Accounting profit represents the explicit monetary gains from business activities, considering only explicit costs like expenses and revenue. Economic profit, however, factors in implicit costs such as opportunity costs and the cost of capital, providing a more comprehensive measure of profitability by considering the full extent of resources employed in a venture. While accounting profit focuses on financial statements, economic profit offers a broader perspective, crucial for decision-making and assessing long-term sustainability.

Key Takeaways

- Accounting profit is the difference between revenue and expenses calculated based on financial accounting principles.

- Economic profit is the difference between total revenue and total cost, including opportunity cost, and is used to measure the long-term viability of a business.

- Accounting profit focuses on the financial performance of a business, while economic gain considers both financial and opportunity costs.

Accounting vs Economic Profit

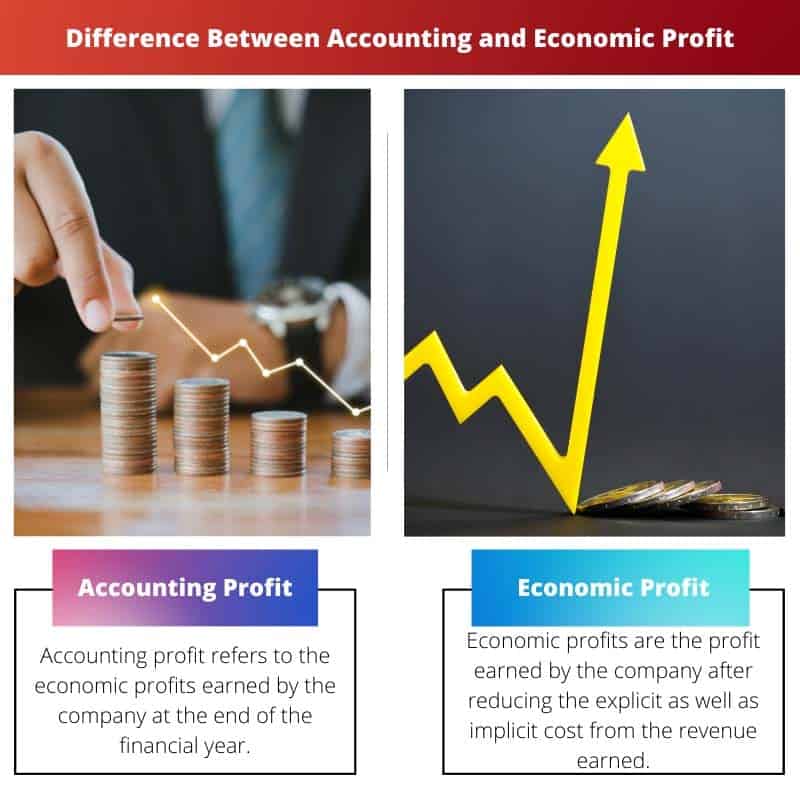

The difference between accounting and economic Profit is that accounting profit refers to monetary revenue minus monetary costs, which includes any type of cost in the organization in the form of rents, salaries, material costs etc. Economic profit refers to the monetary revenue minus total cost. Total cost includes opportunity and implicit costs, including salaries, rents, etc.

Accounting profit consists of only implicit costs, whereas economic profit consists of explicit and implicit costs.

Comparison Table

| Feature | Accounting Profit | Economic Profit |

|---|---|---|

| Purpose | Measures a company’s short-term financial performance based on explicit costs and revenues. | Measures a company’s true profitability by considering all costs, including both explicit and implicit costs. |

| Costs Included | Explicit costs only (e.g., cost of goods sold, operating expenses, salaries, taxes). | Both explicit and implicit costs. |

| Implicit Costs | Not included. | Included (e.g., opportunity cost of capital, implicit rent). |

| Calculation | Total Revenue – Total Explicit Costs | Total Revenue – (Total Explicit Costs + Total Implicit Costs) |

| Interpretation | Indicates a company’s ability to generate profit from its core operations in a specific accounting period. | Indicates a company’s ability to create value for its shareholders by considering the cost of all resources used, including those not explicitly paid for. |

| Limitations | Ignores the time value of money, doesn’t consider risk. | More comprehensive measure, but requires estimating implicit costs, which can be subjective. |

What is Accounting Profit?

Accounting profit is a fundamental concept in financial accounting that serves as a key indicator of a company’s financial performance. It represents the surplus of revenue over explicit costs incurred in generating that revenue during a specific accounting period.

Definition and Calculation

- Revenue: Accounting profit begins with the revenue earned by a company from its primary business activities. Revenue includes sales of goods or services, interest income, rental income, and other sources of income.

- Explicit Costs: Explicit costs are the direct expenses incurred by a company in conducting its business operations. These costs are easily identifiable and quantifiable in financial records. Examples of explicit costs include wages, rent, utilities, raw materials, and advertising expenses.

- Formula: The formula to calculate accounting profit is simple:Accounting Profit=Revenue−Explicit CostsAccounting Profit=Revenue−Explicit Costs

Importance and Applications

- Performance Evaluation: Accounting profit serves as a primary metric for evaluating the financial performance of a company over a specific period. It indicates whether the company is generating more revenue than the costs associated with its operations.

- Investor Analysis: Investors and stakeholders utilize accounting profit to assess the profitability and financial health of a company. Higher accounting profits often indicate better investment opportunities and attract potential investors.

- Taxation: Accounting profit forms the basis for calculating taxes payable by a company to the government. Tax authorities typically impose taxes on the net income derived from business operations, which is closely aligned with accounting profit.

Limitations and Considerations

- Excludes Implicit Costs: Accounting profit does not account for implicit costs, such as opportunity costs and the cost of equity capital. This limitation may lead to an overestimation of the true profitability of a business.

- Short-Term Focus: Accounting profit primarily focuses on short-term financial results and may not provide a comprehensive view of a company’s long-term sustainability and growth prospects.

- Subject to Manipulation: Since accounting profit relies on accounting principles and conventions, it can be influenced by managerial decisions, accounting methods, and adjustments, leading to potential distortions in financial reporting.

What is Economic Profit?

Economic profit is a concept used in economics to measure the true profitability of a business endeavor by considering both explicit and implicit costs. Unlike accounting profit, which only accounts for explicit costs, economic profit factors in the opportunity costs of resources employed in a venture, providing a more accurate assessment of profitability.

Definition and Calculation

- Revenue: Economic profit begins with the revenue generated by a company from its operations, similar to accounting profit.

- Explicit Costs: Like in accounting profit, economic profit considers explicit costs, which are the direct expenses incurred by a company in its business activities.

- Implicit Costs: In addition to explicit costs, economic profit incorporates implicit costs, which represent the opportunity costs of utilizing resources in a particular venture. These costs include the foregone earnings from the next best alternative use of resources, including the owner’s time and the return on invested capital.

- Formula: The formula to calculate economic profit is:Economic Profit=Revenue−(Explicit Costs+Implicit Costs)Economic Profit=Revenue−(Explicit Costs+Implicit Costs)

Importance and Applications

- Holistic Profit Measurement: Economic profit provides a more comprehensive measure of profitability compared to accounting profit by considering all costs associated with a business venture. It offers insights into the true economic value generated by a company’s activities.

- Resource Allocation: By factoring in implicit costs, economic profit aids in optimal resource allocation decisions. It helps businesses identify the most profitable uses of their resources and encourages efficient allocation based on their opportunity costs.

- Long-Term Decision Making: Economic profit is valuable for assessing the long-term viability and sustainability of a business. It enables managers and investors to evaluate whether a venture generates returns that exceed the opportunity costs of the resources invested, guiding strategic decision-making.

Limitations and Considerations

- Subjectivity: Calculating implicit costs, such as opportunity costs, often involves subjective estimates, which may vary among individuals and organizations. This subjectivity can affect the accuracy and reliability of economic profit calculations.

- Complexity: Economic profit analysis can be more complex and time-consuming than accounting profit analysis due to the inclusion of implicit costs. It requires careful consideration of alternative uses of resources and their associated opportunity costs.

- Data Availability: Obtaining accurate data for calculating implicit costs, particularly for intangible resources like time and expertise, may pose challenges, limiting the practical applicability of economic profit analysis in some cases.

Main Differences Between Accounting and Economic Profit

- Scope of Costs:

- Accounting profit considers only explicit costs, such as wages, rent, and materials.

- Economic profit incorporates both explicit and implicit costs, including opportunity costs and the cost of capital.

- Calculation Method:

- Accounting profit is calculated by subtracting explicit costs from revenue.

- Economic profit is calculated by subtracting both explicit and implicit costs from revenue.

- Focus and Application:

- Accounting profit is primarily used for evaluating financial performance and reporting to stakeholders.

- Economic profit provides a broader perspective, aiding in resource allocation decisions, strategic planning, and assessing long-term sustainability.

- https://scholarworks.sjsu.edu/cgi/viewcontent.cgi?article=1037&context=econ_pub

- https://www.bostonfed.org/-/media/Documents/neer/neer498c.pdf

Last Updated : 06 March, 2024

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

While accounting profit focuses on the financial performance of a business, economic profit takes a more comprehensive approach by considering opportunity costs and implicit costs. This distinction is well-articulated in the article, shedding light on the significance of economic profit for long-term strategic decisions.

I found the explanation of economic profit calculation particularly insightful. It’s a valuable metric for businesses to assess their true economic costs and make well-informed decisions for the future.

Indeed, the limitations of accounting profit are effectively explained, particularly in terms of excluding implicit costs and the impact of timing and accruals. This is essential knowledge for anyone involved in financial analysis.

The article provides a comprehensive comparison between accounting and economic profit, highlighting the significance of economic profit for long-term strategic decisions. It’s a valuable resource for businesses seeking a deeper understanding of financial metrics.

I couldn’t agree more. The limitations of accounting profit and the relevance of economic profit for resource allocation are effectively emphasized, offering valuable insights for businesses.

The article effectively outlines the limitations of accounting profit and the timing and accruals involved, providing a comprehensive view of the challenges in evaluating financial performance. It’s a valuable resource for understanding the complexities of financial analysis.

Absolutely, the distinction between accounting and economic profit and the relevance of each for decision-making and strategic planning is well-articulated. It’s an informative read for anyone involved in financial analysis.

I completely agree. The explanation of the limitations of accounting profit is particularly insightful, offering valuable knowledge for businesses and financial analysts.

This article provides an insightful comparison between accounting and economic profit, clearly explaining the differences and nuances between the two concepts. It is a great resource for anyone looking to deepen their understanding of financial metrics.

I completely agree. The detailed breakdown of the components of accounting profit and the calculation formula for economic profit are particularly helpful. It’s a comprehensive analysis.

The significance of accounting profit for performance evaluation and decision-making is well elaborated in the article. It effectively highlights the importance of this financial metric for businesses to assess their growth and financial health.

I completely agree. The explanations of revenue, explicit costs, and their calculation formula provide a clear understanding of accounting profit and its relevance for businesses.

Absolutely, the detailed breakdown of the components of accounting profit and its significance for financial reporting makes this article an excellent reference for financial professionals.

The comparison between accounting profit and economic profit is well-presented in the article, offering a clear distinction and insightful examples. It’s a valuable resource for anyone seeking to enhance their knowledge of financial analysis and decision-making.

Absolutely, the significance of economic profit for long-term viability assessment and the distinction between explicit and implicit costs are effectively articulated. This article is a great reference for understanding the complexities of profitability analysis.

The article effectively explains the calculation of economic profit and its significance for businesses in assessing their true economic costs. It’s a valuable resource for anyone looking to gain insights into the financial performance of a company.

Absolutely, the explanation of economic profit and its calculation formula provides an in-depth understanding of this financial metric. It’s an insightful read for financial professionals and business analysts.

This article provides a comprehensive breakdown of the differences between accounting profit and economic profit, offering detailed explanations and examples to illustrate the concepts. It’s a valuable resource for businesses and financial professionals alike.

I couldn’t agree more. The relevance of economic profit for long-term strategic decisions and resource allocation is particularly emphasized, providing a holistic view of profitability.

The distinction between accounting profit and economic profit is crucial for businesses to make informed decisions and for better understanding of their financial performance. This article does an excellent job in explaining these concepts in a clear and concise manner.

Absolutely, the article effectively highlights the importance of considering both explicit and implicit costs, which is essential for a more accurate assessment of a company’s profitability.

I couldn’t agree more. The comparison table and examples provided make it easy to grasp the key differences between accounting and economic profit, offering valuable insights for businesses.

The comparison table and clear distinction between accounting and economic profit provide a thorough understanding of these financial metrics. The article effectively highlights the pros and cons of each approach, allowing readers to gain valuable insights into the assessment of business profitability.

Absolutely, the limitations of accounting profit and the comprehensive calculation of economic profit are well-presented. This article is a great resource for anyone looking to enhance their financial analysis skills.