GST (Goods and Services Tax) is a consumption tax levied on the supply of goods and services, aiming to replace multiple indirect taxes. TDS (Tax Deducted at Source) is a mechanism for collecting income tax at the source from where income is generated, applicable on various payments like salary, interest, commission, etc., to ensure tax compliance.

Key Takeaways

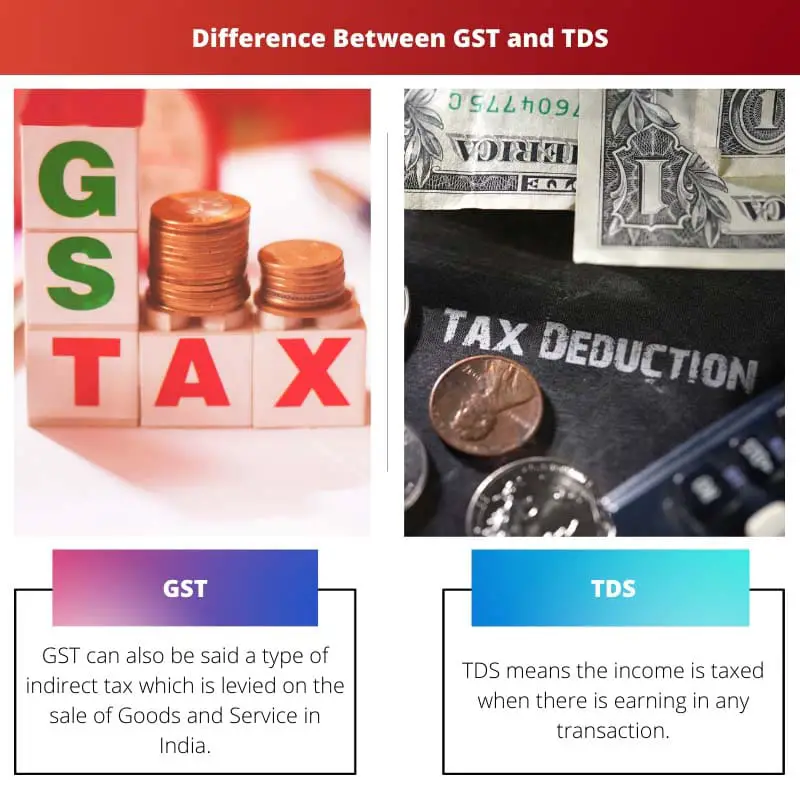

- GST stands for Goods and Services Tax and is a consumption tax levied on the supply of goods and services in India, while TDS stands for Tax Deducted at Source and is a form of income tax deducted from the income source itself.

- GST is a value-added tax collected by businesses and paid to the government. At the same time, TDS is deducted by employers or other entities from income and paid to the government on behalf of the recipient.

- GST and TDS are both types of taxes used in India, but they are applied in different ways and serve different purposes.

GST vs TDS

GST, or Goods and Services Tax, is a comprehensive indirect tax levied on the supply of goods and services, applied at every stage of production. TDS, or Tax Deducted at Source, is a system where tax is deducted at the origin of income, applied to income sources such as salaries, interest on savings, etc.

GST is a percentage of income generated from profit or loss from selling goods or services, payable on completing the business. In TDS, the tax is deducted at source, giving the government an advantage over people who either forget to pay tax or hide their transactions not paying it.

It makes sure that income is deducted in advance from the payments.

Comparison Table

| Feature | GST (Goods and Services Tax) | TDS (Tax Deducted at Source) |

|---|---|---|

| Purpose | Indirect tax levied on the supply of goods and services | Direct tax deducted at the source of income |

| Applicability | Applies to businesses registered under GST | Applies to various income sources like salaries, rent, professional fees, etc. |

| Who pays? | The registered supplier of goods and services | The deductor (payer) responsible for making the payment |

| Who collects? | Government | Government |

| Rate | Varies based on the type of goods and services (0%, 5%, 12%, 18%, 28%) | Varies based on the nature of income and the applicable section of the Income Tax Act |

| Payment mechanism | Filed and paid electronically through the GST portal | Deducted at the time of payment and deposited with the government by the deductor |

| Filing frequency | Varies depending on the turnover of the business (monthly, quarterly, yearly) | Varies depending on the type of income and the deductor’s category |

| Impact on final tax liability | Credited towards the final GST liability of the recipient | Can be claimed as a deduction by the deductee while filing their income tax return |

| Applicability in GST regime | Separate from GST, but TDS applies to certain transactions under GST, like payments for rent, professional fees, etc. |

What is GST?

Introduction to GST:

GST, which stands for Goods and Services Tax, is a comprehensive indirect tax levied on the supply of goods and services in India. It is one of the most significant tax reforms in the country’s economic history, aiming to streamline the taxation system by replacing multiple indirect taxes imposed by the central and state governments.

Key Features of GST:

- Destination-Based Taxation: GST follows a destination-based taxation principle, wherein the tax is levied at the point of consumption rather than the point of origin. This ensures that revenue is collected by the state where the goods or services are consumed, promoting a more equitable distribution of tax revenue among states.

- Dual GST Structure: GST in India operates under a dual structure, comprising Central Goods and Services Tax (CGST) levied by the central government and State Goods and Services Tax (SGST) imposed by the respective state governments. This dual system ensures that both the central and state governments have the authority to levy and collect taxes on the same transaction, thereby enhancing fiscal autonomy.

- Comprehensive Tax Base: GST subsumes various indirect taxes such as Central Excise Duty, Service Tax, Value Added Tax (VAT), Octroi, Entry Tax, and others, simplifying the tax regime and reducing cascading effects. By broadening the tax base and eliminating tax-on-tax incidence, GST aims to enhance efficiency, transparency, and compliance in the tax system.

- Input Tax Credit: One of the fundamental features of GST is the provision for claiming Input Tax Credit (ITC). Businesses can offset the GST paid on input goods and services against the GST liability on output supplies. This mechanism eliminates the cascading effect of taxes and promotes the concept of tax neutrality across the supply chain, encouraging better compliance and reducing the overall tax burden on businesses.

- GST Council: The GST Council, consisting of representatives from the central and state governments, plays a crucial role in formulating policies, making recommendations, and deciding on key aspects such as tax rates, exemptions, and threshold limits. This collaborative approach ensures cooperative federalism and facilitates consensus-driven decision-making in the implementation and administration of GST.

What is TDS?

Introduction to TDS:

Tax Deducted at Source (TDS) is a mechanism used by the government to collect income tax at the source of income generation. It is applicable to various payments made by individuals, businesses, or entities, ensuring that tax is deducted upfront before the recipient receives the payment.

Key Features of TDS:

- Collection of Tax at Source: TDS operates on the principle of collecting tax at the source of income itself. This means that the payer deducts a certain percentage of tax from the payment made to the payee and deposits it with the government on behalf of the payee. Common instances of TDS include salary, interest, rent, commission, and professional fees.

- Legal Provisions and Rates: TDS is governed by the Income Tax Act, 1961, and various rules and regulations issued by the Income Tax Department. The Act specifies the rates at which TDS should be deducted based on the nature of payment and the status of the payee. These rates may vary for different types of payments and are subject to periodic revisions by the government.

- Tax Deduction Certificate: Upon deduction of TDS, the payer is required to issue a Tax Deduction Certificate (TDS certificate) to the payee, indicating the amount of tax deducted and deposited with the government. This certificate serves as proof of tax deduction and can be used by the payee to claim credit for the TDS amount while filing their income tax return.

- Role of Deductor and Deductee: In the TDS process, the individual, entity, or business making the payment is referred to as the “deductor,” while the recipient of the payment is known as the “deductee.” It is the responsibility of the deductor to deduct TDS at the applicable rates and deposit it with the government within the stipulated time frame. The deductee, on the other hand, must ensure that the TDS deducted is correctly reflected in their income tax return and claim credit for the same.

- Compliance and Penalties: Non-compliance with TDS provisions can attract penalties and interest under the Income Tax Act. Failure to deduct TDS or delay in depositing the deducted amount can lead to penal consequences for the deductor. Similarly, if the deductee fails to furnish the TDS certificate or misrepresents information related to TDS, they may face penalties or scrutiny from the tax authorities.

Main Differences Between GST and TDS

- Tax Type:

- GST: Goods and Services Tax is a consumption tax levied on the supply of goods and services.

- TDS: Tax Deducted at Source is a mechanism for collecting income tax at the source of income generation.

- Scope of Application:

- GST: Applicable on transactions involving the supply of goods and services.

- TDS: Primarily applicable on various payments such as salary, interest, rent, commission, etc.

- Objective:

- GST: Aims to streamline the taxation system by replacing multiple indirect taxes and promoting a unified national market.

- TDS: Aims to collect income tax at the source to ensure tax compliance and prevent tax evasion.

- Authority:

- GST: Administered by the GST Council at both central and state levels.

- TDS: Administered by the Income Tax Department under the authority of the central government.

- Mechanism:

- GST: Involves the collection of tax at each stage of the supply chain and allows for input tax credit.

- TDS: Involves deducting a certain percentage of tax from payments made to the recipient and depositing it with the government on behalf of the recipient.

- Nature of Tax:

- GST: Indirect tax.

- TDS: Direct tax.

- Applicability Across Transactions:

- GST: Applicable to all transactions involving the supply of goods and services, subject to certain thresholds and exemptions.

- TDS: Applicable to specific types of payments exceeding specified thresholds, depending on the nature of the payment and the status of the recipient.

- Compliance Requirements:

- GST: Requires businesses to register, file periodic returns, and maintain proper accounting records.

- https://www.icicibank.com/knowledge-base/tax/about-tds.page

- https://www.ajol.info/index.php/wsa/article/view/116183

- https://rrjournals.com/wp-content/uploads/2018/11/884-886_RRIJM180310178.pdf

Last Updated : 02 March, 2024

Emma Smith holds an MA degree in English from Irvine Valley College. She has been a Journalist since 2002, writing articles on the English language, Sports, and Law. Read more about me on her bio page.

The advantages and disadvantages of GST and TDS are well listed. It helps to evaluate the impact of both taxation systems effectively.

Agreed, the detailed advantages and disadvantages provide a clear understanding of the implications of both tax systems.

I found the comparison table particularly insightful. It highlights the implications and importance of both GST and TDS with great clarity.

The explanation of TDS as a form of income tax deducted at the source is quite thorough and informative.

I agree. It provides a comprehensive understanding of how TDS functions within the tax system.

The comparison between GST and TDS is very well explained, making it easier to understand the key differences between the two.

Absolutely, the distinction between GST and TDS is crucial and this article does a great job of clarifying it.

The distinction between GST and TDS is well-detailed, making it easier to comprehend the nuances of both tax systems.

Agreed. It’s a very insightful analysis that sheds light on the differences between GST and TDS.

Absolutely, the detailed comparison helps in understanding the practical implications of both taxation systems.

This article provides a comprehensive understanding of the taxation landscape in India, which is crucial for informed decision-making.

The detailed comparison between GST and TDS is very helpful for understanding the nuances of both taxation systems.

Absolutely, the article offers a clear and comprehensive overview of the differences and applications of GST and TDS.

I would like to see more information about the implementation of GST and TDS in practice, along with real-life examples.

The in-depth overview of what GST entails, including its impact on various taxes, is quite enlightening.

I agree. It’s a very informative read that provides clarity on the taxation landscape in India.

The abolition of interstate checkposts due to GST has significantly improved the movement of goods across states, which is a huge advantage.

Agreed. It’s an important step towards creating a unified market for goods and services in India.

I completely agree. It has certainly made a positive impact on the national common market as well.

The advantages and disadvantages of both GST and TDS are well-stated, but it’s important to consider practical implications and challenges too.

Absolutely, while the comparison is helpful, practical scenarios and challenges in implementing these tax systems are crucial to understand.