examples or case studies to illustrate how audits and reviews are applied in practice, enhancing the practical understanding of readers.

I see your point, Yasmine. Incorporating practical examples could further elucidate the complexities of audits and reviews and their implications for financial reporting, offering readers a more tangible perspective on these processes.

I agree with Yasmine and Holmes. Real-world scenarios would indeed enhance the article’s applicability and facilitate a deeper comprehension of the differences between audits and reviews.

The article provides an excellent overview of audits and reviews, offering a well-structured and comprehensive comparison that sheds light on the fundamental disparities between these financial statement evaluation methods. It’s a highly elucidative and insightful read.

Well said, Jane. The article’s meticulous breakdown of the characteristics and objectives of audits and reviews is a testament to its informative value, making it an indispensable resource for those seeking a deeper understanding of financial statement assessment processes.

While the article’s comparison of audits and reviews is informative, it may benefit from addressing the potential overlap between the two processes and discussing the scenarios in which organizations might opt for reviews over audits, or vice versa, based on their specific requirements and objectives.

I concur with Martin and Millie. Including insights into the decision-making process between audits and reviews would further enrich the article by providing a holistic view of the considerations that inform the selection of these evaluation methods.

I share your viewpoint, Martin. Exploring the practical applications and considerations related to the choice between audits and reviews could indeed enhance the article’s relevance and offer readers a more nuanced understanding of these financial evaluation procedures.