A current account is a basic bank account that allows deposits, withdrawals, and day-to-day transactions. An overdraft, on the other hand, is a facility provided by the bank allowing the account holder to withdraw more money than is available in the account, subject to certain limits and conditions. While a current account serves as a means of managing regular finances, an overdraft offers a temporary buffer for covering short-term expenses beyond the available balance.

Key Takeaways

- Overdraft is a credit facility allowing a current account holder to withdraw more money than is available up to a pre-approved limit. In contrast, a current account is a bank account used for day-to-day transactions.

- Overdrafts come with high-interest rates and fees, while current accounts may have lower fees and interest rates.

- Overdrafts and current accounts are used for managing money and transactions, but overdrafts provide short-term credit.

Overdraft vs Current Account

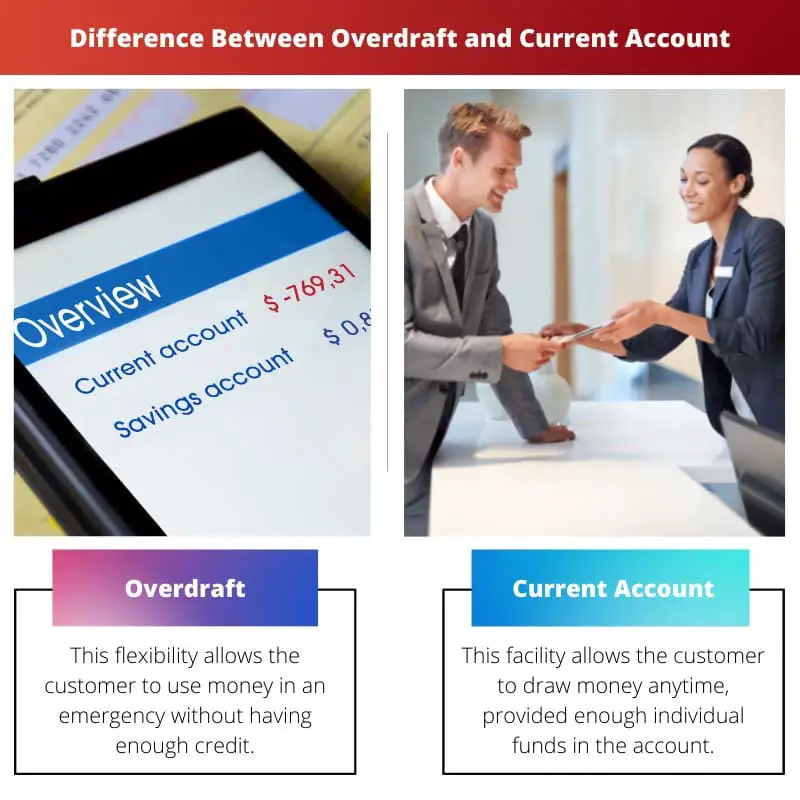

A person can withdraw money from an overdraft account even if their balance is nil. It can be a type of loan which the person has to pay or return within a given time period. A person can withdraw money from a current account at any time. An ATM can also be used to withdraw money. Current accounts can be of different types.

An overdraft is issued by the bank when the account balance is low or zero. Overdraft enables the customer to have less financial burden.

The current account gives easy access to the money in the bank account. Usually, cash in the existing version doesn’t accumulate interest.

This enables the customer to withdraw as much money as possible. This account is used for business purposes.

Comparison Table

| Feature | Overdraft | Current Account |

|---|---|---|

| Definition | A short-term borrowing facility linked to a current account, allowing you to spend more than you have in your balance | A bank account used for everyday transactions like depositing, withdrawing, and transferring money |

| Purpose | To cover temporary shortfalls in your finances, allowing you to make payments even if your balance is insufficient | To manage your everyday finances, including receiving income, paying bills, and making purchases |

| Availability | Not guaranteed, requires approval from the bank based on your financial situation | Generally available to anyone who meets the bank’s eligibility criteria |

| Interest charged | Yes, high interest rates are charged on the amount you borrow and the duration you stay in overdraft | No interest earned on your account balance |

| Fees | May incur additional fees like unarranged overdraft charges or returned payment fees | May have monthly account maintenance fees or fees for specific services like international transactions |

| Impact on credit score | Frequent use or exceeding the limit can negatively impact your credit score | No direct impact on your credit score, but responsible management can build your credit history positively |

What is Overdraft?

How Does Overdraft Work?

1. Authorized Limit:

Banks set an authorized overdraft limit for each account holder based on factors such as credit history, income, and banking relationship. This limit represents the maximum amount that can be overdrawn from the account.

2. Usage and Charges:

When an account holder makes a transaction that exceeds the available balance, the overdraft facility is automatically activated. The bank covers the shortfall, allowing the transaction to proceed. However, this service incurs fees or interest charges, which vary depending on the bank and the terms of the overdraft agreement.

3. Repayment:

Overdrafts are intended for short-term use and should be repaid promptly to avoid accumulating interest charges. Account holders can replenish their account by depositing funds or receiving income. Some banks may also offer repayment plans to help customers manage and clear their overdraft balances over time.

Benefits and Risks of Overdraft:

Benefits:

- Provides flexibility and convenience for managing cash flow.

- Helps account holders cover unexpected expenses or emergencies.

- Can prevent declined transactions and associated fees.

Risks:

- Overuse of overdraft can lead to debt accumulation and financial strain.

- Fees and interest charges can be high, increasing the cost of borrowing.

- Failure to repay overdrafts promptly may harm credit scores and banking relationships.

What is Current Account?

Features and Functions of a Current Account:

1. Deposits and Withdrawals:

- Account holders can deposit funds into their current accounts through various channels, including cash deposits, electronic transfers, and cheque deposits.

- Withdrawals can be made either through ATMs, over-the-counter transactions, electronic transfers, or through debit card transactions.

2. Payments and Transactions:

- Current accounts facilitate various types of payments, including bill payments, utility payments, and purchases.

- Transactions such as direct debits, standing orders, and electronic transfers can be set up to automate regular payments.

3. Overdraft Facility:

- Many current accounts offer an overdraft facility, allowing account holders to withdraw more money than is available in their account, up to a pre-agreed limit.

- Overdrafts provide a temporary financial cushion to cover short-term cash flow gaps or unexpected expenses, subject to fees and interest charges.

4. Account Management:

- Current accounts come with features for managing account activities, such as online banking, mobile banking apps, and telephone banking.

- Account statements, transaction histories, and balance inquiries are easily accessible through these platforms, enabling account holders to monitor their finances effectively.

Benefits and Considerations of a Current Account:

Benefits:

- Convenience: Current accounts offer easy access to funds for day-to-day financial needs, including payments and withdrawals.

- Flexibility: Account holders have the flexibility to manage their finances efficiently through various banking channels and transaction options.

- Security: Funds held in a current account are safe and protected by banking regulations and deposit insurance schemes.

Considerations:

- Fees and Charges: Some current accounts may have maintenance fees, transaction fees, and other charges, depending on the bank and the type of account.

- Interest Rates: While some current accounts may offer interest on deposits, the rates are lower compared to savings accounts or other investment options.

- Overdraft Costs: Utilizing the overdraft facility can result in fees and interest charges, so it’s essential to understand the terms and costs associated with overdraft usage.

Main Differences Between Overdraft and Current Account

- Purpose:

- Overdraft: Provides a temporary borrowing facility allowing account holders to withdraw more money than is available in their account, for short-term cash flow needs or emergencies.

- Current Account: A basic bank account primarily used for day-to-day transactions, deposits, withdrawals, and managing regular finances.

- Availability of Funds:

- Overdraft: Allows account holders to temporarily exceed their account balance up to a pre-agreed limit, subject to fees and interest charges.

- Current Account: Holds funds deposited by the account holder and can be accessed for transactions, payments, and withdrawals within the available balance.

- Usage and Costs:

- Overdraft: Incurs fees and interest charges when utilized, with costs varying depending on the amount borrowed and the terms of the overdraft agreement.

- Current Account: Generally does not involve borrowing costs unless an overdraft facility is used, but may have transaction fees, maintenance fees, or other charges depending on the bank and account type.

- Duration of Use:

- Overdraft: Intended for short-term use to cover temporary cash flow gaps or unexpected expenses, with repayment expected promptly to avoid accumulating interest charges.

- Current Account: Used for ongoing management of day-to-day finances and transactions, with funds deposited and withdrawn as needed without the expectation of immediate repayment.

- Access and Management:

- Overdraft: Managed alongside the current account, accessible through online banking, mobile banking apps, and other banking channels, with overdraft limits and usage displayed alongside account balances.

- Current Account: Offers various means of access and management for transactions, payments, and account monitoring, including online banking, mobile apps, ATMs, and in-branch services.

- https://www.nber.org/papers/w17028.pdf

- https://heinonline.org/hol-cgi-bin/get_pdf.cgi?handle=hein.journals/fedred81§ion=193

- https://www8.gsb.columbia.edu/programs/sites/programs/files/images/Paper1_XiaoLiu.pdf

Last Updated : 04 March, 2024

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The article provides a useful comparison, but it could benefit from some real-world examples to further illustrate the points.

I agree with your point, some practical examples would definitely enhance the understanding of the differences.

While real-world examples could be helpful, the information presented is clear and concise, making it easy to grasp the concept.

The detailed descriptions of overdraft and current accounts are enlightening; it’s a rich source of knowledge for banking enthusiasts.

Absolutely, the depth of information provided is certainly a valuable resource for those interested in banking.

I couldn’t agree more, the level of detail and insight presented is truly impressive.

While the article is informative, it could benefit from a more engaging tone to captivate the reader’s interest.

I see your point, a more engaging approach could make the content even more compelling.

I personally found the straightforward and informative nature of the post to be engaging enough.

A very well-researched and articulate post, shedding light on the intricate details of both account types.

I share your sentiment, the thoroughness of the information is truly commendable.

I appreciate the detailed explanation of the specific eligibility criteria for overdraft facilities, it adds credibility to the information presented.

The focus on eligibility criteria indeed adds depth to the understanding of overdraft accounts and their usage.

This comprehensive explanation effectively demystifies the complexities of overdraft and current accounts, making it accessible to a wide audience.

Absolutely, the content caters to both novice and experienced individuals in the realm of banking.

The comparison table is a great addition, providing a clear and structured overview of the differences between overdraft and current accounts.

The comparison table is definitely a highlight, simplifying the understanding of complex banking terms.

I couldn’t agree more, the tabular format makes it easy to compare and contrast the two account types.

The post covers the essential aspects of overdraft and current accounts in a well-structured manner, offering a wealth of information for readers.

I concur, the post is a treasure trove of knowledge for anyone seeking to understand the nuances of banking.

The post effectively highlights the crucial differences between overdraft and current accounts along with their respective benefits, a very informative read.

I couldn’t agree more, the detailed insights into the benefits of each account type are truly valuable.

Absolutely, the comparison is well-structured and factually sound.

This article provides a comprehensive and detailed comparison between overdraft and current accounts, making it very easy to understand the key differences and benefits of each.

I found the comparison table to be particularly helpful in understanding the nuances of overdraft and current accounts.

I completely agree, the author has done a great job of breaking down complex banking terms into simpler concepts.