A budget is an official statement of the estimate of income and expenditure during a fixed period based on prior records and plans.

A budget can be made by a person, a team, a company, the government, a business or anyone needing to monitor his/her revenue and expenses. A budget can be classified as Static Or Fixed budget based on its adaptive nature.

Key Takeaways

- Static budgets remain unchanged throughout the period, regardless of actual business performance.

- Flexible budgets adjust according to actual production levels or other relevant factors, allowing for more accurate performance assessment.

- Companies use flexible budgets to better adapt to changing business conditions, while static budgets provide a fixed financial plan.

Static Budget vs Flexible Budget

The difference between Static and Flexible budgets lies in their nature of adaptability. A static budget, once formulated, cannot be changed irrespective of changes occurring in its assumed activity before the fixed period is over. A flexible budget, however is free to be adapted according to changes at any point of the set period.

A static budget is a kind of budget in which the income and expenditure of the concerned body are pre-determined for the upcoming period. Even in the case of any fluctuation of change in the predetermined numbers, it remains static, i.e., the same.

A flexible budget, on the other hand, does not pre-determine the money flow of a period. It is free to change according to the needs of the hour and changes in its activity. It is more sophisticated as it needs to be re-evaluated according to the needs at any time during the reporting period.

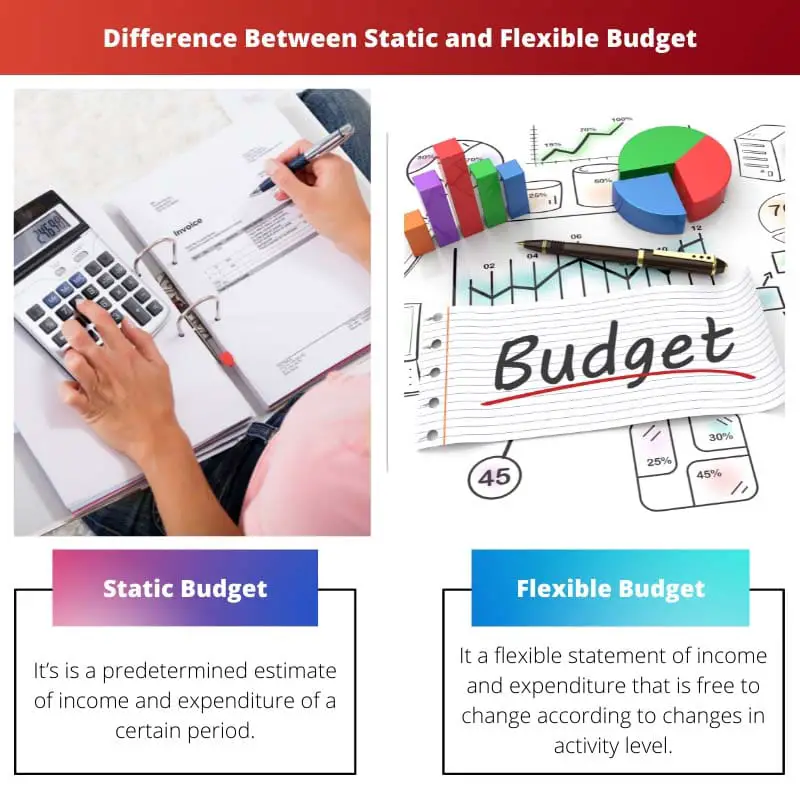

Comparison Table

| Parameters of Comparison | Static Budget | Flexible Budget |

|---|---|---|

| Definition | It’s is a predetermined estimate of income and expenditure of a certain period. | It a flexible statement of income and expenditure that is free to change according to changes in activity level. |

| Assumption | The budget is made assuming there will be no changes in the conditions. | It is designed to change according to needs |

| Degree of adaptability | None | Can be changed at will i.e. it is Dynamic |

| Ease of preparation | Easy to prepare as only one budget with fixed numbers is formed | Highly sophisticated as a series of budgets at different level of changes/activity levels have to be prepared. |

| Time of preparation | Takes less time for preparation | Takes more time of preparation |

| Classification of costs | Costs are not classified into types (variable, fixed or semi-variable) as there exists no variability. | Costs are classified according to the nature of their variability. |

| Comparison | Comparison between budgeted and actual data is difficult if numbers differ | Comparison between budgeted and actual data is easier and realistic. |

| Variance Check | It is easier to check degree of difference between actual and assumed figures (variance) due to it’s static nature | It is very difficult to check variance between data as the budget itself changes according to the activity level |

| Price Fixation | If data varies, price fixation becomes difficult. | Price fixation is easier as difference between data can be met |

| Outcome | It is less effective as change is the only constant . | It is more effective due to its adaptive nature. |

What is Static Budget?

A static budget is the kind of budget in which quantitative figures of income and expenditure of a person, team, business, company or even the government is fixed based on assumptions and prior data collected for a fixed period that can range from a daily basis to annual or even more.

This is a simpler budget to prepare as all figures are predetermined and do not consider any future fluctuation and changes in activity levels. It assumes the conditions will remain constant.

For example, a company estimated its income to be $20 million and expenditure to be $8 million for its annual budget in 2021. However, its income was found to be only $ 16 million at the end of the year.

The difference between the two values is termed a static variance. However, since the assumed data and actual data differed, the cost of goods and price fixation became difficult. Thus although it is effective for variance analysis, it is not realistic as change is the only constant in economies.

A static budget is used by an organization that deals with goods with fixed prices and transactions, government and educational organisations etc.

What is a Flexible Budget?

A flexible budget is the kind of budget that is prepared in a way that allows it to change according to changes in the assumptions made during its preparation.

This is a sophisticated budget to prepare as one has to consider all the changes and variations that can take place in the future reporting period and make a series of budgets to meet specific changes.

One has to have intricate knowledge of which costs are fixed and which are not and prior knowledge of the effect of changes in assumptions. It works with the sales on that changes are bound to happen and hence are designed as flexible.

For example, A business in the fashion industry has a flexible budget as fashion styles change frequently. It is also effective for new ventures as the cost and sales of new ventures are not decided.

Main Differences Between Static Budget and Flexible Budget

- Static Budget is rigid and does not change, while Flexible budget changes according to the relevant situation.

- While preparing a static budget, it is assumed that there will be no fluctuations in the reporting period, while a Flexible budget is designed to adapt to changes.

- A static budget has no degree of adaptability, while a flexible budget, as the name suggests, is flexible.

- It takes a lot more time and experience to formulate a flexible budget than a static budget which is relatively simpler.

- It is difficult to make comparisons between actual and budgeted data if numbers differ in a static budget, while in a flexible budget, it is easier.

- It is also difficult to determine and classify costs in a static budget if data differ, whereas, in a flexible budget, it is easier to attain data as the budget is adjusted according to one’s needs.

- A static budget is rarely used and is not realistic as economies change at all times, while flexible data is a realistic representation of a marketplace.

Flexibility in budgeting is invaluable for addressing the dynamic nature of business, while static budgets can provide a foundational framework for steady financial planning.

The adaptability of flexible budgets allows organizations to better respond to changing business conditions, making them a valuable tool for financial planning.

Both static and flexible budgets have their pros and cons, and it’s essential to choose the right type of budget to meet the specific needs of an organization or individual.

Static and flexible budgets offer distinct advantages in various situations, shaping the financial strategies and decision-making processes of organizations.

Recognizing the roles of static and flexible budgets in different settings, such as government entities and businesses, highlights the diverse applications of budgeting practices.

Static budgets are simpler to prepare, but flexible budgets provide a more accurate assessment of business performance.

Considering the degree of adaptability and ease of variance check, organizations can leverage the strengths of static and flexible budgets to enhance their financial planning and decision-making.

A budget is a crucial tool for any individual or organization to keep track of their finances, and understanding the differences between static and flexible budgets is important for better planning and adaptability.

The impact of static and flexible budgets on price fixation and variance analysis makes it evident that careful consideration is required to select the most suitable budgeting approach.

Understanding the differences between static and flexible budgets is essential for companies to make informed decisions and improve their financial performance.

The comparison between budgeted and actual data is a critical aspect of financial evaluation, and the nature of budgets significantly influences the accuracy and ease of this comparison.

Recognizing the distinct nature of static and flexible budgets in managing financial resources is essential for a comprehensive understanding of budgeting practices across various sectors.

The impact of static and flexible budgets on variance analysis and cost classification provides valuable insights into the implications of budgeting approaches on financial management.

Comparing the nature of adaptability, time of preparation, and ease of variance check between static and flexible budgets clearly illustrates the advantages of each type for different scenarios.

The strategic implications of static and flexible budgets underscore the need for informed decision-making in selecting the most suitable budget to achieve long-term financial objectives.

The outcome of different budgeting approaches in terms of effectiveness and price fixation reflects the strategic implications of selecting the most suitable budget to align with organizational objectives.

The effectiveness of static and flexible budgets in addressing changes in business conditions underscores the need for organizations to align their budgeting practices with their operational environment.

The classification of costs in static and flexible budgets reflects their approach to dealing with variability, and this understanding is essential for effective budget management.

Understanding the appropriateness of static and flexible budgets based on the nature of variability and adaptability is crucial for effective financial planning and decision-making.

Selecting between static and flexible budgets involves weighing their trade-offs and aligning budgeting strategies with the long-term objectives of an organization.

The impact of budget nature on price fixation highlights the strategic implications of selecting the appropriate budgeting approach to achieve financial goals.