All the companies and organizations, small or big, needs to prepare their financial statement or end expense statements.

Principle-Based accounting and Rules-Based accounting are two types of accounting methods where principles and rules are added accordingly and separately.

Key Takeaways

- Principle-based accounting focuses on general guidelines, allowing for flexibility and professional judgment.

- Rules-based accounting adheres to strict regulations, reducing ambiguity and inconsistencies.

- Principle-based systems are more adaptable to change, while rules-based systems offer more uniformity in reporting.

Principle-Based Accounting vs Rules-Based Accounting

Principle-based accounting is a flexible method with predefined principles used for preparing financial reports. It lacks consistency as the rules set are not rigid. Rules-based accounting is a rigid method where balance sheets are made based on predefined rules and guidelines. It has consistency due to its rigid rules.

Principle-Based accounting contains standard principles which cannot be changed, and these predefined principles are only used when preparing income statements, balance sheets, or financial statements.

The Rules-Based accounting method uses specific rules which are applied in financial statements. This method is very complex, and the complexity increases with an increase in expenses.

Comparison Table

| Parameters of Comparison | Principle-Based Accounting | Rules-Based Accounting |

|---|---|---|

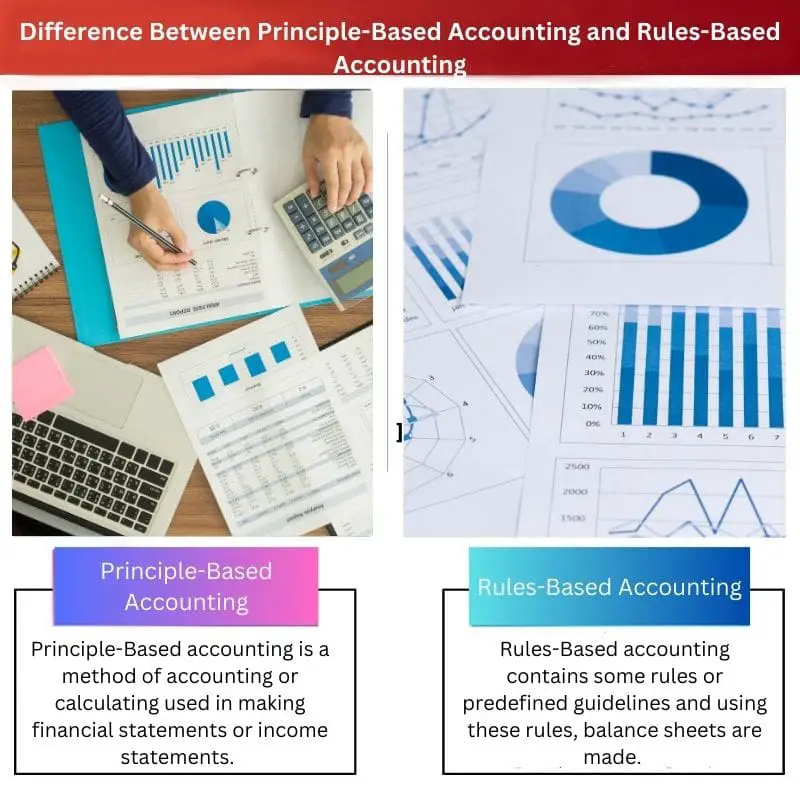

| Definition | Principle-Based accounting is a method of accounting or calculating used in making financial statements or income statements. | Rules-Based accounting contains some rules or predefined guidelines and using these rules, balance sheets are made. |

| Basic dependency | This accounting method depends on principles that are set by the financial accounting standard board and is common for all people. | This accounting method depends on rules which are designed step by step with minimum complexity and can be altered accordingly. |

| Flexibility and complexity | Principle-Based accounting procedures provide you flexibility while accounting, but it becomes complex as the calculation steps increase. | Rules-Based accounting procedure is not very flexible as it has rigorous rules, but the complexity is less. |

| Consistency | The Principle-Based accounting method lacks consistency because of no strict rules present in the method. | The Rules-Based accounting method is more consistent as it contains fixed rules, which are a must. |

| Calculations | This method involves complex calculations, and the projected revenue may vary. | This method contains simple and easy steps without much complexity, and calculations made do not vary. |

| Comparability | The documents or income statements made using this method are hardly comparable and less clear. | Rules-Based documents or financial statements are easily comparable and specified. |

What is Principle-Based Accounting?

Principle-Based accounting uses principles in every step for calculating balance sheets or income statements. International financial reporting standards (IFRS) follow the Principle-Based accounting method.

This accounting method contains guidelines which are needed to be followed while making financial statements. The principles used may vary according to country or state and can be altered according to companies’ convenience.

These principles are easy to apply when it comes to small companies or organizations but their complexity increases as the expenses and the structure of the company increase.

What is Rules-Based Accounting?

The Rules-Based accounting method is a standard method that contains a set of rules that are strictly followed while preparing financial statements or income statements.

Rules-Based accounting is used in (GAAP) accepted accounting principles system. This accounting system helps companies to compare their expenses and profits from other companies in an easy way.

Also, if you are using the Rules-Based accounting method, you create a document that is legal and verified and can be explained almost to anyone by specifying each rule used at every point.

Main Differences Between Principle-Based Accounting and Rules-Based Accounting

- The Principle-Based accounting method lacks consistency because of no strict rules present in the method. In contrast, the Rules-Based accounting method is more consistent as it contains fixed rules, which are a must.

- The Principle-Based accounting method depends on principles that are set by the financial accounting standard board and is common for all people.

- https://www.tandfonline.com/doi/abs/10.1080/09639284.2011.569128

- https://meridian.allenpress.com/accounting-review/article-abstract/87/4/1247/53947

Last Updated : 20 August, 2023

Chara Yadav holds MBA in Finance. Her goal is to simplify finance-related topics. She has worked in finance for about 25 years. She has held multiple finance and banking classes for business schools and communities. Read more at her bio page.

This is a very detailed piece, but the bias diminishes its value. A more balanced approach would enhance the credibility of the content.

Although it provides thorough insights into the accounting methods, the evident bias raises questions about its fairness.

This is a well-written and informative article! Principles-based accounting sounds more adaptable while rules-based accounting ensures consistency. I enjoyed reading this.

This is a solid comparison; it provides clear distinctions between the two methods. I find the analysis very helpful.

Agreed, it’s an informative piece but the bias is very pronounced.

The overt bias takes away from the credibility of the content, but the clarity is commendable.

Good analysis of the accounting methods. Although one-sided in favor of rules-based accounting, it gives a clear explanation and I appreciate that.

Yes, the content gives an informative comparison, but it does show bias.

I agree on the bias, but it does provide a solid overview of the two methods.

The information is useful and well-detailed. However, the bias in favor of rules-based accounting is apparent.

I think the bias is a bit too conspicuous, which detracts from the overall value.

It certainly gives a clear explanation, but I agree, a more balanced view would be better.

The article explains the two accounting methods very well but it shows a strong favoritism towards rules-based accounting. The objectivity is questionable.

Indeed, the subject matter is presented clearly, but the bias is somewhat concerning.

The comparison is detailed and gives a good understanding of the two methods. However, it tends to lean more towards rules-based accounting.

I see your point; the content does seem to favor rules-based accounting. A more balanced view would make it more effective.

While it offers a comprehensive analysis, the heavy bias detracts from the overall effectiveness of the content.

Rules-based accounting sounds legal and verified, but principle-based accounting offers flexibility. I appreciate the clear differentiation.

Absolutely, this provides a focused comparison. I find it highly beneficial for understanding the two accounting methods.

The clarity in differentiating the two methods is noteworthy, yet the bias raises questions about the objectivity of the content.