A business or a company holds many assets which can be instantly converted into cash whenever the company or the business needs it. These assets are purchased with the generated money as revenue.

A thing that has a financial value to it is called an asset. Assets can be of different types that are easily and securely exchanged whenever required.

Current assets and liquid assets are used to determine or analyze the short-term situation of a company or a business using ratio analysis.

Key Takeaways

- Current assets include cash, cash equivalents, and other assets expected to be converted to cash or used up within one year. In contrast, liquid assets are specifically cash or assets that can be easily and quickly converted to cash.

- Liquid assets provide more immediate financial flexibility for a company, as they can be used to cover short-term liabilities or fund operations.

- Current assets encompass a broader range of assets, such as inventory and accounts receivable, which may not be as easily or quickly convertible to cash as liquid assets.

Current Assets vs Liquid Assets

Current assets are expected to be converted into cash within a year or a normal operating cycle of a business. Liquid assets are assets that can be easily and quickly converted into cash without significant loss in value, and this includes cash and accounts receivable.

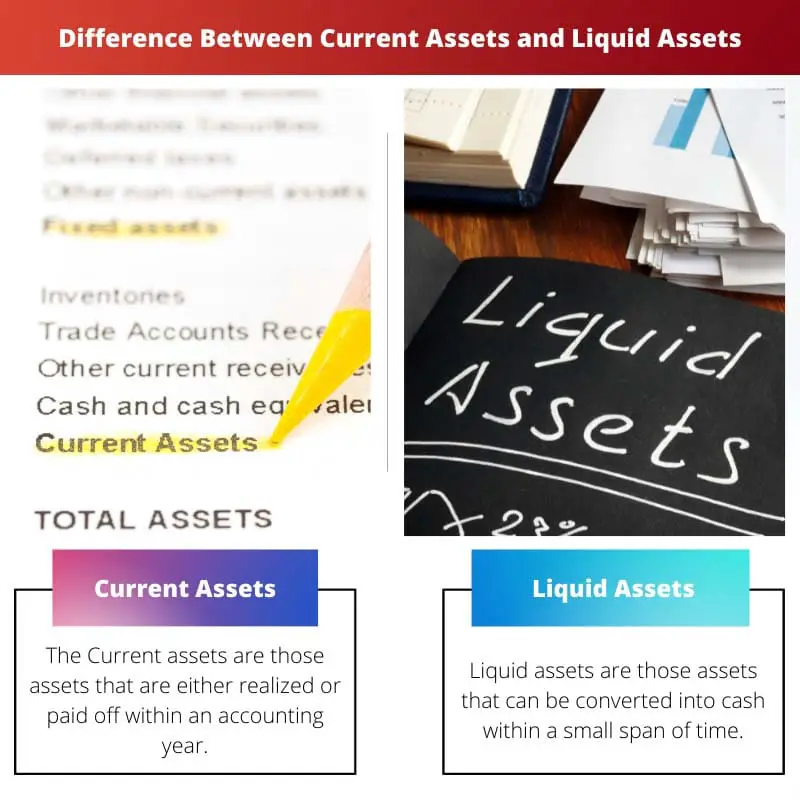

The Current assets are those assets that are either realized or paid off within an accounting year. The value of Current assets is calculated on the lower value between the cost value and the market value.

Current assets are converted into liquid form to pay off the current liabilities.

Liquid assets are those assets that can be converted into liquid form or cash within a small span of time. Liquid assets are converted into their liquid form or cash form while keeping the market value.

Comparison Table

| Parameters of Comparison | Current assets | Liquid assets |

|---|---|---|

| Difference | The Current assets are those assets that are either realized or paid off within an accounting year. | Liquid assets are those assets that can be converted into cash within a small span of time. |

| On financial statement | Current assets are shown on the debit side of the financial statement. | Liquid assets are a part of the current assets. |

| Convertibility to cash | Current assets are less easily convertible than Liquid assets. | The liquid assets are already in the liquid form or get easily converted. |

| Decision making | Current assets are used to evaluate the liquidity of the company. | Liquid assets can be used to highlight liabilities. |

| Examples | Some examples of current assets are cash in the bank, cash in hand, debtor, short-term investments, bill receivables, prepaid expenses, inventories, etc. | Some examples of Liquid assets are cash in the bank, cash in hand, cash equivalents, mutual funds, stocks, treasury bills, bonds, prepaid expenses, accrued income, Government Bonds, Marketable Securities, etc. |

What are Current Assets?

The Current assets are those assets that are either realized or paid off within an accounting year. They are also called short-term assets or circulating assets, circulating capital, or floating assets.

These assets are easily converted to cash and thus are very liquid or already available in liquid form.

Usually, in a business, current assets are converted into liquid form to pay off the current liabilities.

Current assets are shown as different heads in the financial statements. The value of Current assets is calculated on the lower value between the cost value and the market value.

Current assets are used to calculate the current ratio for a business or company. Current assets are less easily convertible than Liquid assets.

Short-term funds are used while financing the current assets. Current assets generate a floating charge.

Some examples of current assets are cash in the bank, cash in hand, debtor, short-term investments, bill receivables, prepaid expenses, inventories, etc.

What are Liquid Assets?

Liquid assets are those assets that can be converted into cash within a small span of time. Liquid assets are converted into their liquid form or cash form while keeping the market value.

Liquid assets are easily convertible in the liquid form or the cash form than the current assets.

Cash in hand is the most liquid asset present in the company or a business, followed by funds that a company or a business can withdraw.

Liquid assets are a part of the current assets. Buyers or businesses use this type of asset.

Some examples of Liquid assets are cash in the bank, cash in hand, cash equivalents, mutual funds, stocks, treasury bills, bonds, prepaid expenses, accrued income, Government Bonds, Marketable Securities, etc.

Main Differences Between Current Assets and Liquid Assets

- Current assets are assets that are either realized or paid off within an accounting year, whereas Liquid assets are those that can be converted into cash within a short time.

- Current assets are less easily convertible than Liquid assets, whereas liquid assets are already in liquid form or get easily converted.

- Some examples of current assets are cash in the bank, cash in hand, debtor, short-term investments, bill receivables, prepaid expenses, inventories, etc whereas Some examples of Liquid assets are cash in the bank, cash in hand, cash equivalents, mutual funds, stocks, treasury bills, bonds, prepaid expenses, accrued income, Government Bonds, Marketable Securities, etc.

- Current assets are shown on the debit side of the financial statements, whereas Liquid assets are a part of the current assets.

- Current assets are used to evaluate the liquidity of the company, whereas Liquid assets can be used to highlight the liabilities.

- https://hrcak.srce.hr/index.php?show=clanak&id_clanak_jezik=333863

- https://repository.vnu.edu.vn/handle/VNU_123/77056

This article gives a comprehensive overview of current and liquid assets, which is very informative to business students. The comparison table is particularly helpful for a clear understanding.

The post does a great job explaining the differences between current and liquid assets. The examples used to illustrate each of their concepts make the article easy to understand.

I find the article to be quite educational and engaging, providing in-depth knowledge about the differences between current and liquid assets. It could have included a case study to further illustrate the concepts.

The article explains the key concepts of current and liquid assets concisely. However, some real-life examples from well-known companies/corporations would have been beneficial.

The article provides a good amount of information about current and liquid assets. It helps to clarify which assets offer more immediate financial flexibility.

The article lacks clarity on the practical implications and applications of understanding the differences between current and liquid assets. This diluted the depth of the article.