Several types of budgeting techniques are available, which help a person or a company to maintain or control their expenses and to know their profits or losses at the end of the year or month.

Incremental Budgeting and Zero-Based Budgeting are two types of budgeting methods that allow a person or a company to balance their expenses with their income or financial turnover.

Key Takeaways

- Incremental budgeting uses the previous year’s budget as a baseline, making small adjustments for the new fiscal year.

- Zero-based budgeting starts from scratch, requiring a full review and justification of all expenses.

- Zero-based budgeting is more time-consuming but can lead to more efficient resource allocation.

Incremental Budgeting vs Zero-Based Budgeting

Incremental budgeting involves slightly altering the existing budget plan to arrive at a new one or doing some premise changes, but it involves complex calculations. Zero-based budgeting is the process of starting the budget from scratch with each line item set at zero before being reviewed each year.

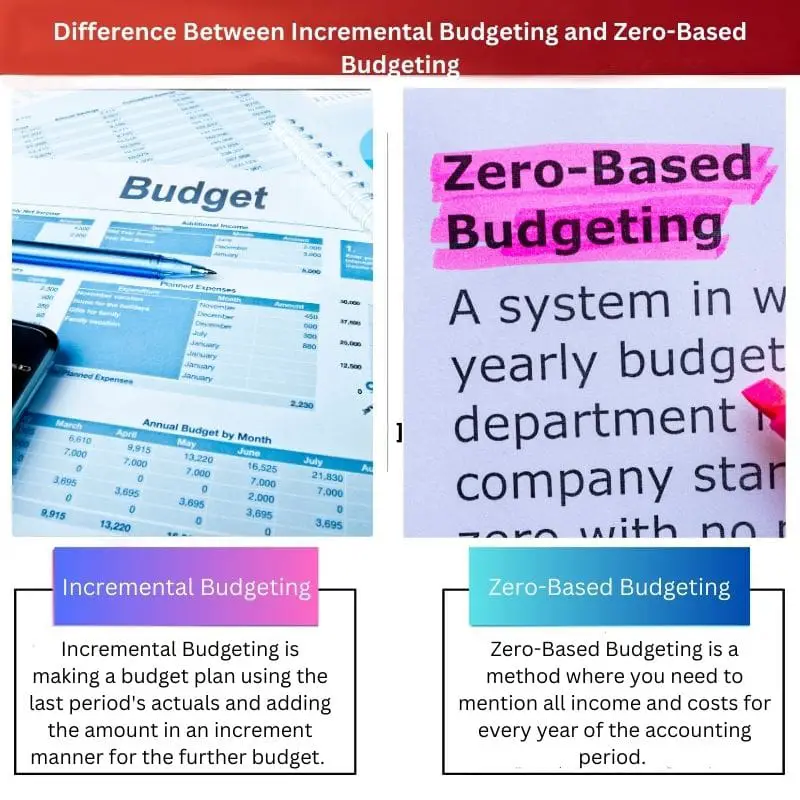

Incremental Budgeting is altering the existing budget plan or doing premise changes to arrive at a new budget plan. This method is not easy to implement, and the calculations made are complex.

Zero-based Budgeting starts everything from scratch. Where each line item is set at zero every year, and every line item is reviewed or justified each year. It ensures funding stability and uses a top-down approach.

Comparison Table

| Parameters of Comparison | Incremental Budgeting | Zero-Based Budgeting |

|---|---|---|

| Definition | Incremental Budgeting is making a budget plan using the last period’s actuals and adding the amount in an increment manner for the further budget. | Zero-Based Budgeting is a method where you need to mention all income and costs for every year of the accounting period. |

| Open to suggestions | Incremental Budgeting is less reactive when it comes to market changes or fluctuations. | Zero-Based Budgeting is very adaptive when it comes to integrating changes in the market. |

| Cost and time | Incremental Budgeting uses more time, but it is economical or cost-efficient. | Zero-Based Budgeting is time-consuming as well as expensive because it covers every detail. |

| Approach | Incremental Budgeting mainly keeps track of the expenditures or spending. | Zero-Based Budgeting monitors the acquirement of the intent or objective. |

| Importance | It is accounting-oriented and focuses only on the cost. | Zero-Based Budgeting is decision-oriented. |

| Procedure | Incremental Budgeting is based on extrapolation. That is, future projections are carried out from the previous figures. | The zero-Based Budgeting decision package is based on cost-benefit analysis. |

What is Incremental Budgeting?

Incremental Budget planning uses past data and makes changes to it. In this technique, the administration supposes that the measures of earnings and costs collected during the present year will also be returned in the coming year.

The results of the current budget plan are summed up and added to next year’s budget plan. And subtle changes are made, like in selling price, related income, and other increases in the actual prices.

Incremental Budgeting easily gets affected by subtle changes in the market as it is not very adaptive. The main focus of this method is only on the cost, no matter how complicated are the budget and expenses.

What is Zero-Based Budgeting?

Zero-Based Budgeting is a methodology in which you need to specify all incomes made and expenses made every new year during budgeting.

This budget plan is very adaptive and market-friendly. And it is proven more accurate than Incremental Budgeting as everything in this budget plan is considered from the base or scratch, which makes it more effective and adaptive.

Zero-Based Budgeting plan managers need to specify and justify all the financial collections and expenditures for the next budget plan to ensure that the budget plan made is free from all previous mistakes and expenditure failures.

Main Differences Between Incremental Budgeting and Zero-Based Budgeting

- Zero-Based Budgeting monitors the acquirement of the intent or objective. While Incremental Budgeting mainly keeps track of expenditures or spending.

- Zero-Based Budgeting is very adaptive when it comes to integrating changes in the market. But Incremental Budgeting is less reactive when it comes to market changes or fluctuations.

- https://www.jstor.org/stable/4531961

- https://onlinelibrary.wiley.com/doi/abs/10.1002/9781119200871.ch30

Last Updated : 20 August, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

The article provides a valuable analysis of incremental and zero-based budgeting, highlighting their differences and advantages. It’s an informative and engaging read with useful references.

The article is very insightful and beneficial for individuals and businesses alike. It provides valuable information about the different types of budgeting methods, highlighting their differences and importance.

The article provides a thorough analysis of incremental and zero-based budgeting, offering readers valuable insights into the differences and applications of these techniques. The comprehensive information presented is commendable.

I completely agree. The article’s comparison of incremental and zero-based budgeting is highly informative and beneficial, providing readers with an in-depth understanding of these concepts.

The article’s detailed explanation and comparison of incremental and zero-based budgeting are enlightening, making it an essential resource for individuals and businesses seeking to improve their financial management.

The article effectively delves into the intricacies of both incremental and zero-based budgeting, offering readers a detailed comparison and insight into these budgeting methods. The information provided is valuable and thought-provoking.

Absolutely, the article’s breakdown of incremental and zero-based budgeting is thorough and informative, providing readers with a clear understanding of these concepts and their applications.

The article serves as an excellent resource for individuals and companies alike, providing a comprehensive comparison of incremental and zero-based budgeting. The explanations are clear, and the information is highly beneficial.

Absolutely, the detailed explanations and concise comparisons in the article make it a valuable source of knowledge for individuals and organizations looking to enhance their budgeting strategies.

I couldn’t agree more. The article offers valuable insights into both budgeting techniques, making it an essential read for those interested in financial planning.

The comprehensive explanation of incremental and zero-based budgeting in the article provides an excellent overview of these techniques. The insights offered will undoubtedly benefit readers seeking to gain knowledge in this domain.

I couldn’t agree more. The comparison between incremental and zero-based budgeting is insightful and detailed, offering readers a comprehensive understanding of the topic.

Absolutely, the article effectively covers the nuances of both incremental and zero-based budgeting, ensuring that readers have a solid understanding of these methods and their applications.

The article presents a detailed breakdown of the key differences between incremental and zero-based budgeting, making it an informative piece for anyone interested in financial planning.

The article is impressive and comprehensive. It offers a clear understanding of incremental and zero-based budgeting, making it easy for readers to grasp the concepts and apply them effectively.

I completely agree. The detailed comparison table is particularly helpful in understanding the key differences between these two budgeting techniques. The article offers valuable insights for both individuals and companies.

Indeed, the article provides a thorough comparison of incremental and zero-based budgeting, shedding light on their cost, time, approach, and importance. It’s a great resource for anyone looking to gain knowledge in this area.