A company’s assets and receivables may be classified into two parts: current assets and noncurrent assets. Current assets are assets that the firm will retain in the near term with the goal of turning to money, namely revenue or cash.

Whereas noncurrent assets are retained and collected for a prolonged period of time sufficing for certain 1 to 2 years. Current and noncurrent assets are both necessary for a company’s seamless operation.

There are several distinctions between these two worlds, and this article will ensure that any misconceptions you may have about current and noncurrent assets are dispelled by comparing them side by side and showing their differences.

Key Takeaways

- Current assets, such as inventory and accounts receivable, can be easily converted into cash within one year.

- Noncurrent assets, such as property, plant, and equipment, are long-term investments that require more than a year to liquidate.

- Current assets provide liquidity for day-to-day business operations, while noncurrent assets contribute to a company’s long-term growth and stability.

Current vs Noncurrent Assets

Current assets can be defined as the aggregate of all assets or resources that can be easily converted into cash and will appear on an income statement and balance sheet. Noncurrent assets are assets that are not liquidated in a fiscal year but is left for liquidation. It is left for one or two financial years.

Current assets are the aggregate of all resources or assets that can be quickly and easily converted into cash and appear on an income statement and balance sheet as well. Equity, trade receivables, account balance, and money available are all instances of current assets.

All of these commodities are classed as current assets in financial statements because they may be converted to cash quickly and readily. A few cash alternatives are also included in current assets.

Hence, All assets that may be turned into cash in about one to four years are considered current assets.

Long-term investments and long durational profit bases in which the fair amount will not be recognized within the financial year are referred to as noncurrent assets. They’re opaque or illiquid, which means they can’t be quickly turned into cash.

Some examples of noncurrent assets include securities, proprietary information, estate development, and technological equipment. On a balance sheet of a company, noncurrent assets are listed; however, in a company’s investment statement, these aren’t counted.

Comparison Table

| Parameters of Comparison | Current Assets | Noncurrent Assets |

|---|---|---|

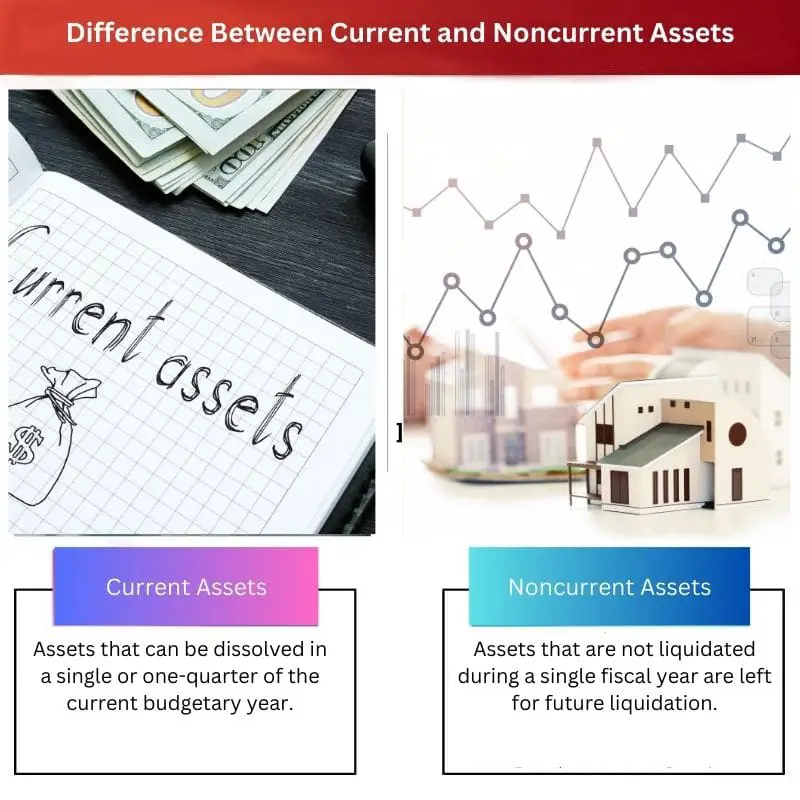

| Meaning | Assets that can be dissolved in a single or one-quarter of the current budgetary year. | Assets that are not liquidated during a single fiscal year are left for future liquidation. |

| Time Duration | A year of time duration is considered for current or immediate assets. | More than one or two financial years. |

| Working Capital | Yes, current assets are counted as working capital. | No, noncurrent assets are not counted as working capital. |

| Value and Market Standard | It is sold at a profitable market value | It is sold at a loss value. Usually lesser than the depreciation value of the asset. |

| Taxes | The taxes result in a business profit since the asset is sold in financial profit. | The taxes result is a business loss. |

What is a Current Asset?

When accounting information is constructed based on availability, “current assets” consist of liquid assets and cash or similar assets that can be instantaneously used up, which is the first budget item on the resource side of the company’s balance sheet. Commercial papers, which are as liquid as cash, are commonly used as cash equivalents.

Trade payables are a type of current asset that means the amount of money owed to the firm by borrowers to whom it has sold products on credit.

Another important current asset is stocks; each firm must keep a certain amount of inventory to operate, but both excessive and low inventory holding costs are undesirable.

Current assets are the working capital of the organization and are considered very resourceful since they have a short stay-time, and these can incur good amounts of business profit for the organization. These assets are the most important because they are included in the company’s balance sheet.

These assets are sold at market value and sometimes higher. Functioning resources, aka the current assets, are important to a business because they are used to finance the company’s working capital needs.

Every business needs money to meet the daily obligations that come with doing business.

Since liquid assets can be liquidated in a short time, it is important for management to adapt to their short-term financing needs.

What is Noncurrent Asset?

A noncurrent asset is an asset that is not sold for a period of one year. These assets are also presented in a company’s financial statements.

Long-term assets are not liquid like current assets and are not held to sell them in the short term because they are kept for future purposes, maybe or may not be for-profit gain.

One of these types of long-term assets is long-term investments consisting of equity and debt, which will be held by the company for a long time. Long-term assets also include the ownership rights a company has in other businesses.

A noncurrent asset is more required to stay functional and prosper with time instead of the immediacy factor considered in current assets.

Noncurrent assets include an industry’s positive reputation, registered trademark, intellectual property, patent protection, and so on. Companies spread overall costs throughout several years since noncurrent assets have a longer useful life.

This procedure aids in the avoidance of significant losses during periods of capital expansion.

Noncurrent assets, such as property or equipment and everything that is tangible and is responsible for the workforce, are instances of noncurrent assets. Intangible resources include long-term holdings such as debt securities or estate development and financial assets in other companies.

Intangible long-term assets include copyrights, customer databases, and goodwill obtained through a business combination.

Main Differences Between Current and Noncurrent Assets

- Current assets are easily liquidated, but liquidating noncurrent assets is a tough job for the people of organizations.

- Holding time for current assets is one to quarter years, whereas noncurrent assets stay longer with lesser market value.

- Current assets are a part of the working capital, whereas noncurrent assets are not part of the working capital.

- Current assets are immediate, like cash and receivables, whereas noncurrent assets are kept for late usage, like furniture and electronics.

- The sale of current assets results in business profit, but sales of noncurrent assets result in business loss or a lesser chance of being a business profit.

- https://corporatefinanceinstitute.com/resources/knowledge/accounting/current-assets/

- https://groww.in/p/non-current-assets/

Last Updated : 13 July, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The explanation of current and noncurrent assets in this article was very detailed and easy to understand. It’s a valuable resource for anyone looking to expand their financial knowledge.

This article effectively highlights the importance of current and noncurrent assets in a company’s financial structure. I appreciated the detailed comparison table that clearly outlines their differences.

I highly appreciate the comprehensive comparison between current and noncurrent assets presented in this article. The key takeaways and clear definitions make it easier for readers to comprehend the topic.

This post did a great job of illustrating the importance of both current and noncurrent assets in a company’s operations. Definitely worth the read for anyone looking to increase their financial knowledge.

This article dispelled any misconceptions I had about current and noncurrent assets. I found it extremely helpful and insightful in understanding the financial aspects of a company.

I found the article quite informative and well-explained. It provides a clear understanding of the differences between current and noncurrent assets, which is essential for everyone interested in understanding company finances.

The article provided a comprehensive overview of the differences between current and noncurrent assets. It’s beneficial for those looking to gain a deeper understanding of financial concepts.

It’s essential to understand the distinctions between current and noncurrent assets, and this article did a fantastic job of breaking it down in a concise manner. A great resource for anyone interested in learning more about company finances.