Expenses and expenditures are two different terms used to define economic outflows in business. Expenses refer to those outflows that aid in the revenue generation process (e.g., rent and salaries). The term expenditures encompass all those outflows that help create the revenue-generating capacity of a business (e.g., purchasing capital assets).

Key Takeaways

- Expenses are costs incurred during a business’s normal operations, such as salaries, rent, and utilities.

- Expenditures are broader and include operating expenses and capital investments, such as purchasing equipment or property.

- Both expenses and expenditures are crucial for planning, budgeting, and evaluating a company’s financial health.

Expenses vs Expenditures

Expenses refer to the cost of running a business or maintaining a household. Expenses may include salaries, utility bills, etc. An expenditure is a cost that is necessary for a business to succeed, including routine expenses and capital investments. It may involve buying machinery, vehicles, etc.

Expenses are short-term costs incurred in the normal course of business. They cover charges like rent, salaries, utility bills (e.g., electricity/telephone), etc. They are essential for running a business and help to smoothen the path of revenue-generating activities. E.g., paying rent ensures businesses have a place to carry on their processes to generate revenue.

Expenditures are costs associated with the purchase of assets and other goods/services that will provide economic benefits over a longer period. E.g., costs incurred on purchasing a machine will ensure that work is done using the same for a long duration and will help in the production of goods for sale.

Comparison Table

| Parameters of Comparison | Expenses | Expenditures |

|---|---|---|

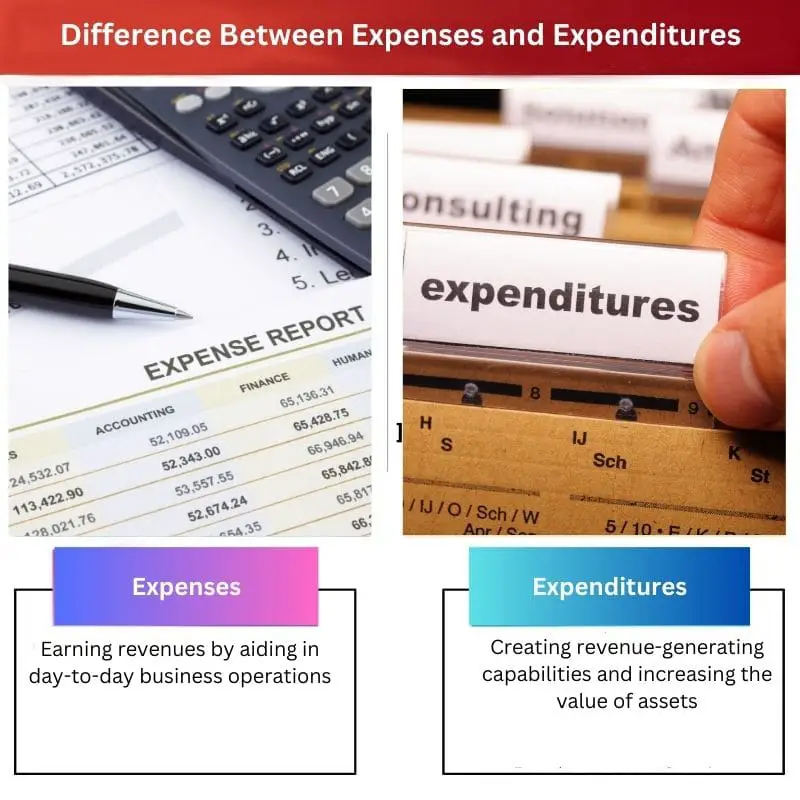

| Purpose | Earning revenues by aiding in day-to-day business operations | Creating revenue-generating capabilities and increasing the value of assets |

| Duration of benefits | Short-term (less than one year) | Long-term (more than one year) |

| Types | Major types include variable, fixed, intermittent, and discretionary expenses | Major types include capital and revenue expenditures |

| Impact on financial results and profit | Direct impact | Indirect impact |

| Recurrence | Frequently | Occasionally |

| Examples | Outflows relating to rent, salaries, utility bills, etc. | Outflows relating to the purchase of assets (like buildings), expansion of existing office space, etc. |

| Reflection on financial statements | Appear on Income Statements | Appear on Balance Sheets |

What is Meant by Expenses?

Expenses are essentially payments made to third parties for the use of basic everyday facilities to ensure the running of normal business procedures.

Expenses can be called the lifeblood for sustaining the framework of a business. They help in carrying out revenue-generation activities of a business seamlessly. They also ensure that the business has the support necessary to cater to all its various processes. E.g., payment towards electricity bills ensures that the business has a steady electricity connection to carry out its operations.

Accounting for expenses in the double-entry bookkeeping system affects both the Balance Sheet and Income Statement. E.g., payment made towards telephone bills will have the following twofold effect at the point of time of the transaction:

- It will lead to a decrease (or credit) in the balance of cash equivalents.

- It will lead to an increase (or debit) in expenses which will be shown as a deduction from revenue to calculate profits.

Thus, expenses directly affect a business’s profits as they are deducted from revenues to calculate net income. Most expenses being admissible for tax deduction purposes lead to a reduction in a business’s tax liabilities.

What is Meant by Expenditures?

Expenditures are cash outflows in favour of another person or entity that are incurred to acquire assets or increase the net worth of a business. Common examples of expenditures can be purchases of machinery, buildings, vehicles, land, etc.

Expenditures can be called the backbone for building a business’s framework. They lead to capital formation and increase the value of a business. They may also be applied to maintain the existing capabilities of a business. E.g., costs incurred towards buying and installing the latest versions of monitors for all the computers of an office to increase performance.

Accounting for expenditures in the double-entry bookkeeping system affects two Balance Sheet accounts. E.g., the purchase of a car will have the following twofold effect at the point of time of the transaction:

- It will lead to a decrease (or credit) in the balance of cash equivalents.

- It will lead to an increase (or debit) in the balance of the vehicle’s account.

Expenditures do not affect the profits of a business directly as they are not deducted from revenue to calculate net income. They are inadmissible for tax deduction purposes, too, except in some special cases where grants/tax relief is granted by government authorities to encourage capital building in the nation.

Main Differences Between Expenses and Expenditures

- Expenses are costs incurred in due course of business, whereas expenditures are outflows that aim towards increasing the value of the business and its assets as well as creating revenue-generating facilities.

- The economic benefits from expenses are short-term (i.e., they can be enjoyed for less than one year), whereas expenditures provide long-term economic benefits of more than one year.

- Major types of expenses include variable (e.g., electricity bills), fixed (e.g., rent), intermittent (e.g., income taxes), or discretionary expenses (e.g., bonuses). On the other hand, expenditures can be majorly classified into capital (e.g., a purchase of machinery) or revenue expenditures (e.g., repair of such machinery).

- Expenses directly affect cash profits as they are expressed as deductions from revenues to calculate net income. Conversely, expenditures do not directly affect cash profits but can help boost revenue and profits in the future (e.g., buying new machinery may help speed up production and sales).

- Expenses are incurred frequently, whereas expenditures are infrequent occurrences.

- Examples of expenses include rent, salaries, utility bills, etc. Alternatively, examples of expenditures include purchasing of buildings, expansion of office space, etc.

- Expenses are reflected on the Income Statement, whereas expenditures appear on the Balance Sheet.